Robotics & Drone-based NDT Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

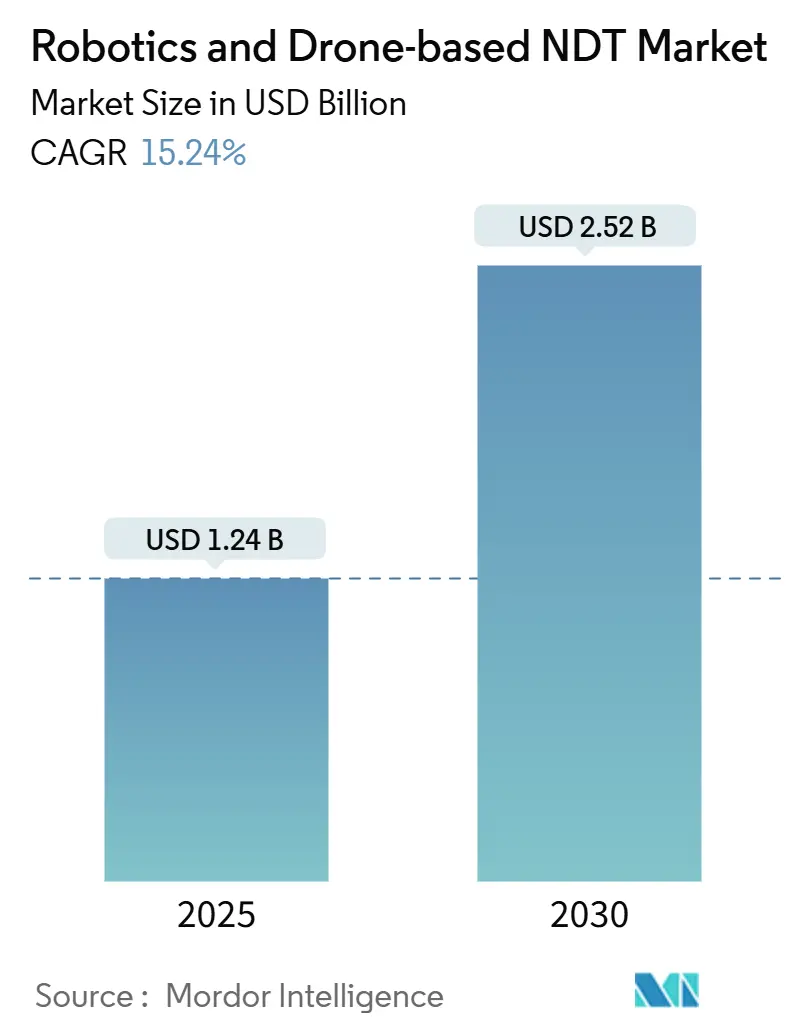

| Market Size (2025) | USD 1.24 Billion |

| Market Size (2030) | USD 2.52 Billion |

| Growth Rate (2025 - 2030) | 15.24% CAGR |

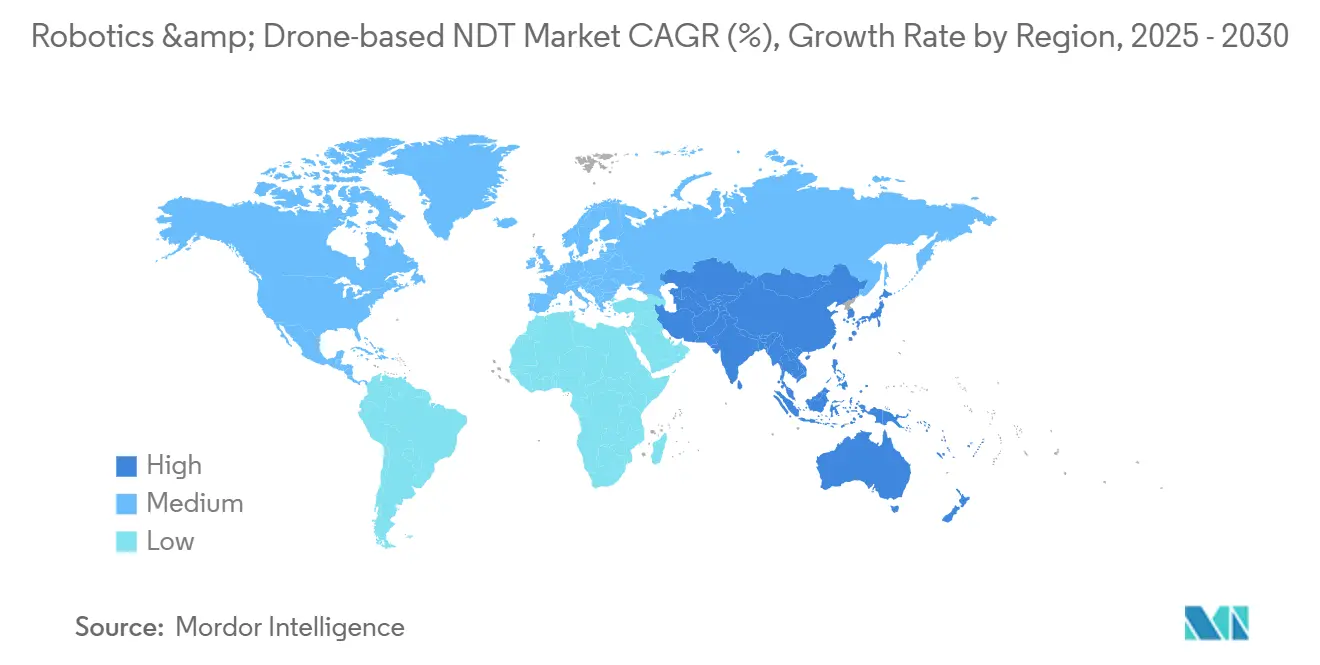

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Robotics & Drone-based NDT Market Analysis by Mordor Intelligence

The Robotics and drone-based NDT market size is projected to reach USD 2.52 billion by 2030, reflecting a 15.24% CAGR from USD 1.24 billion in 2025. The surge stems from urgent safety mandates for aging pipelines, cost-saving predictive maintenance programs, and artificial intelligence-enabled inspection algorithms that shorten decision-making cycles. Energy infrastructure operators are shifting their budgets toward automated systems that prevent technicians from being exposed to toxic, explosive, or high-radiation environments. Platforms that blend ultrasonic, thermographic, and visual sensors now transmit near-real-time data to cloud analytics suites, accelerating root-cause analysis. Competitive intensity is intensifying as niche robotics specialists, large inspection service providers, and software start-ups race to bundle hardware, analytics, and regulatory expertise into turnkey offerings for the Robotics and drone-based NDT market.

Key Report Takeaways

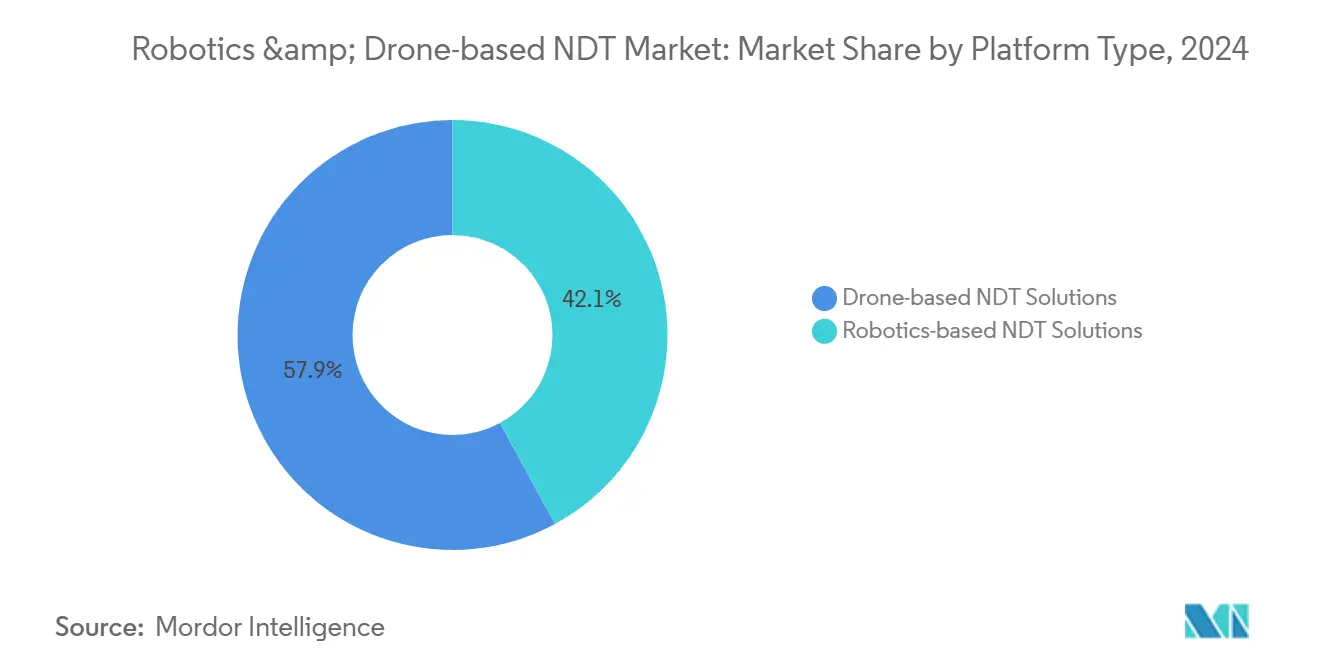

- By platform type, drone-based solutions held 57.9% of the Robotics and drone-based NDT market share in 2024, while robotics-based solutions are set to grow at an 18.4% CAGR through 2030.

- By testing method, ultrasonic testing is expected to lead with a 34.2% revenue share in 2024; thermography and infrared testing are forecast to expand at a 16.1% CAGR to 2030.

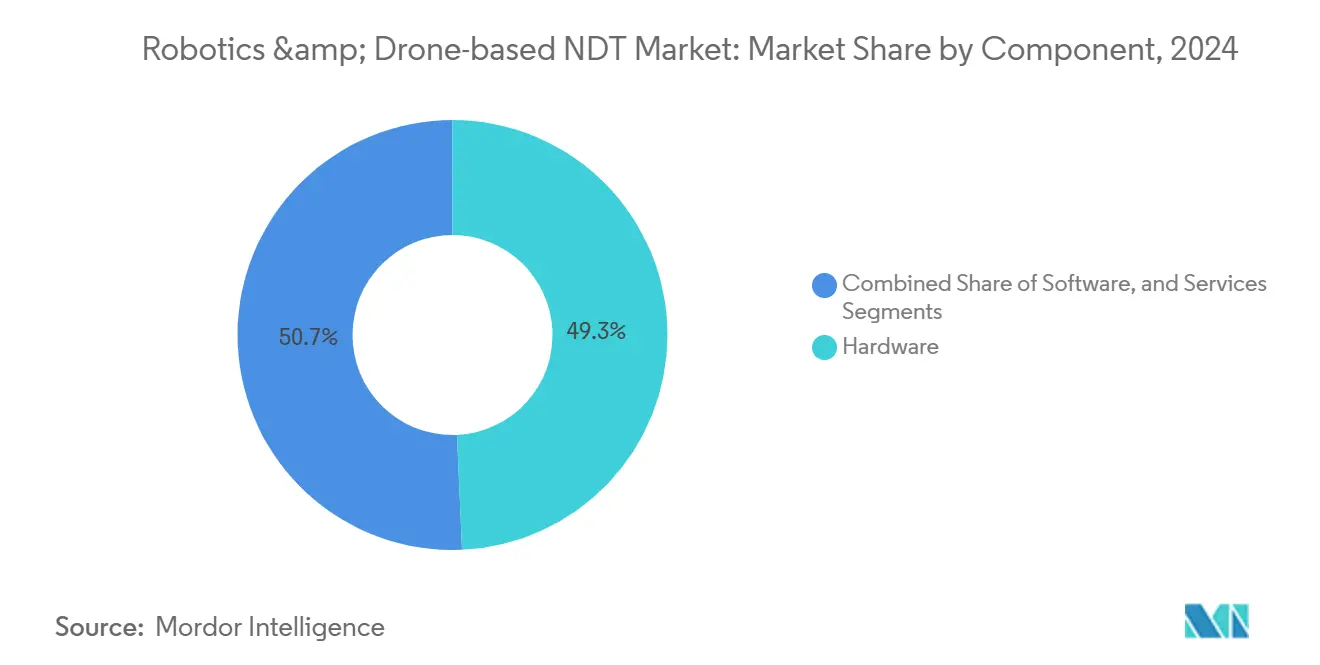

- By component, hardware commanded 49.3% of the Robotics and drone-based NDT market size in 2024, whereas software is projected to post a 19.2% CAGR through 2030.

- By end-user industry, the oil and gas sector captured a 27.4% share in 2024; however, the automotive and transportation sector is projected to record the fastest growth, with a 17.4% CAGR between 2025 and 2030.

- By geography, North America held a 38.3% share in 2024, while the Asia-Pacific region is expected to advance at a 16.5% CAGR through 2030.

Global Robotics & Drone-based NDT Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated uptake of automated inspection in hazardous environments | +3.2% | Global, with a concentration in North America and the Middle East | Medium term (2-4 years) |

| Rising aging infrastructure in oil and gas pipelines | +2.8% | North America and Europe, spillover to the Middle East | Long term (≥ 4 years) |

| Cost reduction from predictive maintenance-as-a-service models | +2.1% | Global, early adoption in APAC manufacturing hubs | Short term (≤ 2 years) |

| Drone regulations easing BVLOS operations | +1.9% | North America and Europe, a gradual expansion to APAC | Medium term (2-4 years) |

| Integration of Digital Twin platforms with NDT data | +1.7% | Global, led by advanced manufacturing regions | Long term (≥ 4 years) |

| ESG-driven demand for safer inspection practices | +1.4% | Global, strongest in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Uptake of Automated Inspection in Hazardous Environments

Industrial facilities now adopt robots and drones to remove personnel from confined spaces where toxic gases, high temperatures, and ionizing radiation persist. The Occupational Safety and Health Administration linked 1,030 confined-space fatalities between 2011 and 2018 to traditional entry methods, spurring stronger compliance enforcement.[1]Occupational Safety and Health Administration, “Confined Space Safety Standards,” osha.gov Petrochemical plants and nuclear operators deploy crawler robots capable of navigating six-inch gaps while carrying ultrasonic and radiographic probes. Onboard 4K cameras and environmental sensors push encrypted data to control rooms, allowing supervisors to intervene immediately if risk thresholds are breached. Operations teams report task-time reductions of 60% when automated inspection replaces rope-access crews. Real-time streaming also feeds digital-twin models that update corrosion rates, supporting evidence-based maintenance budgeting across the Robotics and drone-based NDT market.

Rising Aging Infrastructure in Oil and Gas Pipelines

More than 70% of North American pipelines exceed their original 30-year design life, a reality underscored by 1,377 incidents and USD 1.2 billion in property losses recorded in 2023.[2]Pipeline and Hazardous Materials Safety Administration, “Pipeline Incident Reports,” phmsa.dot.gov Drone-mounted thermographic cameras identify hot spots that indicate coating failure, while ultrasonic crawlers validate wall-thickness loss without interrupting the flow. European operators face comparable risks as Soviet-era lines approach critical thresholds. Automated inspection lowers life-cycle costs because replacement averages USD 3 million per mile, whereas inspection programs cost less than 5% of that amount. When combined with machine-learning trend analysis, operators can schedule recoating or sleeve repair exactly when remaining strength falls below regulatory margins, a practice gaining traction across the Robotics and drone-based NDT market.

Cost Reduction from Predictive Maintenance-as-a-Service Models

Manufacturers are pivoting from reactive fixes to subscription-based monitoring contracts that deploy autonomous platforms on preset intervals. McKinsey estimates these data-driven arrangements cut unplanned downtime by up to 50%. Integrated Internet of Things gateways stream sensor readings to enterprise asset systems, creating alerts that align part procurement, workforce assignment, and production scheduling. Analytics engines now pinpoint bearing degradation up to six months in advance, allowing purchasing teams to negotiate volume discounts. This pay-as-you-use model removes capital barriers for mid-sized factories that previously could not afford robots. The resulting democratization accelerates overall uptake, reinforcing sustainable growth in the Robotics and drone-based NDT market.

Drone Regulations Easing BVLOS Operations

A harmonized regulatory landscape is expanding flight envelopes beyond the visual line of sight. The Federal Aviation Administration has cleared more than 15,000 BVLOS missions since 2024, with energy asset inspection leading all categories.[3]Federal Aviation Administration, “Beyond Visual Line of Sight Operations,” faa.gov The European Union Aviation Safety Agency followed suit in 2024, enabling drones to cross borders without redundant offset approvals. Long-range quadcopters now patrol 200-mile oil trunk lines in a single sortie, a feat that once required helicopters and multi-day ground walks. Utilities disclose 80% cost savings and monthly inspection frequencies, compared with annual schedules prior to BVLOS clearance. As Asia-Pacific regulators roll out similar waivers, demand for long-endurance drones will rise, cementing BVLOS as a core growth lever in the Robotics and drone-based NDT market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited payload capacity affects sensor choice | -2.1% | Global, most acute in offshore and remote applications | Medium term (2-4 years) |

| High upfront cost of advanced robotics systems | -1.8% | Emerging markets and SMEs globally | Short term (≤ 2 years) |

| Data security and IP ownership concerns in cloud analytics | -1.3% | Global, the strongest impact in defense and aerospace | Long term (≥ 4 years) |

| Shortage of certified remote NDT operators | -1.1% | Global, most severe in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Payload Capacity Affecting Sensor Choice

Most commercial drones have a payload capacity of 10-15 pounds, forcing trade-offs between flight endurance and sensor richness. Radiographic cassettes and high-element ultrasonic arrays often breach weight limits, which means running multiple sorties or accepting narrower diagnostic coverage. The American Society for Nondestructive Testing documented instances in which operators missed anomalies because optimal sensor mixes were impossible within weight constraints. Offshore wind inspections underscore the challenge: turbines require long-range plus infrared, ultrasonic, and LiDAR data, yet battery drain accelerates with every additional pound. Advances in fuel-cell propulsion and lightweight composite housings are promising, but until they scale, payload ceilings will temper revenue realization in certain high-value niches of the Robotics and drone-based NDT market.

High Upfront Cost of Advanced Robotics Systems

Full-featured crawler or snake robots cost USD 500,000 to USD 2 million, excluding operator certification and annual maintenance contracts. The International Federation of Robotics confirmed that companies with fewer than 500 employees cite finance as the primary barrier to adoption.[4]International Federation of Robotics, “Industrial Robotics Adoption Report,” ifr.org Leasing and robotics-as-a-service agreements mitigate sticker shock, but multiyear commitments deter firms worried about rapid technology obsolescence. Emerging-market manufacturers also face exchange-rate volatility that inflates loan payments. These capital hurdles lengthen sales cycles, especially for deployments outside regulated sectors where return-on-investment metrics are not mandated by law. Until hardware costs decrease or financing options expand, adoption among small and mid-sized enterprises will be slower than headline forecasts for the robotics and drone-based NDT market suggest.

Segment Analysis

By Platform Type: Robotics Gains Precision while Drones Scale Coverage

The Robotics and drone-based NDT market generated 57.9% of its revenue from drone platforms in 2024, driven by the rapid deployment and wide-area reach of these platforms. Robotics systems are driving the fastest segment growth at an 18.4% CAGR to 2030, reflecting the demand for precision-controlled inspections in boilers, pressure vessels, and nuclear reactors, where millimeter-level positioning is crucial. General Electric’s turbine-blade crawlers locate micro-cracks that aerial surveys cannot resolve, confirming the premium placed on deterministic motion. Manufacturers have begun hybridizing fleets so that drones perform external sweeps while tethered robots tackle interior welds, maximizing inspection completeness. Software convergence means a single dashboard now orchestrates flight paths, crawler routes, and analytics, shrinking data silos. As artificial-intelligence vision pipelines mature, robotics feedback loops will self-correct for slippage or vibration, further improving the probability of flaw detection rates. Such advancements explain why capital budgets are shifting toward robotics in high-stakes industries, despite the current dominance of drones within the broader Robotics and drone-based NDT market.

Robotics platforms also deliver unlimited operation time when cabled for power, enabling continuous production-line quality control. In contrast, drones remain battery-bound, although new hydrogen fuel cells promise three-hour endurance for linear infrastructure patrol. Regulatory scrutiny favors near-ground robots in hazardous locations because they reduce airspace risk and simplify insurance underwriting. Average payback periods fall below 24 months when robots replace scaffold erection and confined-space permits. These economics underpin the anticipated share shift: industry stakeholders expect robotics to account for more than 45% of segment revenues by 2030, reinforcing the pluralistic trajectory of the Robotics and drone-based NDT market.

By Testing Method: Ultrasonic Reliability Meets Thermographic Speed

Ultrasonic probes accounted for 34.2% of 2024 sales, primarily driven by applications in oil and gas wall-thickness measurement and aerospace weld validation. The method’s root-mean-square accuracy and ability to quantify defect depth keep it indispensable for high-integrity components. Infrared thermography is growing at the fastest rate, with a 16.1% CAGR, as core resolution falls to 0.1 °C, revealing early electrical faults that are invisible to ultrasonics. Artificial-intelligence classification models now parse thermal images in real time, flagging hotspots that correspond to material fatigue or loose connections. This speed advantage appeals to automotive battery makers striving for zero-defect cell lines.

Radiographic X-ray remains critical in defense, where castings and composite laminates can hide voids that are unreachable by surface methods. Eddy-current arrays can penetrate coatings without surface preparation, making them popular for mapping aircraft fuselage corrosion. Visual testing benefits from HD optics and LED lighting that enhance low-light capture, while acoustic emission sensors detect crack propagation during pressurization trials. The multidisciplinary approach is codified in the latest International Organization for Standardization guidance, which recommends combining at least two modalities for mission-critical assets. Vendors who bundle multi-sensor payloads are therefore better positioned to win contracts within the evolving Robotics and drone-based NDT market.

By Component: Software Overtakes Hardware for Value Creation

Hardware still represented 49.3% of category income in 2024, but software revenues are expanding at a 19.2% CAGR, as value now lies in data interpretation rather than capture. Cloud analytics engines stitch multiple inspection runs into unified digital twins, allowing what-if failure simulations with 95% confidence. Algorithms identify anomalies and generate automatic work orders that feed maintenance planning modules. Risk-based inspection matrices embedded in the software rank defects by consequence and probability, aiding compliance with ISO 55000 asset-management standards.

Service lines, including operator training and fleet maintenance, account for growing annuity streams that cushion hardware margin compression. Some robotics OEMs now lead with software-as-a-service proposals, bundling devices at breakeven to secure multiyear analytics fees. Real-time dashboards slice throughput by asset type, geography, and time stamp, revealing O-ring fatigue trends that corporate engineers can benchmark across facilities. As 5G rollouts slash latency, edge processing on drones will pre-filter datasets, transmitting only exceptions to the cloud. This distributed architecture eases bandwidth costs and strengthens cyber posture, accelerating enterprise integration across the Robotics and drone-based NDT market.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Oil and Gas Dominates Today, Automotive Accelerates Tomorrow

Oil and gas operators contributed 27.4% of turnover in 2024, primarily due to the extensive mileage of their pipelines and penalties associated with spills. Integrity management programs increasingly specify autonomous crawlers for internal weld scans every six months, up from annual schedules five years ago. Simultaneously, major refiners adopt drone-based gas-leak detection to comply with methane-emission rules. These commitments keep oil and gas entrenched as the largest spender, yet CAGR prospects are moderating as installed fleets mature.

Automotive plants will add the most incremental dollars through 2030 thanks to electric-vehicle battery pack inspections and lidar sensor calibration. Battery lines require non-destructive cell balancing checks that can be completed in under 30 seconds per module using robotic ultrasonics. Autonomous vehicle programs impose stringent sensor-cover integrity tests that infrared drones accomplish without disassembling prototype cars. The aerospace and defense segments maintain premium pricing for computed tomography scans of critical castings, while power generation utilities deploy radiation-tolerant robots in high-flux reactor vessels. Chemical and petrochemical producers remain early adopters of explosion-proof robots. In aggregate, industry diversity cushions cyclical exposure, strengthening the long-term outlook for the Robotics and drone-based NDT market.

Geography Analysis

North America accounted for 38.3% of the revenue in 2024, driven by mature regulations and extensive legacy infrastructure. Pipeline and Hazardous Materials Safety Administration integrity mandates require recurrent smart-piggable diagnostics; however, unreachable elbows and tees prompt operators to consider external crawler robots. Utilities also leverage the Federal Aviation Administration’s BVLOS waivers to inspect high-voltage corridors every month, cutting helicopter flights by 75%. Regional vendors offer turnkey compliance packages that integrate data archives, simplifying audits and reinforcing North American supremacy within the Robotics and drone-based NDT market.

The Asia-Pacific region is advancing at the fastest rate, with a 16.5% CAGR through 2030, driven by the rollout of Belt and Road infrastructure and the upscaling of manufacturing. China mandates ultrasound structural health checks for all new petrochemical tanks, driving volume orders for domestic drone makers. India’s target of 500 GW of renewable capacity by 2030 drives demand for wind-tower and solar-farm inspections. Southeast Asian refineries are adopting pay-per-scan contracts to meet the certification requirements of their export customers. Government innovation funds subsidize local robotics start-ups, sustaining price competition that accelerates the adoption of these technologies.

Europe sits between the two extremes, but its Green Deal policies funnel capital into offshore wind and hydrogen pipelines that require cutting-edge inspection solutions. Germany’s automotive titans deploy in-line thermography to ensure paint-shop quality, while France’s nuclear reactors deploy radiation-hardened crawlers for vessel internals. Cross-border harmonization by the European Union Aviation Safety Agency eliminates legal friction, enabling service firms to operate fleets across the continent. This regulatory clarity supports steady, albeit moderate, expansion of the robotics and drone-based NDT market across Europe.

Competitive Landscape

The Robotics and drone-based NDT market is moderately fragmented, with no firm holding a significant share of revenue. Gecko Robotics, Flyability, Skydio, Eddyfi Technologies, and Terra Drone top the leaderboard, but each specializes in different modalities, preventing direct one-for-one substitution. Patent filings have exceeded 2,400 since 2020, indicating active R&D pipelines focused on lighter sensors, autonomous navigation, and AI analytics.

Strategic mergers concentrate capabilities: Eddyfi’s acquisition of Advanced NDT Solutions unifies its electromagnetic, ultrasonic, and crawler portfolios; Skydio’s X10 launch addresses offshore payload concerns; Terra Drone and Mitsubishi Heavy Industries co-develop turbine inspection drones that leverage Mitsubishi’s blade expertise. Such vertical integration fortifies entry barriers and compels smaller firms to ally for market access.

Partnerships between platform builders and cloud-software vendors are common because hardware differentiation alone is unsustainable. Service providers bundle training and data analytics as annuities to offset declining sensor margins. Buyers are increasingly favoring suppliers that guarantee end-to-end compliance, pushing the ecosystem toward multidisciplinary conglomerates. These dynamics foster competition while leaving room for innovation, thereby sustaining healthy margins within the Robotics and drone-based NDT market.

Robotics & Drone-based NDT Industry Leaders

-

Eddyfi Technologies Inc.

-

Flyability SA

-

Cyberhawk Innovations Ltd.

-

Skydio Inc.

-

Gecko Robotics Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Flyability SA secured USD 25 million Series C funding to scale radiation-hardened inspection robots for nuclear sites in Europe and North America.

- August 2025: Gecko Robotics Inc. formed a five-year alliance with Shell plc to deploy climbing robots across 15 refineries and integrate data with Shell’s digital-twin dashboards.

- July 2025: Skydio Inc. released the X10 industrial drone, featuring 45-minute endurance and a 20-pound payload bay tailored for NDT sensors.

- June 2025: Eddyfi Technologies Inc. bought Advanced NDT Solutions for USD 180 million, adding pipeline-crawler expertise to its portfolio.

Global Robotics & Drone-based NDT Market Report Scope

| Robotics-based NDT Solutions |

| Drone-based NDT Solutions |

| Ultrasonic Testing |

| Radiographic Testing |

| Magnetic Particle Testing |

| Liquid Penetrant Testing |

| Visual Inspection Testing |

| Eddy-Current Testing |

| Acoustic Emission Testing |

| Thermography / Infrared Testing |

| Computed Tomography Testing |

| Hardware |

| Software |

| Services |

| Oil and Gas |

| Power Generation |

| Aerospace |

| Defense |

| Automotive and Transportation |

| Manufacturing and Heavy Engineering |

| Construction and Infrastructure |

| Chemical and Petrochemical |

| Marine and Ship Building |

| Electronics and semiconductor |

| Mining |

| Medical Devices |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Platform Type | Robotics-based NDT Solutions | ||

| Drone-based NDT Solutions | |||

| By Testing Method | Ultrasonic Testing | ||

| Radiographic Testing | |||

| Magnetic Particle Testing | |||

| Liquid Penetrant Testing | |||

| Visual Inspection Testing | |||

| Eddy-Current Testing | |||

| Acoustic Emission Testing | |||

| Thermography / Infrared Testing | |||

| Computed Tomography Testing | |||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By End-user Industry | Oil and Gas | ||

| Power Generation | |||

| Aerospace | |||

| Defense | |||

| Automotive and Transportation | |||

| Manufacturing and Heavy Engineering | |||

| Construction and Infrastructure | |||

| Chemical and Petrochemical | |||

| Marine and Ship Building | |||

| Electronics and semiconductor | |||

| Mining | |||

| Medical Devices | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the Robotics and drone-based NDT market?

The Robotics and drone-based NDT market size is USD 1.24 billion in 2025.

What is the market's expected growth rate through 2030?

The market is projected to expand at a 15.24% CAGR, reaching USD 2.52 billion by 2030.

Which platform type is growing quickest?

Robotics-based solutions are forecast to grow at an 18.4% CAGR, the fastest among platform types.

Which testing method shows the highest growth rate?

Thermography and infrared testing are expected to advance at a 16.1% CAGR through 2030.

Which region will record the strongest growth?

The Asia-Pacific region is set to grow at a 16.5% CAGR, leading to regional expansion.

How are companies addressing payload limitations on drones?

Manufacturers are developing lighter sensors, hydrogen fuel cells, and higher-capacity airframes such as the Skydio X10 to increase payload without sacrificing range.

Page last updated on: