Rechargeable Battery Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

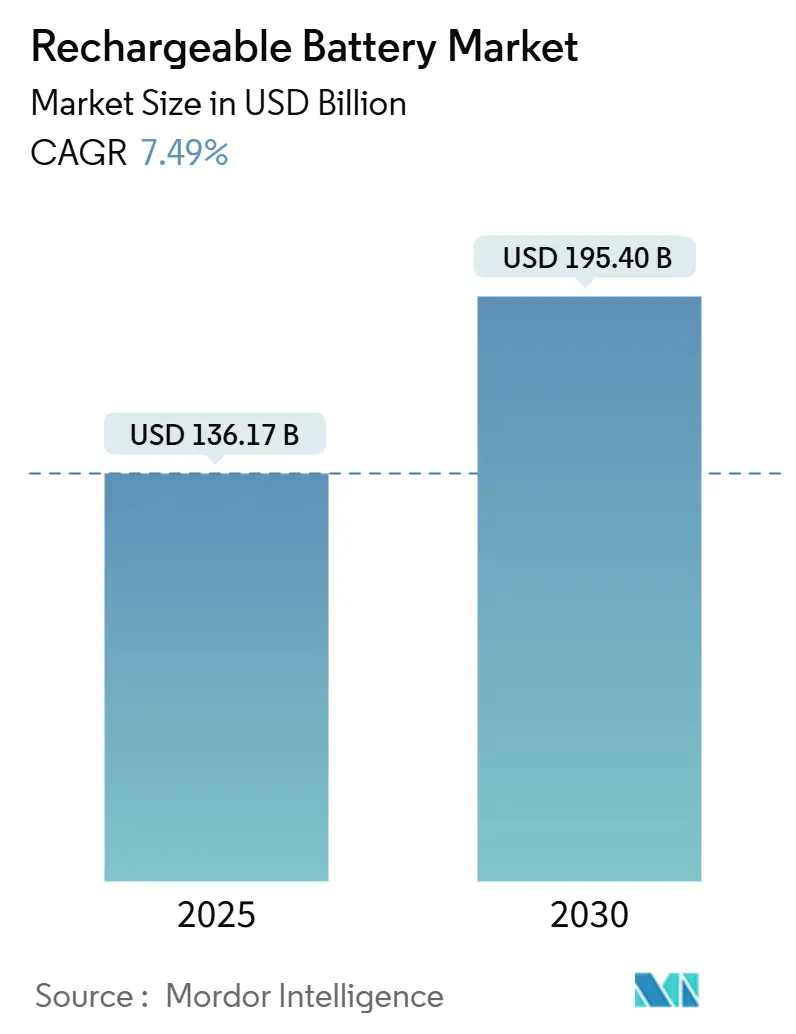

| Market Size (2025) | USD 136.17 Billion |

| Market Size (2030) | USD 195.40 Billion |

| Growth Rate (2025 - 2030) | 7.49% CAGR |

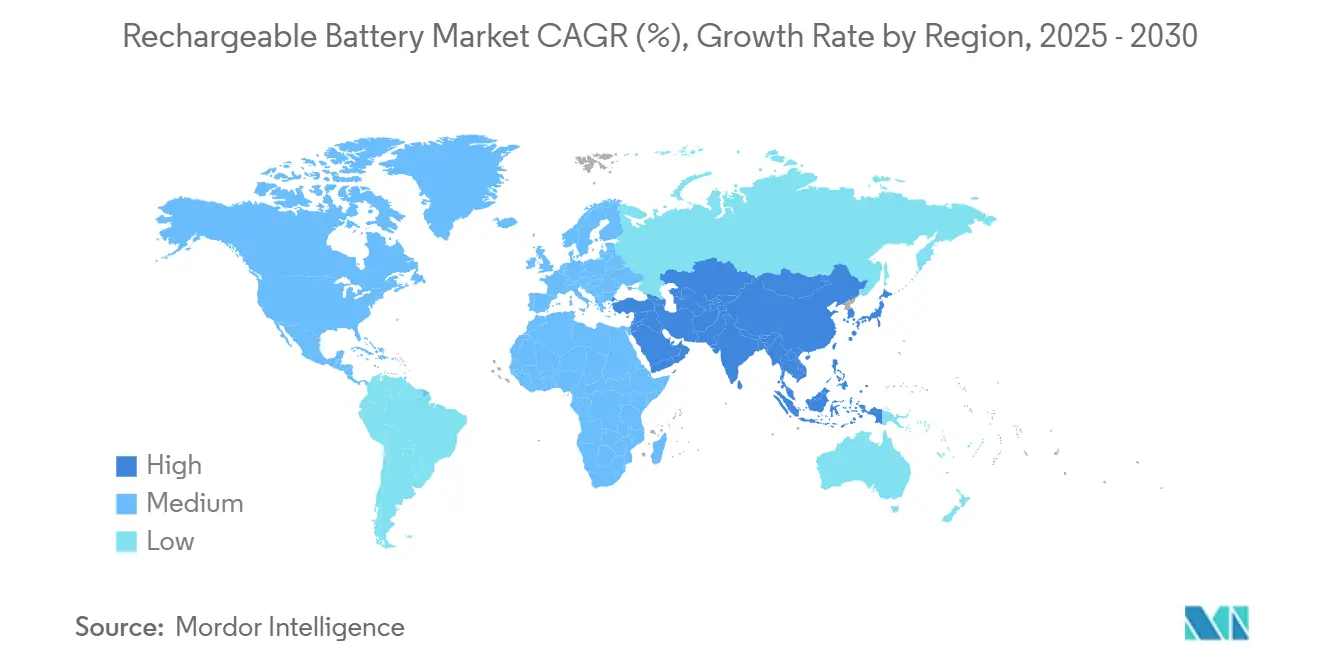

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Rechargeable Battery Market Analysis by Mordor Intelligence

The Rechargeable Battery Market size is estimated at USD 136.17 billion in 2025, and is expected to reach USD 195.40 billion by 2030, at a CAGR of 7.49% during the forecast period (2025-2030).

This expansion reflects enduring demand across electric mobility, stationary storage, and connected device ecosystems as governments, utilities, and corporations accelerate their decarbonization programs. The rechargeable batteries market benefits from converging trends, including record-high electric-vehicle (EV) sales, grid-scale renewable energy mandates, consumer electronics refresh cycles that now encompass wearable and IoT form factors, and policy incentives favoring domestic supply chains. Competitive pressures intensify as leading Chinese manufacturers defend cost advantages while Korean, Japanese, European, and North American peers race to localize production, secure critical minerals, and commercialize solid-state or sodium-ion alternatives. In parallel, price volatility for lithium, cobalt, and nickel introduces investment risk, even as lower raw-material costs temporarily improve battery affordability.

Key Report Takeaways

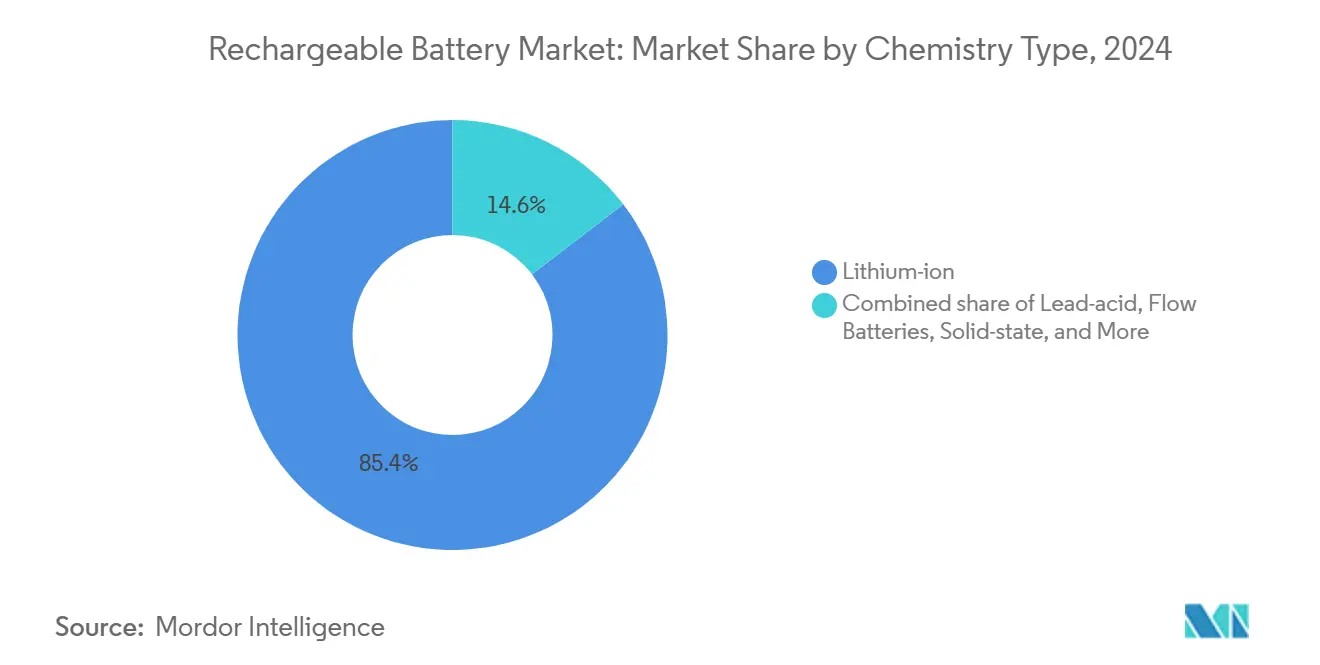

- By chemistry type, lithium-ion technology held 85.4% of the rechargeable battery market share in 2024, while flow batteries were projected to have the highest CAGR of 20.9% from 2024 to 2030.

- By form factor, cylindrical cells captured 50.1% revenue share in 2024; thin-film and micro batteries are expected to expand at a 21.5% CAGR through 2030.

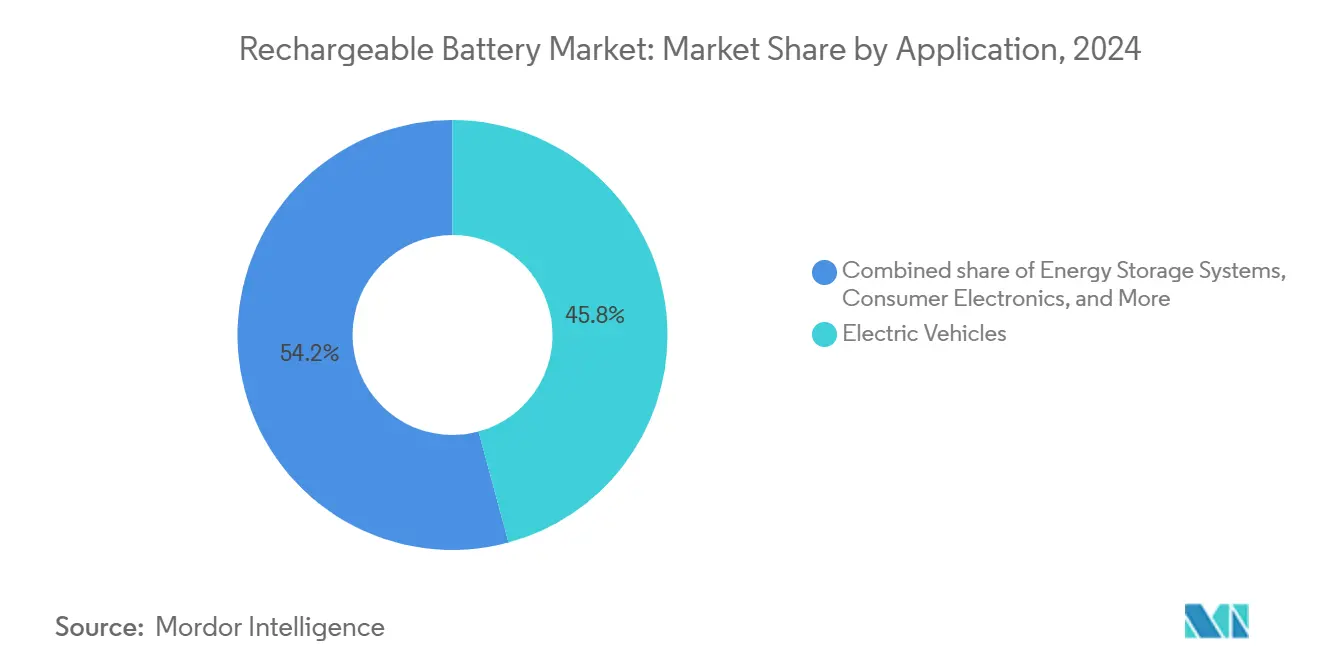

- By application, electric vehicles accounted for 45.8% of the 2024 demand, whereas energy storage systems are forecast to grow at a 19.7% CAGR through 2030.

- By end-user, automotive OEMs represented 50.0% of 2024 shipments, while utilities and IPPs recorded the strongest growth outlook at a 20.1% CAGR to 2030.

- By geography, the Asia-Pacific region accounted for 53.7% of 2024 revenues and is projected to grow at an 8.1% CAGR over the forecast period.

Global Rechargeable Battery Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exponential EV demand & giga-factory expansions | +2.10% | Global, APAC and North America lead | Medium term (2-4 years) |

| Surging consumer electronics & IoT volumes | +1.30% | Global, concentrated in APAC hubs | Short term (≤ 2 years) |

| Grid-scale renewable-storage mandates | +1.80% | North America, Europe, selective APAC markets | Long term (≥ 4 years) |

| Corporate net-zero PPAs driving stationary storage | +0.90% | North America, Europe | Medium term (2-4 years) |

| Defense electrification for silent powerpacks | +0.40% | North America, Europe, developed APAC | Long term (≥ 4 years) |

| Data-center UPS migration to Li-ion | +0.60% | Global data-center clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Exponential EV Demand & Giga-factory Expansions

Electric-vehicle production drives the single largest increase in battery consumption, with capacity requirements forecasted to exceed 5,800 GWh by 2035 as OEMs scale up their production targets. Market leaders are investing heavily: CATL has injected RMB 2.5 billion into NIO Power to integrate battery-swap networks, while LG Energy Solution's Arizona complex will supply 53 GWh annually and meet the requirements of the Inflation Reduction Act. Fast-charge breakthroughs and 6C-rated cells necessitate 650 kW chargers, increasing secondary demand for stationary storage that buffers grid peaks. Korean producers pledged KRW 52 trillion toward capacity through 2025, yet face shrinking margins due to Chinese vertical integration and state support. These investments sustain a virtuous cycle, where production-scale economics lower unit prices, unlocking further volume and reinforcing the growth of the rechargeable batteries market.

Surging Consumer Electronics & IoT Volumes

Smartphone, wearable, and medical device manufacturers are pivoting toward modular designs as EU rules mandate user-replaceable batteries by 2027, favoring cell formats that balance repairability and energy density. The combined wearable and implantable medical segment reached USD 49 billion in 2024, prompting demand for chemistries that tolerate microwatt-range draw with decade-long lifespans. IoT proliferation spurs thin-film and micro-battery innovations, with energy harvesting and solid-state electrolytes improving safety and density. Data-center operators swap lead-acid UPS banks for lithium-ion units; Natron Energy’s North Carolina sodium-ion plant illustrates diversification toward lower-risk chemistries for mission-critical applications. Collectively, these trends diversify revenue beyond automotive and widen the addressable rechargeable batteries market.

Grid-scale Renewable Storage Mandates

Utility-scale storage mitigates renewables' intermittency. Australia's 850 MW Waratah Super Battery exemplifies coal-replacement projects that hinge on four-hour minimum storage durations. Germany commissioned a 500 MWh iron-flow battery, demonstrating the commercial ascent of long-duration, non-lithium technologies. California now stipulates a minimum of 1,000 MWh for projects, pushing developers toward integrated battery-plus-solar architectures that capture investment tax credits. These mandates accelerate adoption in the rechargeable batteries market by guaranteeing offtake for advanced chemistries.

Corporate Net-zero PPAs Driving Stationary Storage

Corporate renewable-power purchase agreements have exceeded historical highs as hyperscale data center electricity demand is projected to reach 2,000 TWh by 2030. The U.S. Department of Energy underwrote a battery installation at Iron Mountain’s Virginia campus, signaling federal alignment with corporate sustainability.(1)U.S. Department of Energy, “Clean Energy Demonstration Program for Universities,” energy.govVirtual-power-plant models allow enterprises to monetize distributed batteries via grid-services markets, while sub-USD 200/kWh system costs make behind-the-meter storage financially attractive. Clarios allocated USD 1 billion from a broader USD 6 billion domestic strategy to next-generation technologies aimed at these C&I buyers. Stationary-storage momentum therefore strengthens the long-term revenue mix of the rechargeable batteries market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Critical-mineral supply risk & price volatility | -1.40% | Global, with heightened exposure outside China | Short term (≤ 2 years) |

| Safety & fire-incident driven transport rules | -0.80% | Global, with stricter enforcement in developed markets | Medium term (2-4 years) |

| Margin compression due to battery oversupply | -0.60% | China, South Korea, extending into export-oriented manufacturing hubs | Short term (≤ 2 years) |

| Localization mandates driving higher capex & compliance | -0.50% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Critical-Mineral Supply Risk & Price Volatility

The International Energy Agency warns that existing mines will satisfy only 70% of projected copper and 50% of lithium demand by 2035, requiring USD 800 billion in new investment to balance supply. Macroeconomic slowdown, reduced EV demand, and Chinese market manipulation have depressed prices, deterring capital allocation as reflected by a 30% fall in S&P Global’s project-pipeline index.(2)Center for Strategic & International Studies, “Metals Markets Monitor March 2025,” csis.orgClosure of Panama’s Cobre mine stripped 350,000 t of annual copper, underscoring environmental and social license vulnerabilities.(3)Financial Post, “Panama Copper Mine Closure Implications,” financialpost.com Argentina’s lithium boom similarly encounters Indigenous opposition and water-scarcity debates that stall approvals. These disruptions threaten input availability and raise the cost of scaling the rechargeable batteries market.

Safety & Fire-incident Driven Transport Rules

Safety regulators intensify oversight after high-profile thermal runaway events. The U.S. Department of Transportation updated FMVSS 305a to standardize EV post-crash protocols and mandated watt-hour labeling for all shipped cells. Logistics providers now face higher insurance premiums and compliance documentation burdens. Simultaneously, the EU’s Battery Regulation imposes comprehensive due diligence and recycled-content thresholds by 2030, thereby increasing the administrative costs for smaller manufacturers. These rules inject friction that tempers near-term growth in the rechargeable batteries market.

Segment Analysis

By Chemistry Type: Lithium-ion Dominance Faces Flow-battery Disruption

Lithium-ion technology retained an 85.4% market share of the 2024 rechargeable batteries market, driven by its high energy density and proven cost curve. Flow batteries, however, show a 20.9% CAGR through 2030 as utilities favor 10-to-12-hour discharge durations that reduce daily cycling stress. The rechargeable batteries market size for flow batteries is projected to rise from a low single-digit USD billion base in 2024 toward mid-teen billions by 2030, capturing niches where cycle life and safety trump volumetric density. Lithium-ion producers are responding with higher-nickel cathodes and silicon-rich anodes to maintain their performance leadership, while solid-state roadmaps promise 900 Wh/L cells by 2027, pending the achievement of scale economics. Iron-flow and vanadium-flow technologies advance in parallel, leveraging recyclable electrolytes that decouple energy and power components. Collectively, chemistry diversification hedges supply chain risks and opens up specialized opportunities within the rechargeable batteries market.

Lithium-ion leaders are funneling R&D toward localized raw-material substitution, adding manganese-rich cathodes to reduce dependency on nickel and cobalt, and licensing safety-layer patents to suppress thermal events. Flow-battery integrators forge EPC alliances to supply containerized systems at solar and wind sites. Lead-acid and nickel-cadmium retain their roles in starter lighting ignition and extreme-temperature aerospace applications, underscoring that proven chemistries coexist alongside emerging ones.

Note: Segment shares of all individual segments available upon report purchase

By Form Factor: Cylindrical Cells Lead Despite Thin-film Innovation

Cylindrical cells accounted for 50.1% of 2024 sales as Tesla-style 4680 formats anchor large automotive programs. The rechargeable batteries market size attributable to cylindrical formats is expected to climb at mid-single-digit CAGR, bolstered by manufacturing yield improvements and mature supply chains. Pouch designs continue to serve premium EVs and flagship smartphones where gravimetric density and flat-pack integration outweigh mechanical rigidity. Prismatic formats dominate Chinese entry-level EVs and energy-storage cabinets, favoured for simplified module assembly. Emerging thin-film and micro batteries, although representing a modest revenue base, are projected to register a 21.5% CAGR as wearables, patches, and implantables proliferate. EU repairability rules catalyze demand for standardized modules, reshaping handset architectures and compelling suppliers to balance serviceability with longevity. Manufacturing scale inhibits rapid displacement of entrenched cylindrical and prismatic lines; however, innovations in laser-welded tablet designs and solvent-free electrode coatings lower cost per watt-hour, sustaining leadership within the rechargeable batteries market.

By Application: EVs Dominate While Energy Storage Accelerates

Electric vehicles accounted for 45.8% of 2024 shipments, equivalent to more than 1 TWh of cell output. Utilities now commission multi-hundred-MWh sites that require extended duration, pushing energy-storage systems to a 19.7% CAGR and elevating the segment’s rechargeable batteries market share. Consumer electronics continue to provide a resilient baseline volume, even as smartphone refresh cycles lengthen, thanks to growth in tablets, AR/VR headsets, and smart home devices. Industrial motive segments—such as forklifts, mining trucks, and construction machinery—switch from lead-acid to lithium-iron-phosphate batteries for maintenance and emissions advantages. Medical, aerospace, and defense end-markets, though smaller, deliver outsized profit margins on specialty chemistries. The interplay between vehicle-to-grid and second-life battery utilization blurs traditional application boundaries, supporting circular economy goals in the rechargeable batteries market.

Note: Segment shares of all individual segments available upon report purchase

By End-user: Automotive OEMs Lead, Utilities Surge

Automotive manufacturers consumed half of 2024 output as global EV production surpassed 14 million units. The utilities and IPP segment registers the fastest uptake at a 20.1% CAGR, propelled by reliability obligations and renewable portfolio standards that require four-hour or longer backup. Electronics OEMs contend with tighter margins but still constitute a significant slice of the rechargeable batteries market, while industrial OEMs benefit from fleet electrification mandates at ports, warehouses, and airports. Residential prosumers adopt rooftop solar-plus-battery packages to avoid demand charges and blackout risks, while commercial building owners retrofit their buildings to capture demand response revenue. Defense agencies seek sovereign supply lines and chemistries free of strategic-metal chokepoints, injecting R&D funds toward sodium-ion and solid-state platforms.

Geography Analysis

The Asia-Pacific region enjoys the largest rechargeable batteries market size, exceeding USD 70 billion by 2025, and is projected to maintain an 8.1% CAGR through 2030 as Chinese and Indian capacity additions reach full utilization. Government subsidies, low-cost labor, and vertically integrated supply chains provide regional manufacturers with cost advantages, even as trade friction increases. In contrast, North America's rechargeable battery market gains momentum from localization mandates tied to federal tax credits; gigafactory announcements exceed 400 GWh, yet raw material refining still relies on imports. Europe's regulatory push for 50% recycled content by 2030 aligns with circular economy priorities but raises capital expenditure hurdles for newcomers and underscores the strategic gap left by Northvolt's restructuring. Emerging regions aim to monetize their lithium and cobalt reserves by moving up the value chain; however, investment security, energy pricing, and skilled labor shortages remain impediments that temper the geographic rebalancing of the rechargeable batteries market.

North America captures an expanding share of announced cathode-and anode-active-material lines, aided by Department of Energy grants and state incentives that stipulate prevailing-wage labor. Canada's Oneida project demonstrates utilities' willingness to stipulate North American cell content, while Mexico positions itself for module assembly alongside U.S. auto plants. Meanwhile, Europe negotiates the return of battery IP as Asian firms establish local subsidiaries to meet local-content thresholds, creating a balancing act between domestic autonomy and foreign investment. The resultant policy landscape introduces regional supply clusters that favor shorter logistics chains and diversified raw material sourcing, which uplifts the rechargeable batteries market and mitigates geopolitical sAsia-Pacific'scific’s dominance remains anchored in robust domestic EV adoption, expansive export pipelines, and an upstream mineral nexus that combines Australian lithium, Indonesian nickel, and Chinese copper refIndia'sIndia’s import-duty concessions for manufacturers investing USD 500 million create new opportunities for global OEMs to participate incountry'stry’s energy transition agenda. Japan continues to leverage its precision-manufacturing expertise for specialty cell formats, while South Korea focuses its R&D on high-silicon anodes and polymer-based solid-state electrolytes to reclaim its margin leadership. Elsewhere, the Middle East leverages petrostate investment funds to seed long-duration storage pilots at renewable megaparks, and South America advances bilateral agreements to develop brine-to-battery partnering.

Competitive Landscape

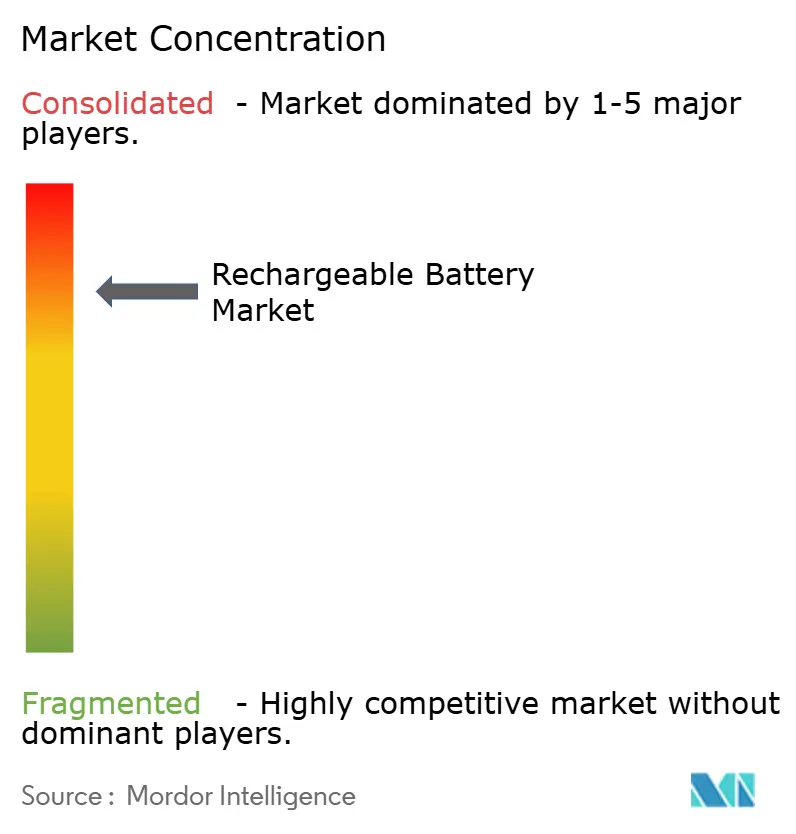

The rechargeable batteries market features a moderate concentration, with CATL leading with a 37.5% share, while the top five suppliers collectively hold roughly 70%, indicating a Score 7 market. Chinese incumbents leverage economies of scale, government subsidies, and secure upstream resources to maintain cost leadership. Korean firms LG Energy Solution, Samsung SDI, and SK On are investing aggressively in North America to regain price competitiveness and hedge against geopolitical exposure. Japanese suppliers emphasize niche chemistries and long-term alliances with automakers and aerospace primes, whereas U.S. and European entrants pursue breakthroughs in solid-state and sodium-ion technologies to leapfrog incumbents.

Strategic moves increasingly center on geographic diversification and vertical integration. CATL’s EUR 13.2 billion European expansion delivers localized capacity for Stellantis, BMW, and Volkswagen. LG Energy Solution’s multi-year cathode-material pact with General Motors underpins a 500,000-tonne CAM supply, reinforcing long-term cell sourcing. Panasonic scales 4680 cylindrical lines in Kansas to protect its anchor-customer franchise. Patent litigation intensifies as Korean and Japanese firms defend IP, evidenced by German injunctions against Sunwoda for cell-stack designs.

Technology roadmaps aim to differentiate themselves on fast charging, cycle life, and resource availability. Samsung SDI targets commercialization of solid-state batteries in 2027 at 900 Wh/L, while Toyota and Idemitsu pioneer the production of lithium-sulfide cathodes for a 2028 mass rollout. CATL and HiNa showcase sodium-ion cells with a capacity of 160 Wh/kg, targeting cost-sensitive markets. Flow-battery specialists ESS Inc. and Invinity secure utility pilot projects that validate iron and vanadium chemistries. Collectively, these initiatives signal an innovation race that could reorder leadership positions within the rechargeable batteries market over the long term.

Rechargeable Battery Industry Leaders

-

Contemporary Amperex Technology Co Ltd

-

LG Energy Solution Ltd

-

BYD Company Ltd.

-

Panasonic Holdings Corp.

-

Samsung SDI Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: NIO and CATL formed a strategic partnership on battery swapping technology, with CATL investing RMB 2.5 billion in NIO Power to establish unified industry technical standards for passenger vehicle battery swapping networks across China.

- March 2025: Clarios announced a USD 6 billion American energy manufacturing strategy, allocating USD 2.5 billion for advanced battery production, USD 1.9 billion for critical minerals processing and recovery, USD 1 billion for next-generation technologies, and USD 600 million for state-of-the-art manufacturing facilities to enhance domestic capacity and reduce reliance on imports.

- February 2025: Stellantis and CATL have committed up to EUR 4.1 billion to build a large-scale lithium-iron-phosphate battery plant in Zaragoza, Spain, with production expected to begin by late 2026.

- January 2025: EnerSys completed negotiation of a USD 199 million U.S. Department of Energy award to construct a lithium-ion battery manufacturing facility in Greenville, SC, supporting commercial, industrial, and defense applications.

- January 2025: Volvo Cars acquired Northvolt's stake in their joint battery venture, Novo, as Northvolt explores opportunities for expansion in North America while managing financial restructuring under Chapter 11 bankruptcy protection.

Global Rechargeable Battery Market Report Scope

| Lithium-ion |

| Lead-acid |

| Nickel-based |

| Solid-state |

| Flow Batteries |

| Other Rechargeables (Na-ion, Li-S, Li-metal) |

| Cylindrical Cell |

| Prismatic Cell |

| Pouch Cell |

| Coin and Button Cell |

| Thin-film and Micro Battery |

| Electric Vehicles |

| Consumer Electronics |

| Energy Storage Systems |

| Industrial Motive and Power Tools |

| Medical Devices |

| Aerospace and Defense |

| Marine and Rail |

| Automotive OEMs |

| Utilities and IPPs |

| Electronics OEMs |

| Industrial OEMs |

| Residential Prosumers |

| Commercial Building Operators |

| Defense Agencies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Chemistry Type | Lithium-ion | |

| Lead-acid | ||

| Nickel-based | ||

| Solid-state | ||

| Flow Batteries | ||

| Other Rechargeables (Na-ion, Li-S, Li-metal) | ||

| By Form Factor | Cylindrical Cell | |

| Prismatic Cell | ||

| Pouch Cell | ||

| Coin and Button Cell | ||

| Thin-film and Micro Battery | ||

| By Application | Electric Vehicles | |

| Consumer Electronics | ||

| Energy Storage Systems | ||

| Industrial Motive and Power Tools | ||

| Medical Devices | ||

| Aerospace and Defense | ||

| Marine and Rail | ||

| By End-user | Automotive OEMs | |

| Utilities and IPPs | ||

| Electronics OEMs | ||

| Industrial OEMs | ||

| Residential Prosumers | ||

| Commercial Building Operators | ||

| Defense Agencies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the rechargeable batteries market in 2030?

The market is forecast to reach USD 195.40 billion by 2030, growing at a 7.49% CAGR from 2025.

Which chemistry is gaining the fastest traction for long-duration storage?

Flow batteries are expected to expand at a 20.9% CAGR through 2030 as utilities pursue multi-hour discharge solutions.

How will regional policies shape supply chains?

Incentive packages in the U.S. and India are prompting manufacturers to localize gigafactories, diversifying supply away from single-region dependence.

Why are cylindrical cells still dominant in EVs?

Established manufacturing lines, proven thermal management, and new 4680 formats keep cylindrical cells at the forefront despite prismatic and pouch alternatives.

What critical challenge could slow market growth?

Supply-side risks for lithium and copper threaten timely capacity expansion, with current projects meeting just 50-70% of projected demand by 2035.

How are companies addressing safety and transport regulations?

Firms invest in advanced battery-management systems, standardized labeling, and solid-state or sodium-ion chemistries to reduce fire risk and comply with stricter rules.

Page last updated on: