Variable Rate Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

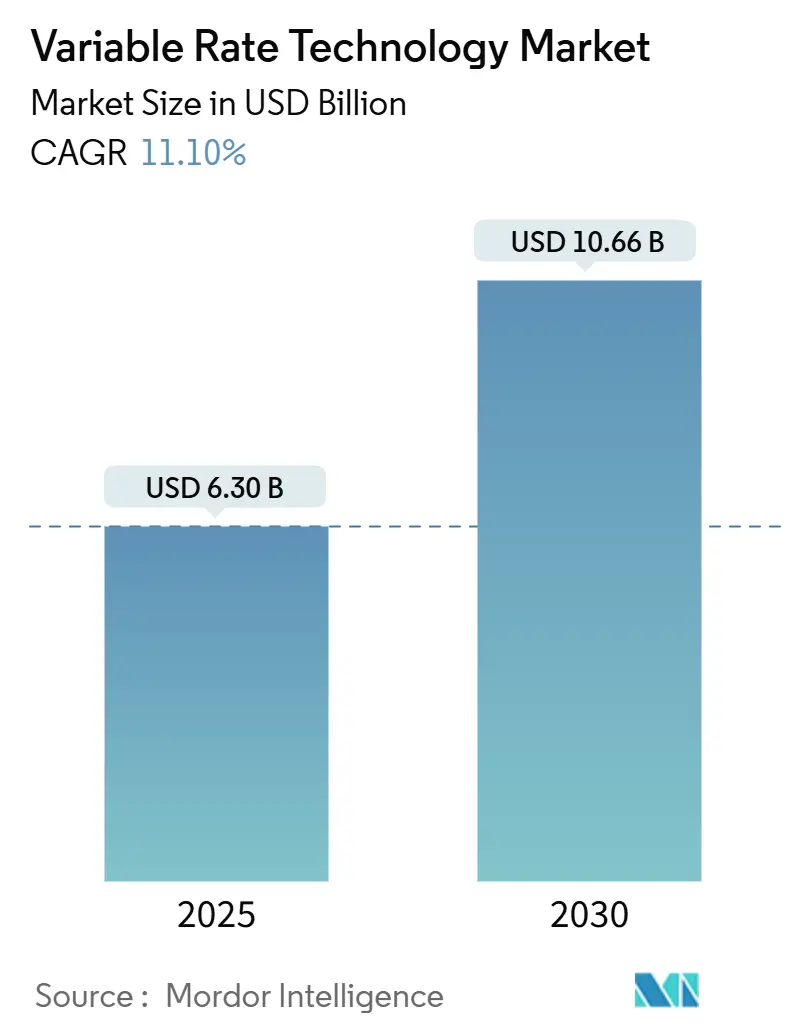

| Market Size (2025) | USD 6.30 Billion |

| Market Size (2030) | USD 10.66 Billion |

| Growth Rate (2025 - 2030) | 11.10% CAGR |

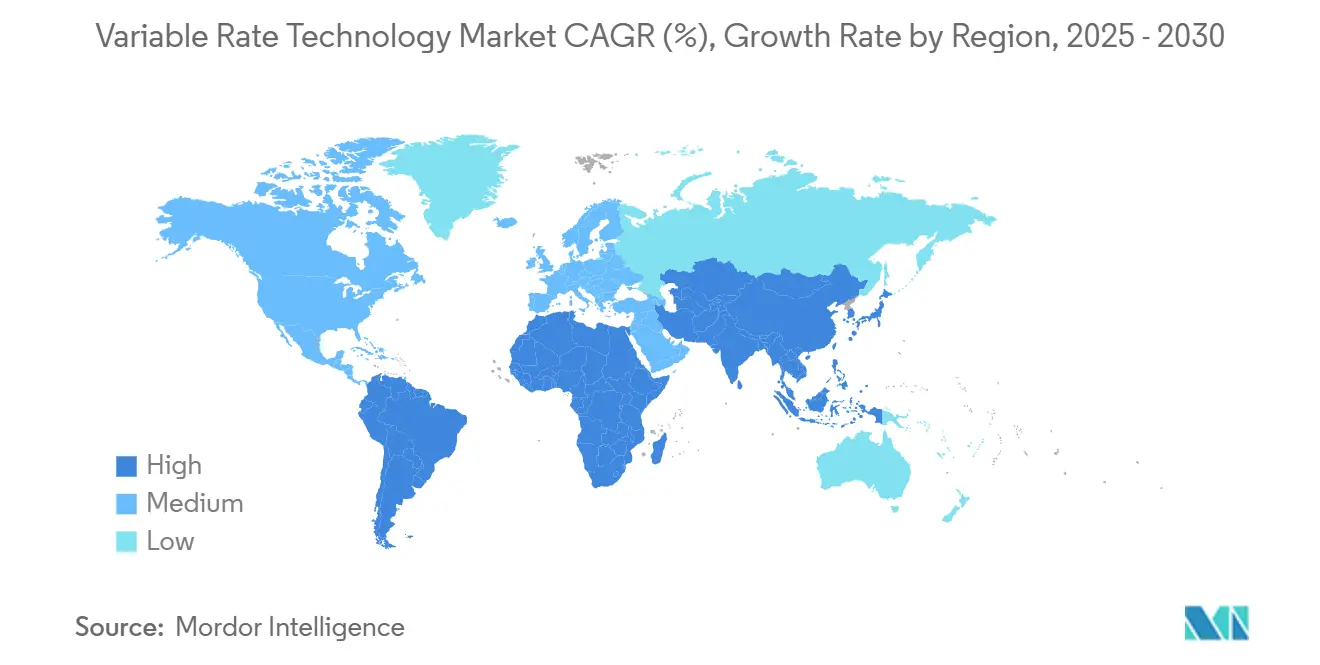

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Variable Rate Technology Market Analysis by Mordor Intelligence

The Variable Rate Technology Market size is estimated at USD 6.30 billion in 2025 and is projected to reach USD 10.66 billion by 2030, at a CAGR of 11.10% during the forecast period. Rising pressure to produce more food with fewer resources, combined with regulatory scrutiny over fertilizer and pesticide use, positions the variable rate technology market as a pivotal enabler of precision input management. Wider farm digitalization, embedded on-equipment AI, and favorable subsidy programs strengthen technology appeal, while consolidation among equipment makers accelerates platform innovation. North America remains the revenue anchor, yet Asia-Pacific contributes the most incremental growth as modernization schemes expand. Hardware sales still dominate value creation, but service-centric business models scale quickly, signaling an industry shift toward outcome-based offerings.

Key Report Takeaways

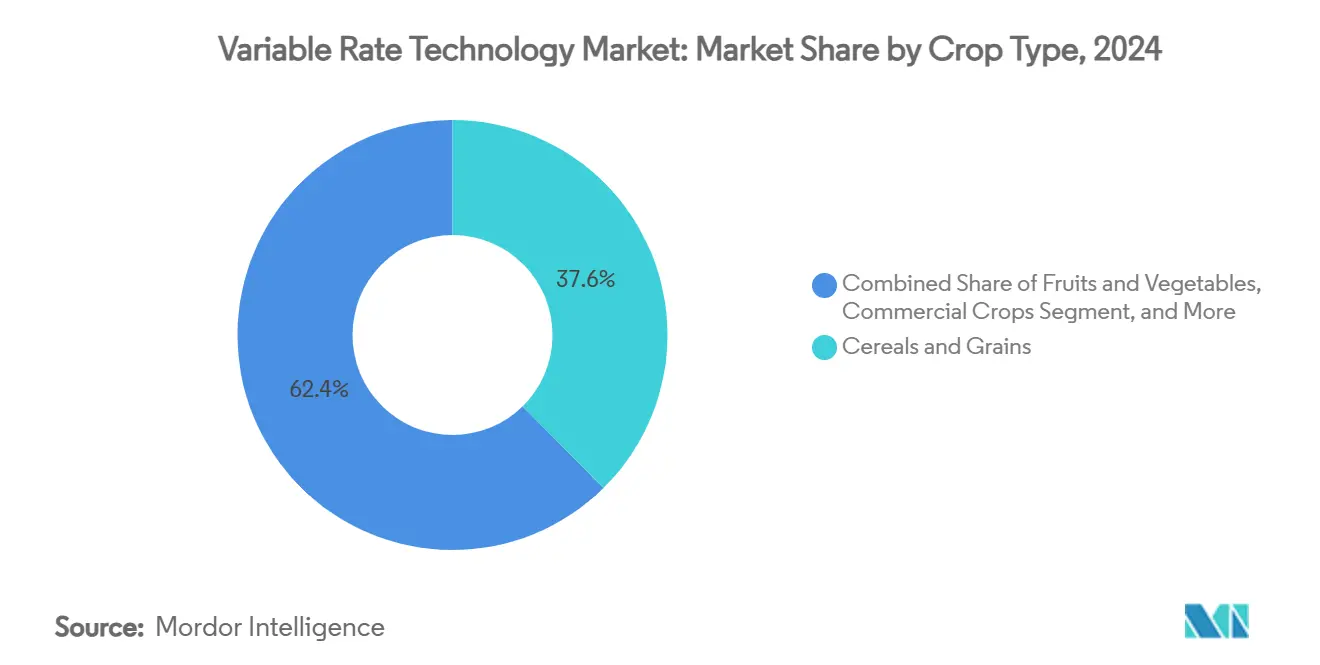

- By crop type, cereals and grains held 37.60% of the variable rate technology market share in 2024; commercial crops are forecast to grow at 14.80% CAGR through 2030.

- By application, fertilizers led with 31.70% revenue share in 2024, while variable-rate irrigation is set to expand at a 17.20% CAGR to 2030.

- By offering, hardware commanded a 56.30% share of the variable rate technology market size in 2024, whereas services are advancing at a 16.40% CAGR through 2030.

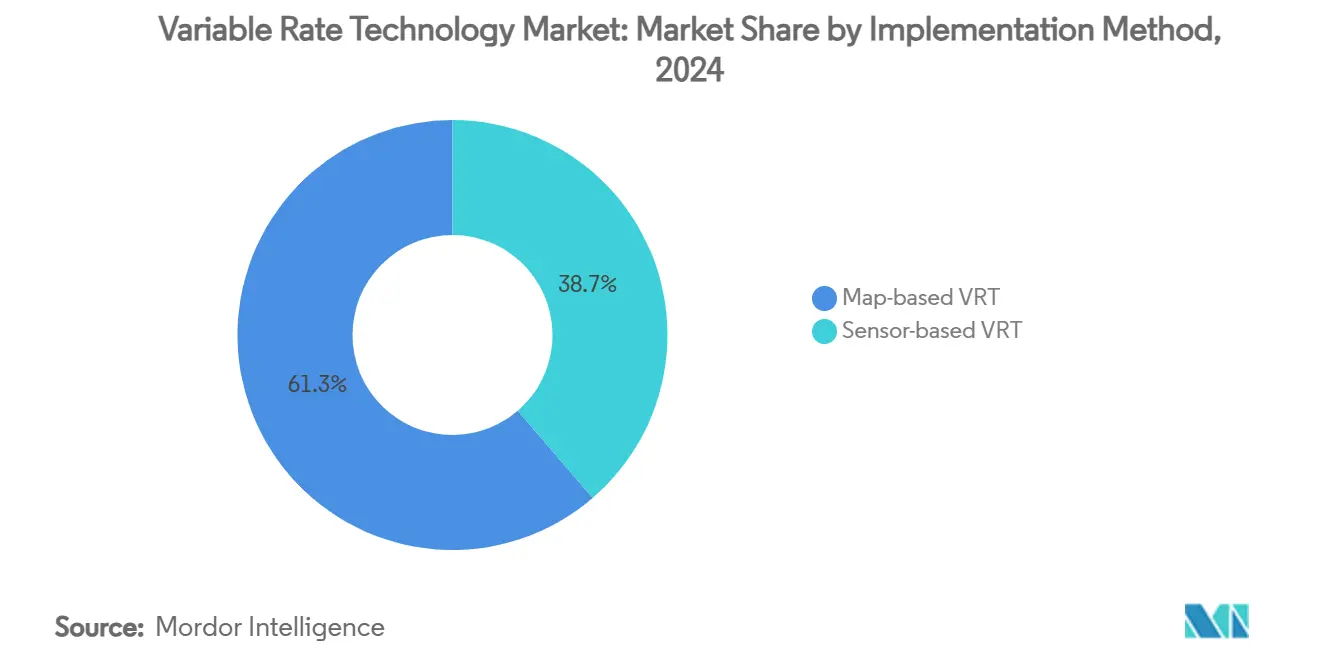

- By implementation method, map-based systems captured a 61.3% share in 2024, while sensor-based approaches are poised for 14.6% CAGR growth.

- By farm size, medium farms accounted for 47.5% of 2024 adoption, yet small farms are projected to rise at 15.2% CAGR through 2030.

- By geography, North America held 39% of the variable rate technology market share in 2024, while Asia-Pacific records the fastest projected growth at 14.1% CAGR through 2030.

Global Variable Rate Technology Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid digitalization of farms | +2.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| Government subsidies and incentive schemes | +2.1% | EU, North America, Asia-Pacific | Short term (≤ 2 years) |

| Rising agricultural labor shortage | +1.9% | North America, Europe, Australia | Long term (≥ 4 years) |

| Satellite NB-IoT-enabled sub-acre prescriptions | +1.6% | Global, accelerating in remote areas | Medium term (2-4 years) |

| Carbon credit monetization demanding input traceability | +1.4% | North America, EU expanding to Asia-Pacific | Long term (≥ 4 years) |

| On-equipment AI chips for offline VRT analytics | +1.2% | Global, first on premium equipment segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Digitalization of Farms

Sixty-one percent of United States farms already rely on precision hardware that feeds real-time agronomic data into cloud platforms.[1]DLL Group, “Global Ag Equipment Trends 2025,” dllgroup.com Equipment makers allocate multibillion-dollar budgets to autonomous solutions that lower labor needs and refine application accuracy, illustrated by John Deere’s decade-long USD 20 billion domestic manufacturing plan. European policy likewise prioritizes an upcoming digital strategy for agriculture, ensuring sustained funding for connected devices. Closed feedback loops created by AI-driven algorithms continuously adjust prescriptions, moving the variable rate technology market beyond static maps toward self-learning systems. Yet a widening digital divide between large and small farms threatens equitable technology uptake.

Government Subsidies and Incentive Schemes

Policymakers use grants, rebates, and eco-schemes to underwrite adoption costs. The USDA Climate-Smart Commodities initiative channels USD 3.1 billion into projects that necessitate granular production data and, by extension, precision input tools.[2]United States Department of Agriculture, “Climate-Smart Commodities,” usda.gov Australia’s On-Farm Connectivity Program covers half the cost of smart irrigation devices, while India’s Digital Agriculture Mission earmarks INR 6,000 crore (USD 722.89 million) for connected infrastructure. Europe’s Common Agricultural Policy directs at least 25% of direct payments toward eco-schemes that reward variable-rate fertilization. These subsidies lower entry barriers, especially for mid-size farms whose cash flows were once restricted by high-tech spending.

Rising Agricultural Labor Shortage

Persistent worker deficits lift automation from a discretionary upgrade to an operational necessity. Field-level robotics now pairs with rate controllers so one operator can supervise multiple machines while maintaining optimal input levels. Satellite broadband arrangements such as John Deere-Starlink furnish the always-on connectivity required for uncrewed operations. The resulting service demand helps explain the double-digit growth projected for variable-rate technology market services.

Satellite NB-IoT–Enabled Sub-Acre Prescriptions

Partnerships between space and telecom firms deliver a narrowband spectrum to remote croplands, removing a historic bottleneck for real-time prescriptions. OQ Technology and Deutsche Telekom now market a 5G IoT service tailored for rural sensors that updates moisture, nutrient, and stress metrics every few minutes. Active satellite IoT connections in farming are on track to double by 2029, directly expanding the addressable variable rate technology market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure of VRT-ready machinery | -2.3% | Global, most acute for small and medium farms | Short term (≤ 2 years) |

| Patchy rural connectivity infrastructure | -1.8% | Emerging markets, rural North America, remote EU regions | Medium term (2-4 years) |

| Data ownership and sharing ambiguities | -1.2% | Europe, North America | Medium term (2-4 years) |

| Shortage of VRT skilled agronomic service providers | -1.0% | Asia-Pacific, Africa, parts of Eastern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure of VRT-Ready Machinery

Profitability breakeven often starts at economic farm sizes above EUR 100,000 (USD 114,923.51), leaving smaller operations priced out of equipment purchases. Lenders such as AgDirect offer sector-specific loans, yet collateral hurdles persist for family farms with thin balance sheets. As a workaround, equipment-as-a-service contracts spread costs across acres serviced rather than units owned.

Patchy Rural Connectivity Infrastructure

Only one-quarter of United States farms connect machines to the cloud because broadband gaps linger despite federal grants. Manufacturers, therefore, integrate satellite receivers, and CNH Industrial now bundles Intelsat coverage with Raven application controls. Edge computing solutions mitigate dead zones but curb benefits tied to multi-farm data pooling.

Segment Analysis

By Crop Type: Commercial crops outpace staples

In 2024, cereals and grains represented 37.60% of revenues, cementing their role as the foundation of the variable rate technology market. These broad-acre crops benefit from decades of prescription mapping that fine-tunes nitrogen, phosphorus, and seeding density across large tracts. Commercial crops such as cotton, tobacco, and specialty fibers deliver the fastest gains with a 14.80% CAGR outlook, as higher margins justify premium sensors and on-equipment AI. Variable rate technology market size for commercial crops is anticipated to climb in tandem with quality-linked pricing schemes that reward precise micronaire or leaf grade. Continuous monitoring of plant stress via multispectral cameras feeds real-time models that initiate potassium or foliar-feed interventions within minutes. This responsiveness helps producers capture contract bonuses and reduce grade-related downgrades. Cereals will keep anchoring installed base volumes, yet specialty segments set the pace for advanced feature uptake.

Second-generation soil spectroscopy now measures nutrient release curves that underpin fertilizer micro-dosing in oilseed and pulse rotations. Adoption is especially strong in Brazil and India, where protein and oil content directly influence farm-gate prices. The variable rate technology market further penetrates orchard and vineyard operations as fruit exporters demand tighter Brix and color tolerances. Providers bundle sap analysis and irrigation rate control into subscription services so smaller acreage fruit farms can access high-end analytics without outright equipment purchases.

Note: Segment shares of all individual segments available upon report purchase

By Application: Irrigation leads acceleration

Fertilizers held a 31.70% market share in 2024 because nitrogen efficiency improvements deliver quick paybacks in most climatic zones. Variable-rate irrigation is poised for a 17.20% CAGR by 2030, reflecting escalating water scarcity and regulatory caps on seasonal withdrawals. In California trials, precision pivots cut water use by 25% with no yield penalty[3]Valmont Industries, “Water Savings with Variable Rate Irrigation,” valleyirrigation.com, validating the economics for almond and pistachio groves. The variable rate technology market size for irrigation equipment is forecast to add USD 1 billion in incremental sales by 2030, buoyed by subsidy programs that reimburse low-pressure nozzle retrofits. Crop-protection spraying follows close behind as computer-vision weed identification slashes herbicide volumes by up to 80%. Added to these gains, yield monitoring applications complete the data feedback loop that refines future prescriptions and anchors subscription renewals for analytics software.

Integration of wireless soil probes with cloud dashboards enables irrigation decisions that account for evapotranspiration forecasts and future rainfall probability. This predictive capability extends pump life and trims energy demand, reinforcing the resource-efficiency value proposition. Fertilizer applications now leverage real-time tissue testing via portable lab kits that sync to rate controllers, converting static maps into season-long dynamic schedules. Product innovation in biological crop-protection inputs further amplifies the need for precise micro-dosing that hinges on sensor-driven variable rate algorithms.

By Offering: Services unlock recurring revenue

Hardware retained a 56.30% share in 2024 through steady combine and sprayer sales, yet the services arm of the variable rate technology market is climbing at 16.40% CAGR as growers favor guaranteed outcomes over asset ownership. Dealers now provide agronomic audits, data cleansing, prescription generation, and in-season monitoring under per-acre contracts. This pivot stabilizes cash flow for manufacturers and reduces decision complexity for farmers. Integrated dashboards blend weather, soil, and machine health data so agronomists can adjust rates remotely, shrinking labor demands on farm staff. Variable rate technology industry participants increasingly offer tiered service bundles that include hardware maintenance, over-the-air software updates, and regulatory reporting modules.

Software layers supply the connective tissue across mixed fleets, demonstrated by AGCO’s Fuse platform and the newly formed PTx Trimble joint venture that focuses on retrofit solutions. This open-architecture push broadens addressable acres because older equipment can now access modern rate control without full tractor replacements. Service contracts also address data privacy fears by stipulating ownership clauses and encryption standards, reassuring growers who previously hesitated to share field analytics.

By Implementation Method: Sensors narrow the gap

Map-based VRT workflows accounted for 61.3% of deployments in 2024, a legacy of yield mapping and soil sampling practices that dominated the first precision agriculture wave. Sensor-based VRT systems are catching up fast at 14.6% CAGR as multispectral cameras, chlorophyll meters, and soil probes fall in price. Field-mounted optics read canopy reflectance to gauge nitrogen status, feeding immediate side-dress commands to rate controllers.

Hybrid approaches merge historical yield maps with real-time sensor data, improving prescription accuracy in variable weather years. The variable rate technology market, therefore, transitions from static planning toward autonomous adjustment powered by machine-learning inference within implementations. Edge computing chips now process high-resolution video streams locally, eliminating latency even when cellular networks fail. As connectivity expands, cloud synchronization allows cross-field benchmarking that refines algorithms for future seasons.

By Farm Size: Democratization accelerates

Medium farms between 200 and 1,000 hectares owned 47.5% of the installed systems in 2024 because their scale justifies capital spending while still allowing owner-operator control. Yet the highest growth lies with smaller farms under 200 hectares, which will expand adoption at 15.2% CAGR as cooperative models and financing tools mature.

Variable rate technology market share growth in this tier is supported by equipment rental pools, dealer-managed custom applications, and smartphone dashboards that reduce technical complexity. Large enterprises remain technology pioneers, integrating autonomous tractors, drone fleets, and AI-driven supply chain traceability to defend thin commodity margins. Regulators now recognize smallholder inclusion as critical for national sustainability targets, prompting grant programs that offset setup costs and sponsor precision-ag apprenticeships.

Geography Analysis

North America generated 39% of 2024 revenue for the variable rate technology market. Strong machinery penetration, supportive financing, and USDA climate-smart procurement rules anchor demand. Subsidy frameworks reward documented nutrient reductions, spurring the adoption of smart implements that capture nozzle-level logs. Rural broadband lags in parts of the Midwest and Prairie provinces, yet satellite link rollouts promise coverage boosts by 2026. Ohio State trials show a 6% yield lift when VR nitrogen intersects with drone stand counts, proof points that validate ongoing investment. Dealer ecosystems supply certified technicians who maintain fleets and interpret data, underscoring the service growth narrative.

Asia-Pacific is the fastest climber, tracking a 14.1% CAGR to 2030 as governments attach digital farming clauses to modernization spending. China’s latest Five-Year Plan promotes low-carbon, high-efficiency agriculture that dovetails with targeted input delivery. India’s Aadhaar-linked Farmer Registry simplifies subsidy disbursement for sensor kits, while Japan’s Food and Agriculture Ministry co-funds paddy-specific variable rate seeding trials. The region’s small-plot structure sparks creative solutions, including shared-service drones operated by village entrepreneurs. Water scarcity across Australia and Northern China accelerates variable-rate irrigation uptake, driving cross-border knowledge transfer and hardware imports.

Europe embeds variable rate technology adoption within sweeping climate policy. The Common Agricultural Policy for 2023-27 allocates EUR 269.5 billion (USD 312.4 billion), nearly half aimed at climate objectives that include reduced fertilizer leaching and pesticide drift. Each member state must earmark at least 25% of direct payments for eco-schemes, many of which list precision application as a qualifying practice. Countries such as the Netherlands fund digitization grants that reimburse up to 40% of sensor installations, hastening implementation. Data sovereignty rules raise compliance costs as platforms adapt to General Data Protection Regulation obligations. Nonetheless, consortium projects like Germany’s 5G Testbed Agriculture expedite confidence in secure connectivity, and Pan-European carbon initiatives depend on traceable input data generated by rate controllers.

Competitive Landscape

The variable rate technology market exhibits moderate concentration, with five leaders holding a 62% share. Deere & Company secures 22% through integrated hardware, AI vision, and cloud analytics that run across its Operations Center. It's See & Spray Premium identifies weeds in green-on-green settings and instantly modulates herbicide flow, cutting chemical spending while creating verifiable compliance logs. AGCO commands 15.5% after launching the PTx Trimble venture that supplies retrofit rate control to mixed fleets, opening new revenue from aging tractors.

CNH Industrial leverages Raven Industries’ controllers plus Intelsat connectivity to cement its 12% position. Variable-rate irrigation specialists Valmont and Lindsay round out the top tier, owning 7% and 5.5%, respectively, through Valley and FieldNET smart pivots. Strategic themes revolve around vertical integration, platform openness, and autonomous capability. Deere’s acquisition of Sentera adds drone imagery that feeds smart-spraying algorithms, while CNH’s business plan doubles Precision Tech's revenue share by 2030 through sensor-rich implements.

Start-ups such as EarthOptics and Pattern Ag merge to provide soil-digital-twin subscriptions that challenge equipment-centric incumbents. Manufacturers also execute partnership playbooks: John Deere aligns with Starlink for broadband, AGCO dealers merge to enlarge service footprints, and Phytech teams with Rivulis and Netafim to blend plant sensors with irrigation. Competitive intensity rises, yet scale advantages in Research and Development and distribution still favor established players, keeping market concentration moderate.

Variable Rate Technology Industry Leaders

-

Deere & Company

-

AGCO Corporation

-

CNH Industrial N.V.

-

Lindsay Corporation

-

Valmont Industries, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: John Deere acquired Sentera to integrate aerial crop data with See & Spray systems, enabling precise weed frameworks.

- January 2025: Valmont Industries unified four platforms into the AgSense 365 app to streamline variable-rate irrigation management.

- August 2024: EarthOptics and Pattern Ag have merged to deliver high-resolution soil data and predictive analytics, enabling variable-rate fertilization and tillage prescriptions.

- April 2024: AGCO Corporation acquired an 85% stake in Trimble's agricultural assets and technologies portfolio for USD 2.0 billion in cash, while Trimble retained a 15% stake. Trimble provides agricultural technology solutions, including variable rate technology.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the variable rate technology (VRT) market as all hardware, software, and connected services that actively change the on-field rate of crop inputs such as seed, fertilizer, irrigation, and crop-protection chemicals by using prescription maps or real-time sensors across agricultural land. According to Mordor Intelligence, map-based and sensor-based systems sold as factory-fit units, retrofit kits, or SaaS bundles are included, while revenue from generic farm-management platforms without rate-control capability is left out.

We purposely exclude income earned solely by custom contracting service operators.

Segmentation Overview

- By Crop Type

- Cereals and Grains

- Fruits and Vegetables

- Oilseeds and Pulses

- Commercial Crops

- By Application

- Fertilizers

- Crop-protection Chemicals

- Soil Sensing

- Yield Monitoring

- Irrigation

- Others (variable-rate seeding/planting, variable-rate lime and soil-amendment application)

- By Offering

- Hardware

- Software

- Services

- By Implementation Method

- Map-based VRT

- Sensor-based VRT

- By Farm Size

- Large Farms (greater than 1,000 ha)

- Medium Farms (200-1,000 ha)

- Small Farms (less than 200 ha)

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Turkey

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview agronomists, equipment dealers, sensor makers, and large growers across North America, Europe, Latin America, and Asia-Pacific. We've found these conversations clarify regional incentives, realistic selling prices, and replacement cycles, filling gaps left by secondary data and anchoring key assumptions.

Desk Research

We start with public data from the USDA, FAO, Eurostat, the International Fertilizer Association, and similar bodies to size planted acreage, input intensity, and guidance-equipped machinery fleets. Trade statistics, patent filings, scientific journals, and investor presentations then refine adoption curves and price corridors. Counts are cross-checked through paid databases including D&B Hoovers for company financials and Dow Jones Factiva for shipment trends, plus focused sources such as Marklines for tractor electronics and Questel for sensor patents. We're mindful that the list above is illustrative; many additional publications inform the desk work.

Market-Sizing & Forecasting

A top-down model converts cultivated hectares and average input spend into a demand pool, then applies VRT penetration rates gathered from research. Select bottom-up checks, such as dealer roll-ups and sampled average selling price multiplied by unit shipments, tighten the totals. Core variables include precision-capable tractor penetration, sensor cost curves, fertilizer price index moves, harvested-crop margin trends, and acreage under sustainability-linked subsidies. Multivariate regression projects each driver through 2030 and creates low, base, and high scenarios; missing bottom-up evidence is bridged with regional proxy ratios agreed during interviews.

Data Validation & Update Cycle

Outputs pass variance checks against historical equipment shipments and input-use statistics. Senior analysts review anomalies and re-query sources when swings exceed two standard deviations. Reports refresh annually, and interim updates follow material policy or weather shocks so clients receive the latest view.

Why Mordor's Variable Rate Technology Baseline Earns Confidence

Published estimates often diverge because firms pick different product mixes, currency years, and refresh cadences. Our disciplined scope and annual recalibration keep those drifts modest.

Key gap drivers include whether ancillary guidance systems are counted, the year chosen for currency conversion, assumed retrofit replacement cycles, and the aggressiveness used when modeling future acreage under precision-farming subsidies.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.30 B (2025) | Mordor Intelligence | |

| USD 9.34 B (2024) | Global Consultancy A | counts generic farm software and multi-industry dosing tools |

| USD 4.29 B (2024) | Industry Association B | omits retrofit hardware and sensor subscriptions |

| USD 4.00 B (2022) | Regional Consultancy C | uses an older base year and static currency rates |

The comparison shows that Mordor's balanced scope, variable-driven forecasts, and active refresh cycle deliver a dependable baseline that decision-makers can trace to clear drivers and repeatable steps.

Key Questions Answered in the Report

What is the current size of the variable rate technology market?

The market is valued at USD 6.3 billion in 2025 and is forecast to reach USD 10.66 billion by 2030.

Which segment will grow the fastest through 2030?

Variable-rate irrigation is projected to post a 17.20% CAGR, the highest among all application areas.

Why are services expanding faster than hardware sales?

Farmers increasingly prefer outcome-based contracts that bundle analytics, custom application, and equipment maintenance, pushing services to a 16.40% CAGR.

How are governments supporting adoption?

Programs such as the USDA Climate-Smart Commodities initiative and EU eco-schemes provide grants and direct payments that offset technology investment costs. Programs such as the USDA Climate-Smart Commodities initiative and EU eco-schemes provide grants and direct payments that offset technology investment costs.

Page last updated on: