Voice Prosthesis Devices Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

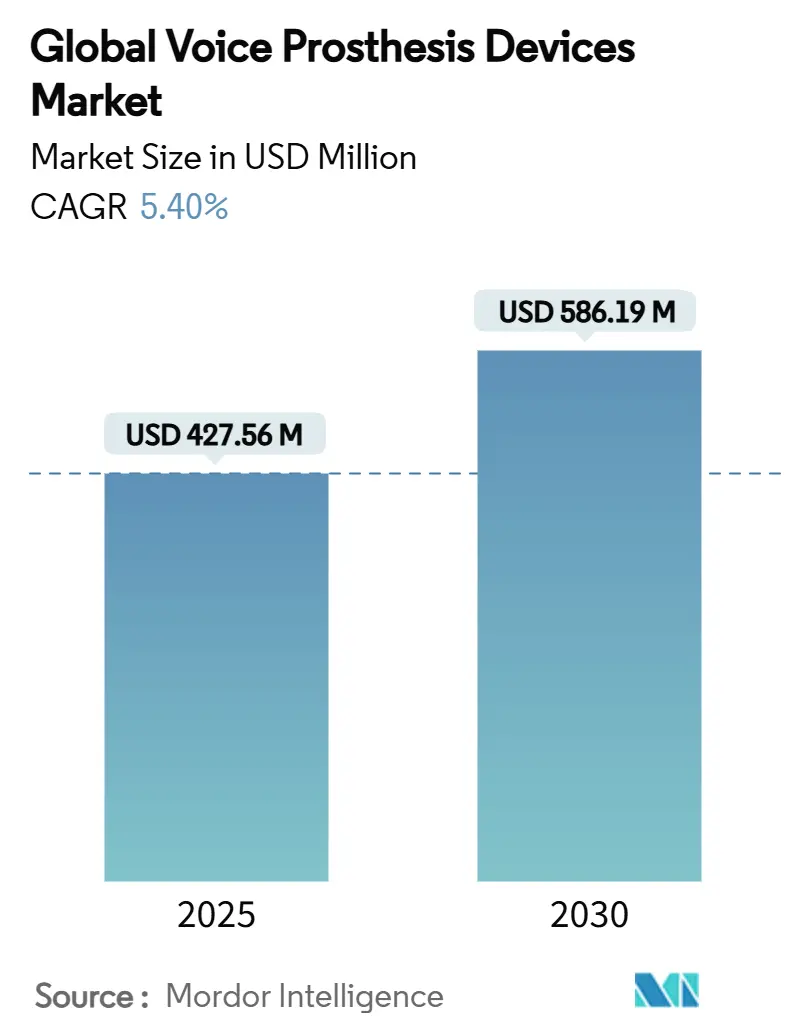

| Market Size (2025) | USD 427.56 Million |

| Market Size (2030) | USD 586.19 Million |

| Growth Rate (2025 - 2030) | 5.40% CAGR |

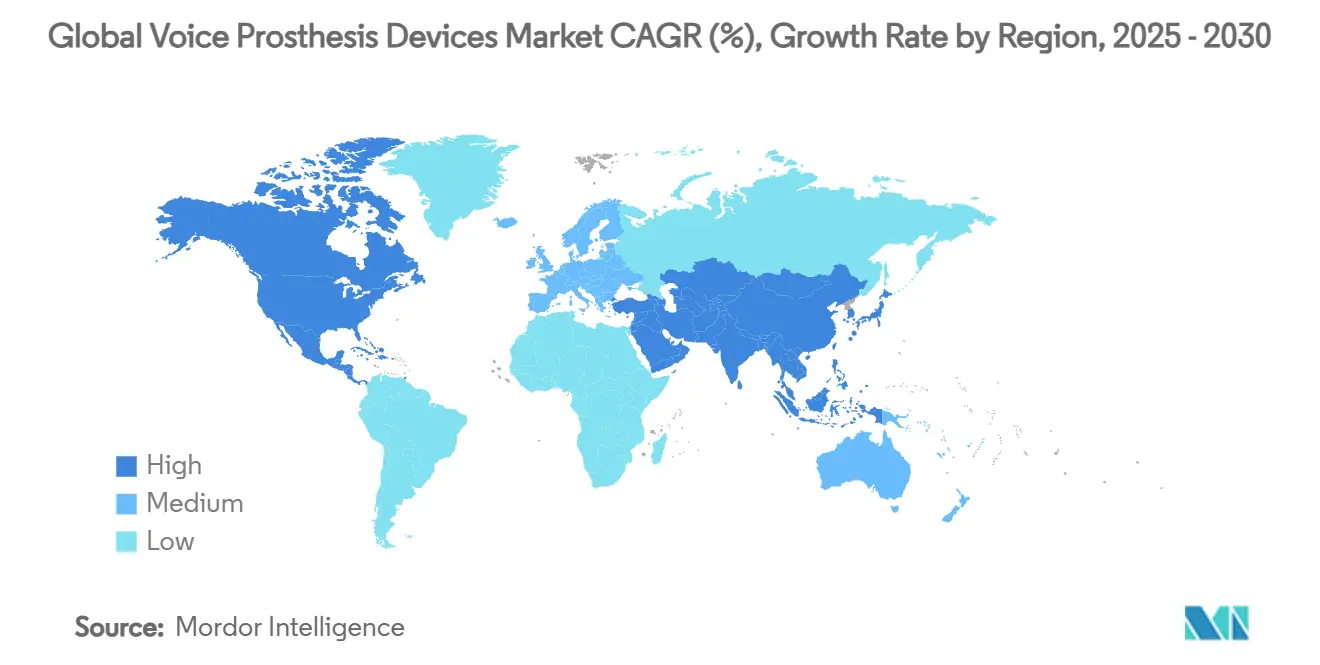

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Voice Prosthesis Devices Market Analysis by Mordor Intelligence

The voice prosthesis devices market size is valued at USD 427.56 million in 2025 and is projected to reach USD 586.19 million by 2030, expanding at a 5.40% CAGR during the forecast period . Steady progress in biofilm-resistant valve materials, broader reimbursement in high-income regions and a rising pool of laryngectomy survivors sustain this trajectory for the voice prosthesis devices market. North America keeps the largest revenue base, yet Asia-Pacific posts the quickest gains as domestic manufacturers introduce lower-priced products adapted to regional budgets. Regulatory convergence—most notably the 2026 alignment of the FDA’s quality-system rule with ISO 13485—raises compliance costs but shortens multi-region registration cycles, enabling quicker launches. In parallel, the migration of ENT procedures to outpatient settings multiplies yearly replacement volumes while intensifying price sensitivity.

Key Report Takeaways

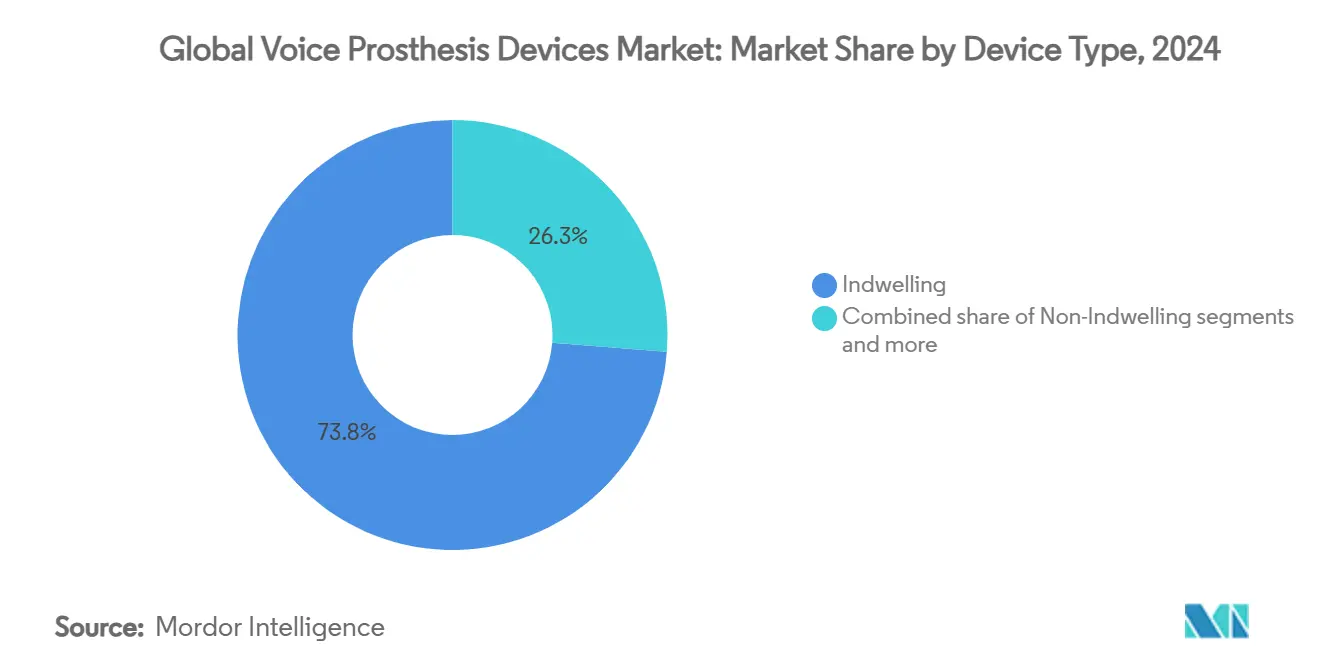

- By device type, indwelling systems captured 73.75% of voice prosthesis devices market share in 2024; non-indwelling systems record the fastest 6.05% CAGR through 2030.

- By valve type, Provox Series led with 62.30% revenue share in 2024, while Blom-Singer Dual Valve systems advance at a 6.47% CAGR to 2030.

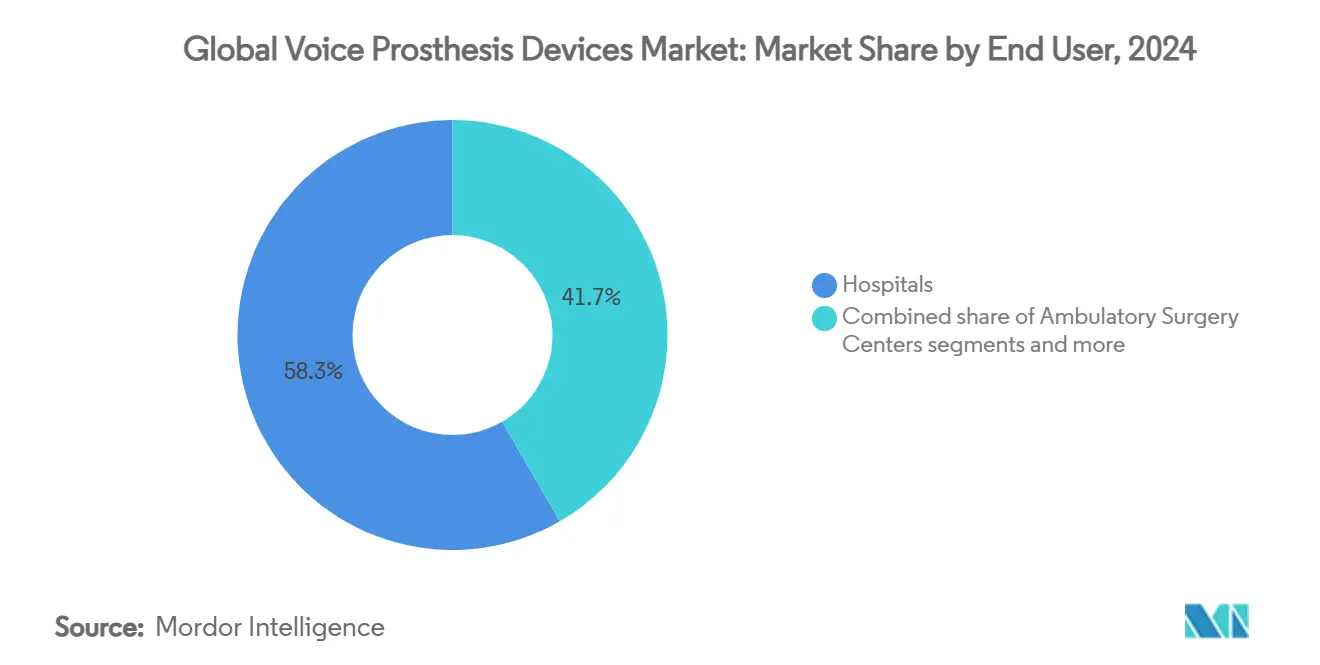

- By end user, hospitals commanded 58.31% of the voice prosthesis devices market size in 2024, whereas specialty clinics are expanding at a 6.91% CAGR through 2030.

- By geography, North America held 41.33% revenue in 2024; Asia-Pacific is projected to widen at a 7.39% CAGR to 2030.

Global Voice Prosthesis Devices Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of laryngeal cancer and total laryngectomies | +1.2% | Global, with highest impact in North America and Europe | Medium term (2-4 years) |

| Technological advances extending prosthesis lifetime | +0.9% | Global, led by developed markets | Long term (≥ 4 years) |

| Expanding reimbursement coverage in high-income countries | +0.8% | North America, Europe, select APAC markets | Medium term (2-4 years) |

| Growing ENT-focused surgical volumes in outpatient settings | +0.7% | North America, Europe, urban APAC centers | Short term (≤ 2 years) |

| Adoption of low-cost indigenous prostheses in price-sensitive Asia | +0.6% | Asia-Pacific, emerging markets | Medium term (2-4 years) |

| Additive-manufactured custom valves improving fit & comfort | +0.4% | Developed markets with advanced manufacturing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Laryngeal Cancer and Total Laryngectomies

Population-based data show 104 991 U.S. cases between 2000-2020, a figure expected to escalate as the population ages. Europe and Asia present similar upward trends, and forecasts point to a 50% rise in hypopharyngeal cancer by 2040. Because 70-75% of laryngectomy survivors become candidates for a prosthetic voice, incidence trends convert directly into demand, reinforcing the growth curve of the voice prosthesis devices market.

Technological Advances Extending Prosthesis Lifetime

Next-generation silicone blends, hydrophobic coatings and magnet-assisted closures double functional life from six to twelve months in early studies. Custom 3-D-printed flanges reduce fit-related leakage, while antimicrobial surfaces slow fungal colonisation. These improvements lower replacement frequency and total cost of ownership, encouraging clinicians in developed regions to recommend indwelling models more readily and sustaining revenue momentum across the voice prosthesis devices market.

Expanding Reimbursement Coverage in High-Income Countries

U.S. payers such as Aetna classify indwelling voice valves as durable medical equipment and reimburse replacements twice yearly when medically justified. Germany’s 2025 OPS code update adds endoscopic replacement codes, improving billing clarity. When coverage removes financial barriers, patients adhere to the optimal replacement cycle, which heightens recurring demand and underpins the voice prosthesis devices market.

Outpatient ENT Surgery Growth

Ambulatory centres served 3.3 million Medicare fee-for-service beneficiaries in 2022, with USD 6.1 billion in spending.. ENT teams increasingly use modified retrograde insertion techniques that allow same-day discharge. Lower facility costs appeal to payers, while convenience attracts patients, pushing more replacements—and thus market revenue—into high-throughput outpatient channels of the voice prosthesis devices market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High replacement costs and limited insurance in emerging markets | -0.8% | Asia-Pacific, Latin America, Africa | Medium term (2-4 years) |

| Device-related complications (leakage, biofilm, aspiration) | -0.6% | Global, with higher impact in resource-limited settings | Short term (≤ 2 years) |

| Stringent sterilization/supply-chain regulations raising COGS | -0.4% | Global, particularly affecting smaller manufacturers | Long term (≥ 4 years) |

| Shortage of trained TEP surgeons in low-resource regions | -0.5% | Emerging markets, rural areas globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Replacement Cost and Limited Insurance in Emerging Markets

In price-sensitive countries, a single indwelling valve can equal a worker’s monthly wage. India’s Aum Voice Prosthesis retails at one-third the price of imports yet still meets resistance when insurance is absent. High out-of-pocket burdens discourage timely replacements, clipping 0.8 percentage points from the expected CAGR for the voice prosthesis devices market.

Device-Related Complications (Leakage, Biofilm, Aspiration)

Australian surveys note complication rates above 60%, primarily due to leakage and aspiration. Each failure triggers urgent clinician visits, inflates cost and deters late adopters. Manufacturers are investing in antimicrobial additives and tapered-edge flanges, but persistent complication fear keeps some patients on electro-larynx alternatives, exerting downward pressure on uptake in the voice prosthesis devices market.

Segment Analysis

By Device Type: Indwelling Valve Dominance Maintains Revenue Base

Indwelling valves represented 73.75% of voice prosthesis devices market share in 2024. The voice prosthesis devices market size tied to this segment is forecast to grow at 5.1% CAGR as upgraded materials push dwell time to a year in controlled cohorts. Indwelling systems demand professional replacement, fitting seamlessly into hospital and specialty-clinic workflows. Non-indwelling devices—posting a 6.05% CAGR—appeal to self-managing patients who value autonomy, especially in markets with robust tele-rehabilitation. Electrolarynx units and emerging 3-D-printed valves fill clinical gaps for anatomies unsuited to standard flanges, but their collective share remains below 5%.

Surgeon-reported primary-puncture success rates hover at 76.2%, climbing to 81.8% for secondary puncture though with higher complications. U.S. insurers reimburse indwelling replacements at three- to six-month intervals, sustaining predictable order cycles. In resource-constrained regions, innovators market budget valves under USD 100, broadening access and buffering volume volatility. These trends collectively ensure indwelling leadership while fostering niche growth vectors, keeping the voice prosthesis devices market diversified yet stable.

Note: Segment shares of all individual segments available upon report purchase

By Valve Type: Provox Series Holds Technological Edge

Provox Series captured 62.30% revenue in 2024, reinforcing the line’s centrality to the voice prosthesis devices market. Upgrades such as Provox Vega reduce speaking effort by 20% and decrease leakage events, making them the default choice in high-volume oncology centres. Blom-Singer Dual Valves grow at 6.47% CAGR, leveraged by special-order lengths and oversized flanges that solve complex leakage cases. ActiValve magnetic options carve a niche among younger, active patients who seek hands-free voicing. Groningen, Aum and regional specialty designs compete on price and locally favoured insertion methods.

Material science drives differentiation: Atos embeds silver oxide, InHealth experiments with tungsten shafts, and European start-ups pilot graphene-reinforced stems. Developers also test Bluetooth-enabled leak sensors that signal smartphones when replacement is due, features already under review by German sickness funds. As these innovations mature, replacement intervals may lengthen, yet higher ASPs preserve revenue, sustaining healthy margins in the voice prosthesis devices market.

By End User: Specialty Clinics Accelerate Procedure Volumes

Hospitals retained 58.31% of the voice prosthesis devices market size in 2024, primarily through initial laryngectomies and primary punctures. Specialty clinics follow close behind, growing 6.91% CAGR as outpatient ENT programs expand. Clinics bundle speech therapy with valve replacement, offering convenience that locks in patient loyalty. Ambulatory surgery centres thrive in the United States, applying modified retrograde techniques that cut facility fees by 35%. Homecare remains embryonic; however tele-coaching and mail-order accessories are emerging support services that encourage adherence.

Value-based bundles are under pilot by Blue Cross plans, paying a fixed amount per six-month care episode inclusive of valve, professional time and rehabilitation. Clinics able to control cost within that envelope stand to gain share, an incentive aligning with payer interest and fuelling clinical throughput in the voice prosthesis devices market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America’s advanced reimbursement environment underpins predictable demand. Medicare’s durable equipment rules authorise two indwelling replacements yearly when leakage or degradation is documented [1]Source: Altavo GmbH, “Series A Financing Announcement,” altavo.com . The United States houses 13 dedicated laryngectomy centres that publish outcome data influential worldwide. Canada’s provincially funded system provides comparable access, and Caribbean patients travel to Florida centres, incrementally enlarging the served population.

Asia-Pacific’s acceleration stems from policy and production. India’s Health Scheme, China’s fast-track approvals and Japan’s super-aged society all expand candidate numbers. Domestic manufacturing cuts landed cost by 40-60%, translating into higher annual replacement adherence. Early detection programs under Healthy China 2030 are set to lift operable tumour counts, further replenishing the user pool for the voice prosthesis devices market.

Europe’s universal systems guarantee access yet negotiate aggressively on price. Germany’s diagnosis-related group refinements add points for endoscopic replacements, improving hospital economics. France’s assurance maladie reimburses devices at retail price, but austerity keeps physicians mindful of cost. The NHS includes valves on its High Cost Tariff Excluded list, sustaining volume while capping reimbursement. Logistics disruptions tied to Brexit have eased, and stock buffers now shield UK patients from shortage risk.

Competitive Landscape

Atos Medical, InHealth Technologies and Coloplast collectively control slightly above 60% of revenue, indicating moderate consolidation. Atos leverages Provox’s clinical heritage, bundles cleaning kits and funds multicentre studies on valve longevity. InHealth differentiates with on-demand custom lengths and variable resistance flanges.

Emerging players focus on niche innovations. Altavo raised EUR 5 million to develop AI-driven “silent speech” software intended to complement mechanical valves[2]Source: Centers for Medicare & Medicaid Services, “Medicare Payment Policy Report,” medpac.gov . APrevent Medical’s injectable VOIS implant aims at glottic insufficiency, yet the firm shares polymer research with valve manufacturers, foreshadowing hybrid solutions. Supply-chain vigilance intensified after FDA spotlighted silicone-component shortages, prompting firms to dual-source moulding in Mexico and Eastern Europe.

Intellectual-property strategies shape pricing. Atos holds patents on dual-valve mechanics until 2032. InHealth’s designs avoid patent conflict by focusing on variable occlusion pressures. European SMEs are poised to exploit expiring legacy patents in 2026, signalling impending price pressure in value segments of the voice prosthesis devices market.

Voice Prosthesis Devices Industry Leaders

-

Andreas Fahl Medizintechnik-Vertrieb GmbH

-

InHealth Technologies

-

ICU Medical Inc.

-

Coloplast A/S (Atos Medical AB)

-

Orbisana Healthcare GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: FDA issued a white paper on medical-device supply-chain vulnerabilities, urging diversification of silicone and magnet suppliers

- February 2024: Altavo secured EUR 5 million Series A funding for AI-based “silent speech” technology

Global Voice Prosthesis Devices Market Report Scope

As per the scope of the report, a voice prosthesis device is an artificial device made of a biocompatible material that allows making sounds by pushing air from the lungs through the valve and up into your mouth. A voice prosthesis is the most common way to restore speech after surgery.

The Voice Prosthesis Devices Market is segmented by Device (Non-Dwelling Voice Prosthesis Devices and In-Dwelling Voice Prosthesis Devices), Valve Types (Provox Series Valves, Blom-Singer Series Valves, ActiValve Magnetic Valves, Groningen Valve, Aum Voice Prosthesis, and Specialty Custom Valves), End-User (Hospitals, Clinics, and Others), and Geography (North America, Europe, Asia-Pacific, and the Rest of the World). The report offers the value (in USD million) for the above segments. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Indwelling Tracheoesophageal Voice Prosthesis |

| Non-Indwelling Tracheoesophageal Voice Prosthesis |

| Electrolarynx / Artificial Larynx Devices |

| Custom 3-D Printed Voice Valves |

| Provox Series Valves |

| Blom-Singer Series Valves |

| ActiValve Magnetic Valves |

| Groningen Valve |

| Aum Voice Prosthesis |

| Specialty Custom Valves (Kapitex, Hood etc.) |

| Hospitals |

| Specialty ENT Clinics |

| Ambulatory Surgery Centers |

| Homecare & Direct-to-Patient Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| Device Type | Indwelling Tracheoesophageal Voice Prosthesis | |

| Non-Indwelling Tracheoesophageal Voice Prosthesis | ||

| Electrolarynx / Artificial Larynx Devices | ||

| Custom 3-D Printed Voice Valves | ||

| Valve Types | Provox Series Valves | |

| Blom-Singer Series Valves | ||

| ActiValve Magnetic Valves | ||

| Groningen Valve | ||

| Aum Voice Prosthesis | ||

| Specialty Custom Valves (Kapitex, Hood etc.) | ||

| End User | Hospitals | |

| Specialty ENT Clinics | ||

| Ambulatory Surgery Centers | ||

| Homecare & Direct-to-Patient Channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

Q1 What is the 2025 value of the voice prosthesis devices market?

A1 The voice prosthesis devices market size is USD 427.56 million in 2025.

Q2 What CAGR is expected for the market through 2030?

A2 The market is projected to grow at a 5.40% CAGR from 2025 to 2030.

Q3 Which device category leads the market?

A3 Indwelling valves hold 73.75% market share and remain the primary revenue driver.

Q4 Which region is growing fastest?

A4 Asia-Pacific is forecast to expand at a 7.39% CAGR owing to improving insurance and local manufacturing.

Page last updated on: