Zygomatic And Pterygoid Implants Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

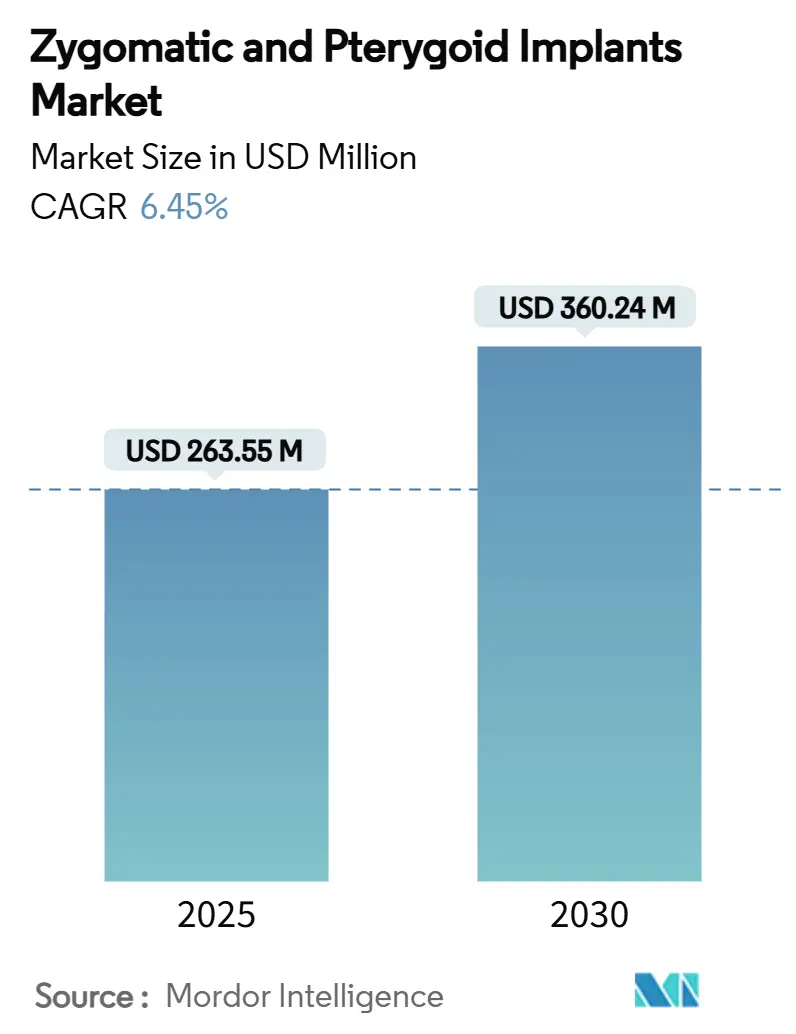

| Market Size (2025) | USD 263.55 Million |

| Market Size (2030) | USD 360.24 Million |

| Growth Rate (2025 - 2030) | 6.45% CAGR |

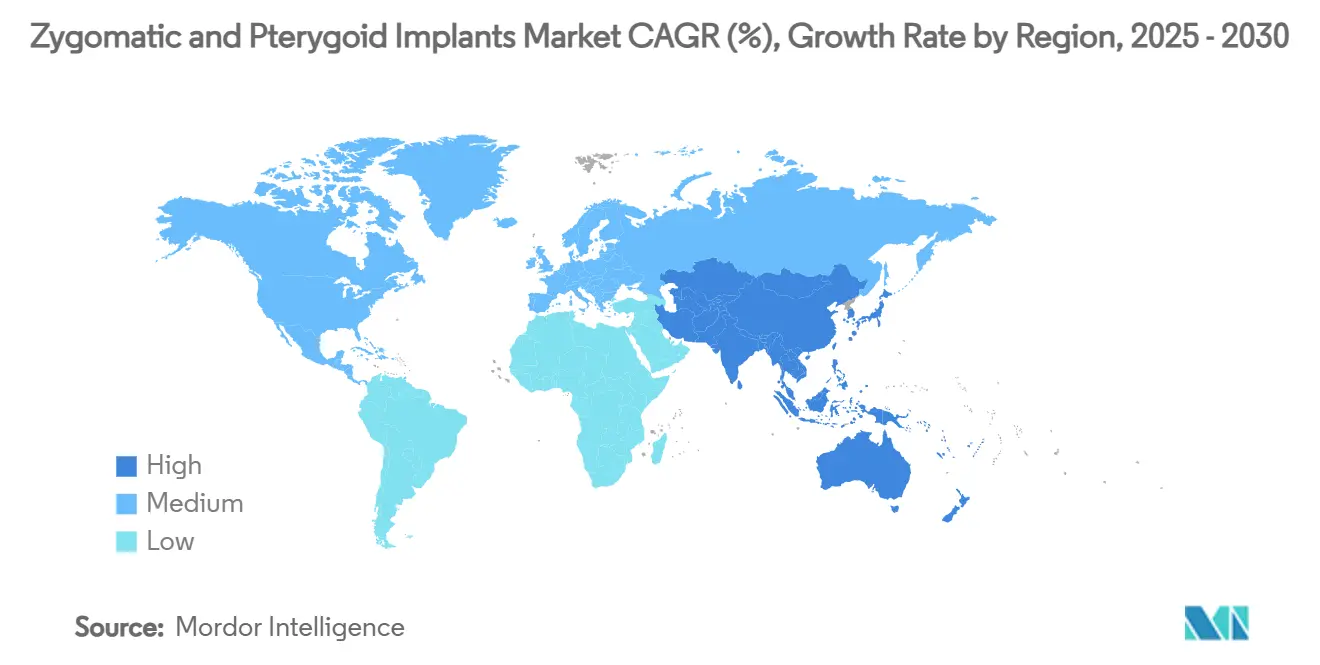

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Zygomatic And Pterygoid Implants Market Analysis by Mordor Intelligence

The zygomatic & pterygoid implants market size stands at USD 263.55 million in 2025. It is forecast to reach USD 360.24 million by 2030, reflecting a 6.45% CAGR during the period and underscoring strong momentum in the specialty implant category. Sustained acceptance among surgeons, faster patient rehabilitation, and the ability to avoid bone-grafting procedures position the Zygomatic & Pterygoid Implants market as the preferred option for complex maxillary reconstruction. Immediate loading dominates demand, digital workflows improve placement accuracy, and regulatory clarity from the October 2024 FDA guidance accelerates new product clearances. Competitive dynamics favor suppliers that combine long-term clinical evidence with AI-enabled navigation tools and robust training networks. Emerging regenerative therapies and persistent cost barriers moderate expansion yet do not offset the favorable long-term trajectory of the Zygomatic & Pterygoid Implants market.

Key Report Takeaways

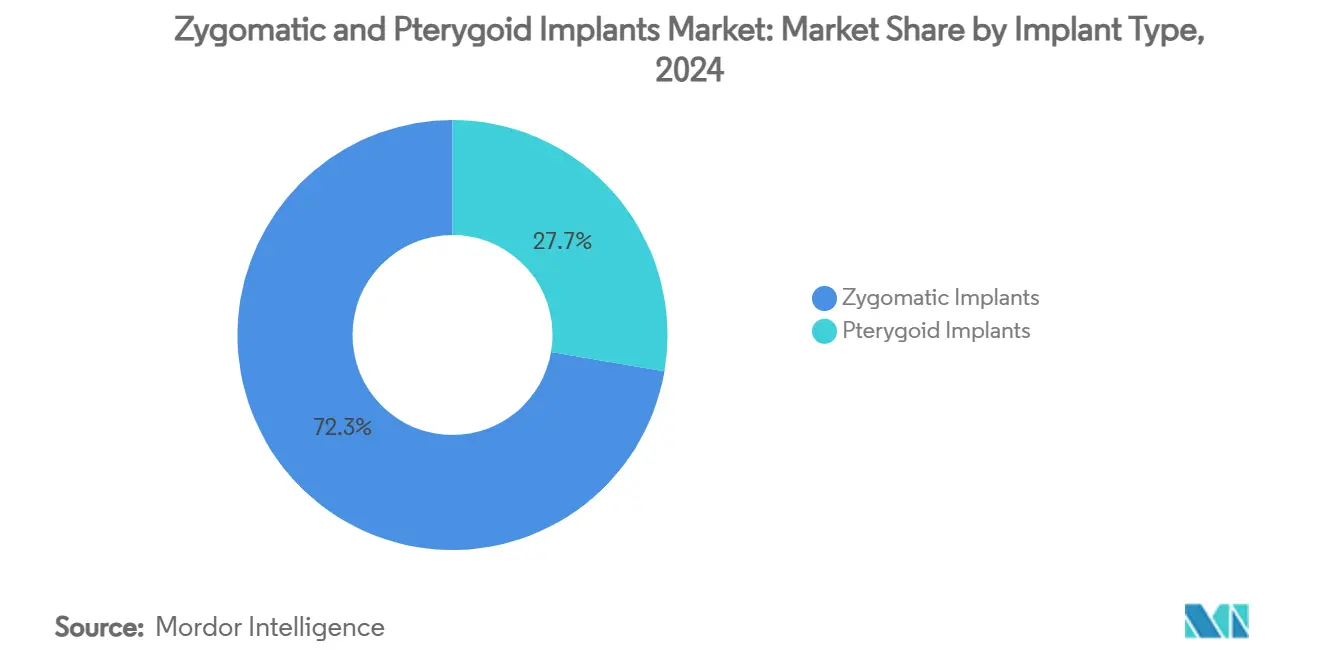

- By implant type, zygomatic implants led with 72.34% share in 2024; pterygoid implants are projected to expand at an 8.54% CAGR through 2030.

- By product length, 30–50 mm devices captured 46.54% revenue share in 2024, while implants above 50 mm are forecast to post an 8.67% CAGR between 2025 and 2030.

- By procedure type, immediate loading dominated with 63.23% share in 2024 and is also advancing at an 8.45% CAGR over the forecast period.

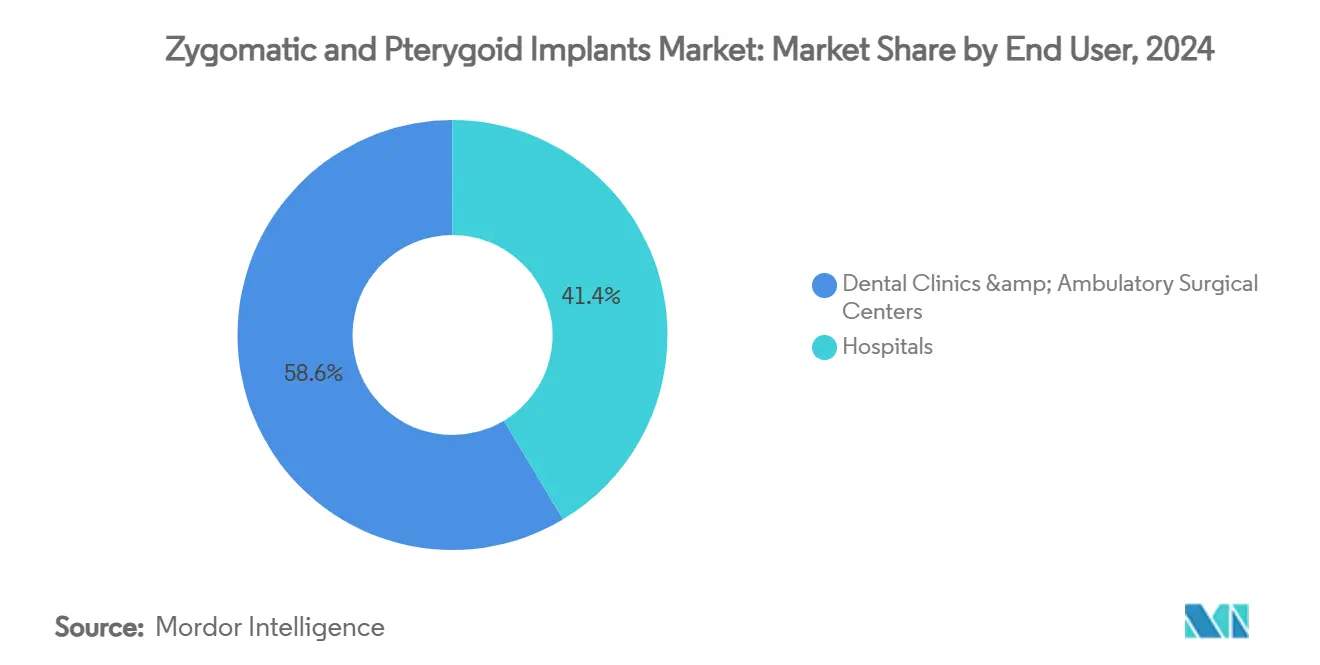

- By end user, dental clinics and ambulatory surgical centers held 58.65% of 2024 revenue, as hospitals register the highest projected CAGR at 9.56% through 2030.

- By application, maxillary sinus reconstruction accounted for 55.43% of 2024 sales, whereas severe maxillary bone atrophy cases are set to grow at a 9.67% CAGR to 2030.

- By geography, North America represented 42.34% share in 2024, while Asia-Pacific is poised for the fastest growth with a 7.54% CAGR during 2025–2030.

Global Zygomatic And Pterygoid Implants Market Trends and Insights

Driver Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of edentulism and atrophic maxilla | +1.8% | Global, concentrated in aging populations of North America & Europe | Long term (≥ 4 years) |

| Expanding global geriatric demographics | +1.5% | Global, particularly developed economies | Long term (≥ 4 years) |

| Growing preference for immediate-loading implant solutions | +1.2% | North America & Europe leading, expanding to Asia-Pacific | Medium term (2-4 years) |

| Advances in digital dentistry and surgical navigation | +1.0% | Global, with early uptake in high-income markets | Medium term (2-4 years) |

| Increasing dental tourism to cost-competitive markets | +0.7% | Asia-Pacific core hubs, spill-over to Latin America | Short term (≤ 2 years) |

| Expanded clinical training and certification programs | +0.3% | Global, emphasis on emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Edentulism and Atrophic Maxilla

Severe maxillary bone loss continues to stimulate demand for specialized implants because conventional graft-dependent protocols prove inadequate in many elderly cases. Clinical follow-ups indicate 90.7% success for pterygoid fixtures in atrophic posterior maxillae, which eliminates sinus-lift morbidity and shortens chair time[1]Foundation for Oral Rehabilitation, “Long-Term Outcomes of Pterygoid Implants,” FOR.org. Population aging intensifies the prevalence of edentulism, and cone-beam studies show that 116 of 120 examined atrophic arches can accommodate virtual pterygoid placement, validating broad anatomical applicability. Digital planning complements anatomical feasibility by mapping angulation and depth, thereby reducing intraoperative guesswork and enhancing primary stability for the Zygomatic & Pterygoid Implants market. Surgeons emphasize graftless approaches to minimize healing disruptions, and patients appreciate shorter treatment cycles, reinforcing sustained uptake of these complex fixtures.

Expanding Global Geriatric Demographics

The share of individuals above 65 years is rising, and their prosthetic expectations evolve toward minimally invasive therapy. Evidence shows implant therapies designed for ultra-aged profiles reduce systemic risk because they avoid donor-site graft harvesting. Zygomatic constructs sidestep the morbidity linked with sinus augmentation, making them clinically attractive for elderly cohorts with compromised healing. Digital workflows further enhance predictability by enabling restorative loading within 24 hours, as validated by immediate protocols that restore mastication and speech on the same day. These demographic shifts ensure that the Zygomatic & Pterygoid Implants market remains aligned with expanding geriatric care pathways.

Growing Preference for Immediate-Loading Implant Solutions

Patients increasingly demand same-day function that avoids removable prostheses and multiple surgeries. Clinical monitoring over 77.9 months demonstrates 100% survival for immediately loaded implants in edentulous maxillae and correlates with improved psychological well-being. Protocols such as “One Shot” employ titanium frameworks to simplify laboratory steps and achieve rapid aesthetic results. Accuracy from static and dynamic guides outperforms freehand placement, fostering surgeon confidence in immediate delivery. Consequently, immediate loading solidifies dominance inside the Zygomatic & Pterygoid Implants market as both a revenue leader and the fastest-growing procedural segment.

Advances in Digital Dentistry and Surgical Navigation

AI-powered workflows identify bone contours and nerve pathways, delivering 90% diagnostic accuracy and cutting placement errors by 43%, which safeguards outcomes. Robotic assistance further narrows coronal and apical deviation compared with dynamic navigation systems, underscoring superior mechanical precision. Optical coherence tomography now replaces radiation-based imaging for certain chairside steps, trimming two-visit crown procedures to 15 minutes while boosting patient throughput. With training modules integrated into these platforms, the Zygomatic & Pterygoid Implants market benefits from higher procedural adoption and lower revision incidence.

Restraints Impact Analysis

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procedure cost and limited insurance coverage | -2.1% | Worldwide, more acute in lower-income regions | Medium term (2-4 years) |

| Postoperative sinusitis and infection risks | -0.8% | Global, heightened where surgical expertise is limited | Short term (≤ 2 years) |

| Limited surgeon expertise in complex implant techniques | -0.6% | Emerging markets and select developed regions | Medium term (2-4 years) |

| Emerging alternative bone regeneration therapies | -0.5% | High-income markets with advanced R&D activity | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Procedure Cost and Limited Insurance Coverage

Full-arch rehabilitation costs range from USD 60,000 to USD 90,000, a barrier that deters many candidates from seeking care. U.S. federal insurance programs exclude implant benefits, and only a subset of Medicare Advantage plans provide partial reimbursement with annual caps as low as USD 1,500. Private carriers impose “missing-tooth” exclusions, obligating patients to self-finance via payment plans or membership-based discount networks. Out-of-pocket liabilities slow uptake in emerging economies where average per-capita income is lower, thereby restraining global growth for the Zygomatic & Pterygoid Implants market despite clinical advantages.

Postoperative Sinusitis and Infection Risks

Zygomatic anchorage traverses the sinus wall, heightening the chance of postoperative sinusitis that requires direct sinus access, saline irrigation, and prolonged antibiotic therapy[2]International Journal of Implant Dentistry, “Virtual Planning of Pterygoid Implants in Atrophic Maxillae,” implant-dentistry.org. Systematic reviews cite 12.4% sinus-related complications and occasional ocular events that can become vision-threatening if unmanaged. These risks mandate strict patient screening and surgeon proficiency, which hinders procedure diffusion in regions lacking advanced training facilities. Litigation fears and additional aftercare visits also inflate total treatment costs, collectively tempering the otherwise strong expansion of the Zygomatic & Pterygoid Implants market.

Segment Analysis

By Implant Type: Zygomatic Dominance Drives Market Leadership

Zygomatic fixtures delivered 72.34% of the 2024 Zygomatic & Pterygoid Implants market size following decades of longitudinal evidence that confirms 96.1% ten-year survival for systems such as NobelZygoma[3]Nobel Biocare, “NobelZygoma Clinical Evidence Compendium,” NobelBiocare.com. This dominance is reinforced by surgeon familiarity and comprehensive instrumentation sets that shorten operating time. Nonetheless, pterygoid devices post an 8.54% CAGR to 2030, reflecting their ability to bypass sinus anatomy and secure cortical bone in the pterygoid process. The “VIV” concept, which combines three anterior with two pterygoid implants, reduces cantilever forces and widens stress distribution, thus appealing to clinicians treating extreme atrophy.

Digital planning tools simulate implant trajectory and length, improving safety margins and helping practitioners visualize anatomical constraints. Studies reveal 7.1 mm average bone engagement beyond the pterygoid junction, a parameter that predicts superior primary stability. Together, these attributes strengthen the Zygomatic & Pterygoid Implants market, where both implant types complement each other to broaden the treatable patient population.

Note: Segment shares of all individual segments available upon report purchase

By Product Length: Extended Lengths Enable Complex Anatomy Solutions

Implants measuring 30–50 mm held 46.54% Zygomatic & Pterygoid Implants market share during 2024 because they suit common maxillary atrophy scenarios and fit within commercially available drill kits. Devices exceeding 50 mm length accelerate at an 8.67% CAGR because they anchor into dense zygomatic cortex or pterygoid plates, increasing torque values and allowing immediate provisionalization in extreme cases. Extended lengths further decrease cantilever stress on distal prosthetic units, thereby boosting long-term stability.

Surface modifications, including acid etching and UV activation, stimulate osteoblast activity and improve osseointegration speed, which is critical for immediate loading. Conversely, implants shorter than 30 mm focus on mild to moderate atrophy, but their adoption remains slower as clinicians gravitate toward more versatile intermediate lengths. The result is a balanced portfolio within the Zygomatic & Pterygoid Implants market that caters to varying anatomical presentations.

By Procedure Type: Immediate Loading Transforms Patient Experience

Immediate protocols accounted for 63.23% revenue in 2024 and advance at 8.45% CAGR, cementing their role as both the largest and the quickest-growing category within the Zygomatic & Pterygoid Implants market. Same-day restoration alleviates patient anxiety associated with removable dentures, and computer-guided surgery ensures predictable placement even in severe atrophy. Clinical series report 98.04% survival when combining transcrestal sinus lifts with immediate implants, further validating the approach.

Delayed loading today fills niche indications such as insufficient primary stability or systemic conditions that impair healing. Even in those situations, enhanced surface treatments shorten the transition later on. Consequently, implant manufacturers invest in abutment designs optimized for immediate temporization, and software vendors integrate occlusal schemes to facilitate chairside provisionalization.

By End User: Hospital Integration Accelerates Specialized Care

Dental clinics and ambulatory centers retained 58.65% of the 2024 Zygomatic & Pterygoid Implants market size due to established referral networks and seasoned implantologists. Yet hospitals expand at 9.56% CAGR through 2030, propelled by multidisciplinary capabilities that accommodate high-risk cases and comprehensive anesthesia resources. Hospital-based programs now incorporate navigation labs and prosthetic milling suites, delivering fully digital workflows under one roof that enhance efficiency and patient comfort.

Institutional investment in robotic platforms strengthens accuracy and standardizes complex procedures across resident training programs. Collaborative care models also facilitate management of comorbidities typical in elderly edentulous patients, thereby widening access and fueling overall growth in the Zygomatic & Pterygoid Implants market.

Note: Segment shares of all individual segments available upon report purchase

By Application: Severe Atrophy Cases Drive Innovation

Maxillary sinus reconstruction contributed 55.43% revenue in 2024, underscoring the frequency of sinus-linked bone resorption. Severe atrophy emerges as the fastest-growing application at 9.67% CAGR, motivated by the high success of zygomatic approaches that achieve 96.3% five-year survival while cutting operative time to 177 minutes compared with bone-graft alternatives. Digital renderings assess bone stock and visualize safe angulation for extra-sinus pathways, enabling treatment where grafting once ruled out implant rehabilitation.

Reconstructive indications after trauma or congenital defects benefit from the same technology stack but represent smaller volume. Still, advances such as patient-specific guides and stackable prosthetic substructures continue to press innovation forward, reinforcing the comprehensive appeal of the Zygomatic & Pterygoid Implants market.

Geography Analysis

North America retained 42.34% market share in 2024 as premium procedures and training intensity aligned to patient demand for predictable outcomes. Adoption of AI navigation and strict adherence to the October 2024 FDA guidance sustain clinician confidence, although Straumann reported soft implantology sales as penetration levels approach maturity. Growth now centers on complex reconstructions that carry higher average selling prices, ensuring the Zygomatic & Pterygoid Implants market maintains value leadership within the region.

Asia-Pacific posts the highest trajectory at a 7.54% CAGR, buoyed by aggressive health-care investments, medical-tourism incentives, and technological diffusion. Straumann logged 82% organic sales growth in Q1 2024 as Chinese demand recovered and Southeast Asian clinics promoted cost-effective yet sophisticated care pathways. Regulatory reforms that expedite import approvals further encourage manufacturers to prioritize APAC rollouts of zygomatic and pterygoid systems.

Europe delivers steady mid-single-digit growth supported by robust training frameworks such as ITI’s European Campus and harmonized CE marking that streamlines market entry. Clinicians leverage well-developed insurance schemes, although cost containment measures in certain countries nudge some patients toward neighboring lower-cost destinations. Latin America and the Middle East & Africa remain nascent markets but display increasing awareness and incremental infrastructure upgrades that unlock gradual opportunities for the Zygomatic & Pterygoid Implants market.

Competitive Landscape

The supplier base is moderately consolidated with Straumann, Nobel Biocare, and Dentsply Sirona controlling a majority of specialist implant revenue. Nobel Biocare’s catalog is backed by 81 clinical studies spanning 25 years, fostering trust among surgeons handling high-stakes atrophy cases. Straumann pursues abutment innovation, filing patents for laser-textured surfaces that enhance prosthetic bonding and potentially shorten chairside adjustments. Dentsply Sirona builds on software-hardware integration through its intraoral scanners and chairside mills, creating seamless workflows that appeal to multi-location practices.

Challenger brands such as Southern Implants and Noris Medical differentiate via niche designs and localized service, while Osstem Implant’s acquisition pursuits signal ambitions to broaden geographic reach. Across all tiers, investments gravitate toward AI planning modules, guided-surgery consumables, and continuing-education portals, which together drive sustainable engagement within the Zygomatic & Pterygoid Implants market. Regulatory expertise and post-market surveillance infrastructures remain decisive barriers, thus favoring incumbents with global compliance track records.

Zygomatic And Pterygoid Implants Industry Leaders

-

Noris Medical

-

S.I.N. Implant System

-

Southern Implants

-

Straumann Holding AG

-

IDC Implant & Dental Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Proclaim raised capital to scale its Custom-Jet Oral Health System, enrolling 700+ practices.

- January 2025: Nuvia Dental Implant Center earned 2024 recognition for its “permanent teeth in 24 hours” protocol.

- December 2024: Patient Square Capital acquired Patterson Companies for USD 4.1 billion with intentions to take the distributor private at a 49% shareholder premium.

- October 2024: FDA issued comprehensive guidelines on endosseous dental implants and abutments, defining safety-based performance criteria and streamlining 510(k) pathways.

- August 2024: Perceptive showcased the first fully automated dental procedure using AI robotics, reaching 90% cavity-detection accuracy and cutting chair time to 15 minutes.

- July 2024: Henry Schein bought abc dental AG for USD 27.5 million to deepen presence in French and German-speaking markets.

Global Zygomatic And Pterygoid Implants Market Report Scope

As per the scope of the report, zygomatic and pterygoid implants are a unique option for the upper jaw when there is significant bone loss. Zygomatic and pterygoid implants anchor in the jaw bone and the bone behind the upper jaw, as opposed to normal dental implants, which do so in the jaw bone. The Zygomatic and Pterygoid Implants Market is Segmented by Product Length (Upto 30 mm, 30-50 mm, and Above 50 mm), Application (Maxillary Sinuses, Severe Atrophy of Maxillary Bone, and Other Applications), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Zygomatic Implants |

| Pterygoid Implants |

| Up To 30 mm |

| 30 – 50 mm |

| Above 50 mm |

| Immediate Loading |

| Delayed Loading |

| Hospitals |

| Dental Clinics & Ambulatory Surgical Centers |

| Maxillary Sinus Reconstruction |

| Severe Maxillary Bone Atrophy |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Implant Type | Zygomatic Implants | |

| Pterygoid Implants | ||

| By Product Length | Up To 30 mm | |

| 30 – 50 mm | ||

| Above 50 mm | ||

| By Procedure Type | Immediate Loading | |

| Delayed Loading | ||

| By End User | Hospitals | |

| Dental Clinics & Ambulatory Surgical Centers | ||

| By Application | Maxillary Sinus Reconstruction | |

| Severe Maxillary Bone Atrophy | ||

| Other Applications | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the Zygomatic & Pterygoid Implants market?

The specialty segment is valued at USD 263.55 million in 2025 with a forecast to reach USD 360.24 million by 2030.

How fast is demand growing for immediate-loading implant procedures?

Immediate protocols are expanding at an 8.45% CAGR and already account for 63.23% of overall revenue.

Which region presents the highest growth opportunity?

Asia-Pacific leads with a 7.54% CAGR through 2030 owing to robust dental tourism and rising healthcare investment.

What are the main cost barriers to adoption?

Full-arch rehabilitation ranges from USD 60,000 to USD 90,000, and insurance coverage is often limited or capped at low annual maximums.

How do digital workflows enhance surgical precision?

AI planning and robotic guidance cut placement deviations and reduce complication rates, improving long-term implant survival.

Which implant length segment is gaining momentum?

Devices longer than 50 mm exhibit the fastest growth at an 8.67% CAGR because they anchor securely in dense anatomical structures.

Page last updated on: