Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

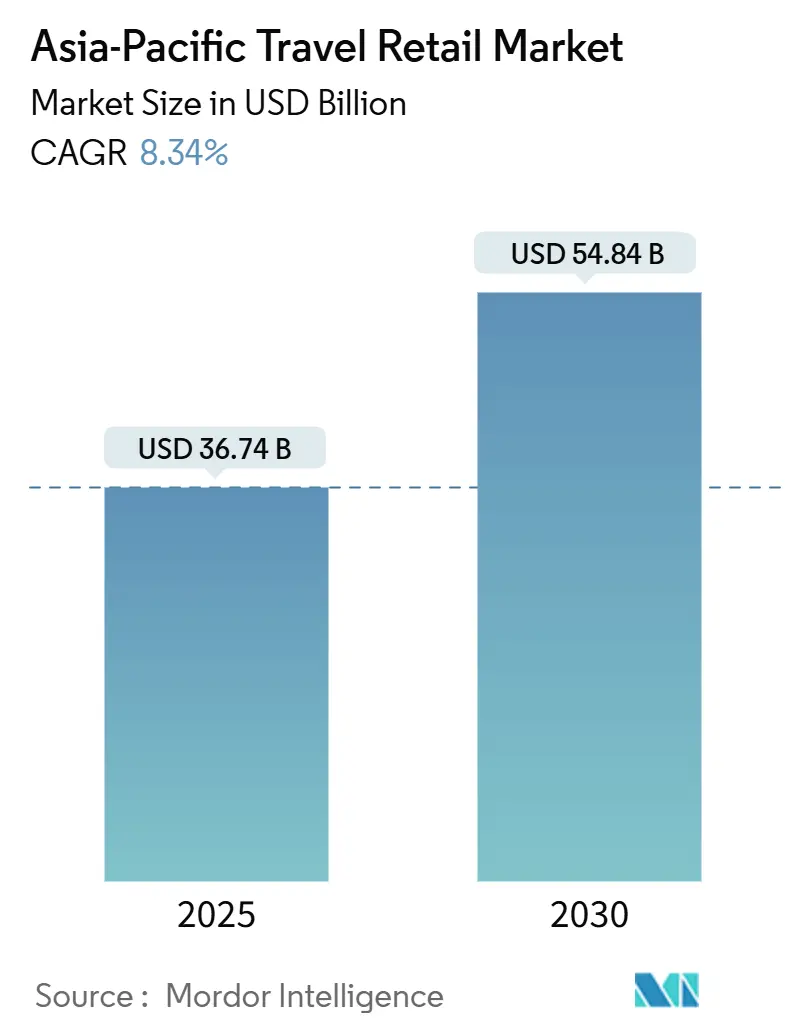

| Market Size (2025) | USD 36.74 Billion |

| Market Size (2030) | USD 54.84 Billion |

| Growth Rate (2025 - 2030) | 8.34% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Travel Retail Market Analysis by Mordor Intelligence

The Asia-Pacific travel retail market size stood at USD 36.74 billion in 2025 and is projected to reach USD 54.84 billion by 2030, corresponding to an 8.34% CAGR across the forecast period. Strong aviation and rail recovery, liberalized visa regimes, and infrastructure upgrades are expanding passenger volumes and reshaping shopping behaviours toward experiential purchases rather than status-driven luxury. China’s visa-free push and India’s surging outbound traffic are channelling a new wave of high-propensity shoppers who outspend pre-pandemic cohorts on fragrances, cosmetics, and niche wines. Airport operators are designing dwell-time-rich terminals, while retailers embed click-and-collect platforms that fuse digital discovery with on-site fulfilment. Although currency swings and geopolitical frictions inject short-term volatility, long-run growth fundamentals remain intact as ASEAN duty-free harmonization and high-speed rail investments widen the Asia-Pacific travel retail market’s geographic reach.

Key Report Takeaways

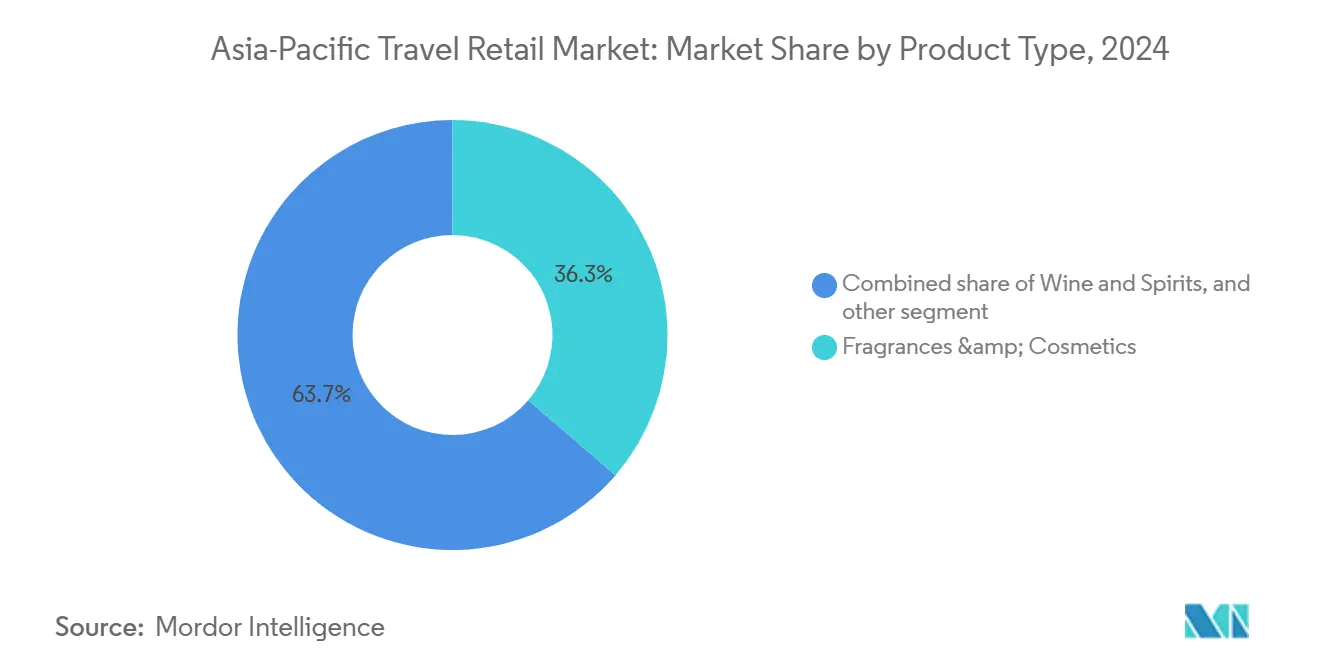

- By product category, fragrances and cosmetics led with 36.33% revenue share of the Asia-Pacific travel retail market in 2024, while wines and spirits are forecast to expand at a 12.65% CAGR through 2030.

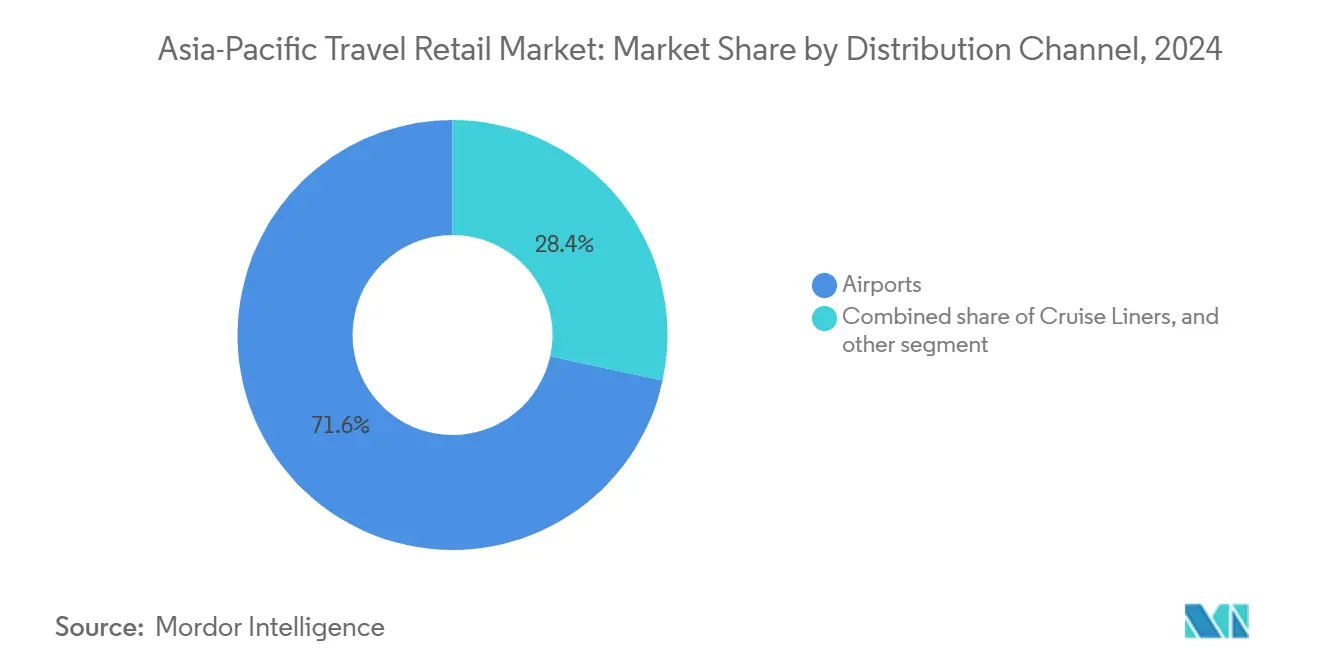

- By distribution channel, airports accounted for 71.64% of the Asia-Pacific travel retail market share in 2024, whereas railway stations are projected to record a 15.34% CAGR to 2030.

- By traveller demographic, leisure travellers held 52.37% of the Asia-Pacific travel retail market in 2024; medical and wellness tourists are set to rise at a 14.83% CAGR through 2030.

- By geography, China commanded 45.76% of the Asia-Pacific travel retail market size in 2024, while India is projected to post the fastest 13.32% CAGR between 2025 and 2030.

Asia-Pacific Travel Retail Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in outbound Chinese tourism after visa relaxations | +2.1% | China, ASEAN core, spill-over to Japan and Australia | Short term (≤ 2 years) |

| Expansion of low-cost carriers across secondary airports | +1.8% | Global, with a concentration in Southeast Asia and India | Medium term (2-4 years) |

| Rising disposable incomes & luxury appetite in Southeast Asia | +1.5% | Southeast Asia core, extending to emerging Asia-Pacific markets | Long term (≥ 4 years) |

| Large-scale airport & terminal expansions (India, Vietnam) | +1.2% | India, Vietnam, with regional connectivity benefits | Medium term (2-4 years) |

| Pre-order & click-collect platforms boosting conversion | +0.9% | Global, led by tech-advanced markets like Singapore, Japan | Short term (≤ 2 years) |

| ASEAN duty-free allowance harmonisation | +0.7% | ASEAN member states, cross-border trade facilitation | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Outbound Chinese Tourism After Visa Relaxations

China granted visa-free entry to travellers from 74 nations, resulting in 20.115 million visa-free arrivals in 2024, a 112.3% annual leap [1]Global Times, “China Records 20.115 m Visa-Free Entries in 2024,” globaltimes.cn . Chinese outbound trips are forecast to approach 130 million by year-end, reviving passenger flows across ASEAN and Pacific gateways. Chinese travellers have consistently demonstrated high spending per trip when traveling abroad. Projections indicate that they are likely to allocate increased discretionary budgets for international travel in 2025, reflecting a strategic shift in their spending behaviour and priorities. Retailers that pivot toward experience-centric bundles, spa vouchers, cultural tours, and chef-led tastings align with shifting preferences away from conspicuous luxury. Secondary destinations such as Da Nang and Cairns benefit from overflow as tier-one hotspots reach capacity, broadening the Asia-Pacific travel retail market footprint.

Expansion of Low-Cost Carriers Across Secondary Airports

Low-cost carriers (LCCs) account for 30% of the total seat capacity in the Asia-Pacific region, demonstrating significant penetration in several domestic markets. This highlights the growing influence of LCCs in shaping the competitive dynamics of the regional aviation industry [2]Centre for Aviation, “LCCs in Asia Pacific,” centreforaviation.com . New nonstop links between tier-two cities, Lucknow to Kuala Lumpur, Da Nang to Seoul, democratize air travel and direct retail demand toward untapped airports. Secondary hubs offer a cost-effective environment for operators by charging lower concession fees. This enables businesses to test and implement compact store formats and kiosk concepts without incurring the high overhead costs typically associated with premium locations. Shopper profiles skew younger and value-driven, catalysing demand for competitively priced beauty minis, craft snacks, and digital promotions. The geographic dispersion boosts resilience by lowering overreliance on mega-hubs within the Asia-Pacific travel retail market.

Rising Disposable Incomes in Southeast Asia

The rise in middle-income households across Southeast Asia in 2024 significantly influenced consumer behaviour, leading to increased discretionary spending on premium categories such as travel and beauty products. Mass-affluent millennials favour authentic labels over logo-heavy goods, lifting demand for regional designers and limited-run collaborations. Luxury beauty sales rose 11% region-wide and are projected to triple to USD 7.6 billion by 2026. Retailers leverage cultural events, Songkran, Hari Raya, and Lunar New Year, to run pop-ups that blend local storytelling with global brands. Government-backed tourism corridors in Thailand and Indonesia channel affluent traffic into new commercial precincts, expanding the Asia-Pacific travel retail market’s premium base.

Large-Scale Airport & Terminal Expansions (India, Vietnam)

Vietnam’s USD 13.38 billion Long Thanh International Airport will welcome 25 million annual passengers in Phase 1 and rank among the world’s top hubs by the mid-2030s [3]VnExpress, “Long Thanh Airport to Welcome First Commercial Flights,” vnexpress.net . Kempegowda International Airport in India has committed an investment of USD 2 billion to enhance its infrastructure, aiming to expand its passenger handling capacity to 100 million. This strategic move aligns with the airport's long-term growth objectives and reflects its efforts to cater to increasing air travel demand in the region. Modern designs dedicate more leasable space to retail, install AI-enabled flow systems, and embed contactless payment nodes. Early-bird tenants secure prime frontage, co-plan omnichannel services, and lock in long lease tenures that hedge against rent inflation. These mega projects expand the Asia-Pacific travel retail market size by injecting fresh real estate and higher-spending traffic.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High concession fees are squeezing retailer margins | -1.4% | Global, particularly premium airports in Singapore, Hong Kong | Short term (≤ 2 years) |

| Stricter tobacco-marketing regulations | -0.8% | Asia-Pacific core, following the WHO Framework Convention guidelines | Medium term (2-4 years) |

| FX volatility is impacting pricing parity | -0.6% | Japan, Australia, and emerging markets with currency instability | Short term (≤ 2 years) |

| "Travel-light" trend reducing impulse purchases | -0.5% | Global, led by younger demographics and sustainable travel advocates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Concession Fees Squeezing Retailer Margins

Market operators are strategically reallocating capital toward secondary gateway locations, leveraging the benefits of lower fee structures and reduced competitive pressures to optimize profitability. Collaborative efforts, such as forming joint ventures with airport authorities and implementing hybrid rent models linked to passenger traffic volumes, are becoming key approaches to effectively balance and mitigate operational risks. Additionally, the adoption of advanced technologies, including AI-driven demand forecasting, self-checkout systems, and robotic stock replenishment processes, is enabling significant reductions in operating costs per square foot while improving operational efficiency. In the Asia-Pacific travel retail market, consolidation dynamics are accelerating as midsize companies actively seek scale expansion to absorb fee-related shocks, enhance resilience, and strengthen their competitive positioning in a rapidly evolving market landscape.

Stricter Tobacco-Marketing Regulations

WHO-aligned controls are shrinking a category that once drove double-digit profit shares. Plain-pack laws, nicotine caps, and display bans sweep across Japan, South Korea, and Australia. Heated tobacco, dominant in Japan, faces fresh location-use restrictions, while South Korean exceptions create cross-border arbitrage risks. Retailers pivot to premium spirits, wellness supplements, and craft confectionery, but gross margins compress compared with tobacco’s historical highs. Compliance costs mount for staff training and POS upgrades, yet reputational alignment with health goals may entice wellness-minded travellers over time.

Segment Analysis

By Product Type: Premiumization Drives Category Evolution

Fragrances and cosmetics captured 36.33% of 2024 sales, buoyed by livestream tutorials, AR shade-matching kiosks, and travel-exclusive gift sets that convert browsers into buyers. The Asia-Pacific travel retail market share of wines and spirits is climbing fastest at a 12.65% CAGR, fuelled by millennials chasing single-malt whiskies and small-batch gin rarities. Tobacco’s share continues to retreat amid compliance headwinds, though limited-edition cigars retain a loyal niche. Food and confectionery thrive on gifting norms—mooncake trios, matcha truffles, bird’s-nest snacks—that drive impulse purchases. Fluctuations in the yen and yuan have created opportunities for downtown retailers to strategically leverage duty-free price differentials. This trend has particularly benefited the "other product types" category, which includes electronics, watches, and jewellery, as these products continue to attract consumer demand despite currency volatility. AI-driven forecasting tools refine SKU selections, lifting shelf productivity and preserving working capital, while “Asia only” collaborations elevate discovery appeal inside the Asia-Pacific travel retail market.

The premiumization wave also expands basket sizes as travellers trade up to niche perfumes, clean-label skincare, and single-vineyard wines. Brands build immersive installations, AR fragrance caves, mixology counters, that generate social-media buzz and data capture opportunities. Retailers diversify supplier bases to include artisanal chocolatiers, eco-friendly sunscreen lines, and K-wellness tonics, refreshing the assortment cycle. Category managers measure success not solely by unit velocity but by Instagram impression lift and loyalty-app re-engagement. This fusion of storytelling and analytics cements premium sectors as core engines of Asia-Pacific travel retail market growth.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Infrastructure Modernization Reshapes Access Points

Airports are projected to maintain their dominant position, contributing 71.64% of the total revenue in 2024. This dominance is anticipated to persist through 2030, driven by strategic initiatives such as the expansion of retail real estate and the adoption of advanced AI-powered crowd-flow management systems. These developments are expected to enhance operational efficiency and revenue generation capabilities within the airport segment. Average dwell times in newly established terminals are measured in minutes, offering retailers multiple touchpoints to strategically influence consumer purchasing decisions and enhance conversion rates. Railway stations are the breakout channel, growing at a 15.34% CAGR, propelled by China’s 47,000 km high-speed grid and India’s fast-building corridors. Station outlets target commuters with smaller formats, frictionless payment pods, and local souvenir walls.

Cruise liners primarily target high-income leisure travellers through week-long voyages, generating significantly higher per-capita spending compared to air travellers. However, despite this higher spending potential, cruise liners account for a relatively smaller proportion of the Asia-Pacific travel retail market size, highlighting an opportunity for growth within this segment. Border-crossing and ferry terminals cater to budget tourists and business commuters seeking regulatory price differentials on health supplements and local crafts. Omnichannel ecosystems unify inventory pools across channels, letting travellers reserve online and pick up at their preferred node. Integrated mobility hubs co-locating rail, air, and bus facilities promise future synergies for single-checkout journeys.

Note: Segment shares of all individual segments available upon report purchase

By Traveler Demographics: Medical Tourism Drives Segment Growth

Leisure travellers retained a 52.37% share in 2024, supplying baseline volume and sustaining category diversity. Seasonal peaks coincide with school holidays, Golden Week, and Diwali breaks, requiring agile staffing and real-time inventory updates. Medical and wellness tourists are expanding fastest at 14.83% CAGR, attracted by Thailand’s USD 34.6 billion wellness ecosystem and Vietnam’s 300,000 international patients annually. They stay longer, spend more on clean beauty, vitamins, and ergonomic luggage, and show higher loyalty to personalized service. Business travellers appreciate speed and predictability, relying heavily on pre-order apps and fast-track pick-up lockers.

Visiting friends and relatives (VFR) travellers drive gift-oriented purchases, regional sweets, health tonics, silk scarves, while students favour tech accessories and affordable skincare minis that fit cabin-bag allowances. Demographic segmentation informs targeted promotions: wellness bundles for medical tourists, limited-edition snacks for VFR shoppers, and study-abroad starter kits for students, maximizing conversion across the Asia-Pacific travel retail market.

Geography Analysis

China commanded a 45.76% share in 2024, underpinned by 20.115 million visa-free arrivals and downtown duty-free reforms in eight megacities. Passenger volumes concentrate around tier-one airports, yet provincial hubs in Hainan, Chengdu, and Xi’an are scaling duty-free capacity, diluting geographic risk. Chinese shoppers increasingly value experiences, propelling sales of cultural craft kits, local coffee beans, and theme-park tickets alongside premium cosmetics. Currency swings influence category mix: yuan softness bolsters outbound shopping, while strength favours domestic spending patterns inside the Asia-Pacific travel retail market.

India emerges as the fastest-growing geography with a 13.32% CAGR to 2030, lifted by a rising middle class and airport megaprojects that enhance capacity and shopper comfort. Indian consumers spend heavily on perfumes, whiskey, and gold jewelry, creating fertile ground for loyalty-app upsells and co-branded payment incentives. Government schemes such as “Dekho Apna Desh” ignite domestic tourism, boosting spend at internal duty-paid outlets and supporting a 360-degree Asia-Pacific travel retail market ecosystem.

Japan hosted a record 36.9 million visitors in 2024 who spent 8.1 trillion yen (USD 54.06 billion) despite yen volatility, cementing its allure for Korean cosmetics, electronics, and craft spirits [4]CNBC, “How a Stronger Yen May Impact Tourism,” cnbc.com . Southeast Asia, led by Vietnam’s 17.5 million arrivals and Thailand’s wellness boom, adds diversified growth nodes. Australia leverages favourable FX rates to lure Asian shoppers toward wine and organic skincare, while South Korea continues to profit from K-beauty fervour and electronics export appeal. This geographic diversity buttresses the Asia-Pacific travel retail market against localized shocks and currency gyrations.

Competitive Landscape

The Asia-Pacific travel retail market exhibits moderate concentration, with the top five companies controlling more than half of the revenue, leaving space for agile disruptors. China Duty Free Group, Dufry, DFS Group, Lagardère Travel Retail, and The Shilla Duty Free wield procurement scale and multi-country footprints, negotiating favourable terms for anchor positions in flagship airports. Omnichannel capabilities deepen: AI personalization engines recommend bundles, while mobile wallets enable one-click settlement for pre-trip reservations. Secondary airports and high-speed rail stations offer cost-advantaged concessions, attracting niche operators that specialize in vegan beauty, craft beer, or regional souvenirs. Joint ventures between landlords and brand consortiums accelerate buildouts while sharing capital risk. Sustainability themes, plastic-free packaging, local sourcing, renewable energy lighting, score tender evaluation points, and improve shopper perception.

The Asia-Pacific travel retail market is undergoing a significant transformation as emerging competitors adopt advanced strategies to capture market share. These strategies include utilizing social-commerce influencers to drive engagement, integrating augmented-reality trial experiences to enhance customer interaction, and launching cryptocurrency-linked loyalty programs to appeal to tech-savvy Gen-Z and millennial consumers. Concurrently, established players are increasingly engaging in strategic acquisitions of technology startups to accelerate innovation cycles and strengthen their market position. Despite facing challenges such as rising rental costs and heightened regulatory compliance expenses, competition within the market remains intense. Companies are shifting their focus toward delivering superior customer experiences, leveraging sophisticated data analytics, and expanding their distribution channels. This strategic emphasis on value creation over price competition is fostering a dynamic and competitive landscape in the Asia-Pacific travel retail market.

Asia-Pacific Travel Retail Industry Leaders

-

China Duty Free Group (CTGDF)

-

Dufry AG

-

Lotte Duty Free

-

DFS Group (LVMH)

-

Shilla Duty Free

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: Lagardère Travel Retail secured an eight-year duty-free contract at Auckland Airport, marking a significant expansion of its store network in Oceania and strengthening its regional footprint.

- February 2025: China Duty Free Group (CDFG) entered Sri Lanka by opening its first duty-free operation in the country, a strategic expansion into South Asia that broadens the company’s geographic reach.

- January 2025: CDFG won downtown duty-free concessions in Chengdu and Tianjin under China’s new urban retail policy, deepening its presence in major mainland cities.

- August 2024: The Shilla Duty Free opened a flagship beauty-brand boutique zone in Incheon Airport Terminal 2, launching a new premium beauty concept tailored to international travellers.

Asia-Pacific Travel Retail Market Report Scope

Travel retail is sales made in travel environments. It covers duty-free environments of the world, including airports, airlines, cruises, downtown locations, and border shops. Asia-Pacific travel retail market is segmented into product type, distribution channel, and geography. The market is segmented by product type into fashion and accessories, jewelry and watches, wine & spirits, food & confectionery, fragrances and cosmetics, and tobacco. The market is divided by distribution channels into airports, airlines, and ferries. By geography, the market is divided into China, Japan, Korea, India, Australia, Southeast Asia, and the Rest of Asia-Pacific. The report offers market size and forecasts for the Asia Pacific retail market in value (USD) for all the above segments.

By Product Type

| Fashion and Accessories |

| Wine and Spirits |

| Tobacco |

| Food and Confectionary |

| Fragrances and Cosmetics |

| Other Product Types (Stationery, Electronics, Watches, Jewelry, etc.) |

By Distribution Channel

| Airports |

| Cruise Liners |

| Railway Stations |

| Other Distribution Channels |

By Traveler Demographics

| Business Travelers |

| Leisure Travelers |

| Visiting Friends and Relatives (VFR) |

| Medical and Wellness Tourists |

| Student Travelers |

By Geography

| India |

| China |

| Japan |

| Australia |

| South Korea |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) |

| Rest of Asia-Pacific |

| By Product Type | Fashion and Accessories |

| Wine and Spirits | |

| Tobacco | |

| Food and Confectionary | |

| Fragrances and Cosmetics | |

| Other Product Types (Stationery, Electronics, Watches, Jewelry, etc.) | |

| By Distribution Channel | Airports |

| Cruise Liners | |

| Railway Stations | |

| Other Distribution Channels | |

| By Traveler Demographics | Business Travelers |

| Leisure Travelers | |

| Visiting Friends and Relatives (VFR) | |

| Medical and Wellness Tourists | |

| Student Travelers | |

| By Geography | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large will Asia-Pacific travel retail spending be by 2030?

Forecasts place the market at USD 54.84 billion by 2030.

Which category leads duty-free sales across the Asia Pacific?

Fragrances and cosmetics held the top position with a 36.33% share in 2024.

What traveller cohort is expanding fastest?

Medical and wellness tourists are projected to grow at a 14.83% CAGR.

Why are railway stations viewed as the next big retail hubs?

High-speed rail buildouts in China and India unlock new passenger volumes and lower rent structures.

How concentrated is competitive power among retailers?

The top five groups control more than half of the revenue, indicating moderate concentration.

What is the main profitability headwind for operators?

Rising concession fees at flagship airports compress margins and shift focus to secondary gateways.

Page last updated on: