Phosphine Fumigation Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 1.9 Billion |

| Market Size (2030) | USD 2.41 Billion |

| Growth Rate (2025 - 2030) | 4.90% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

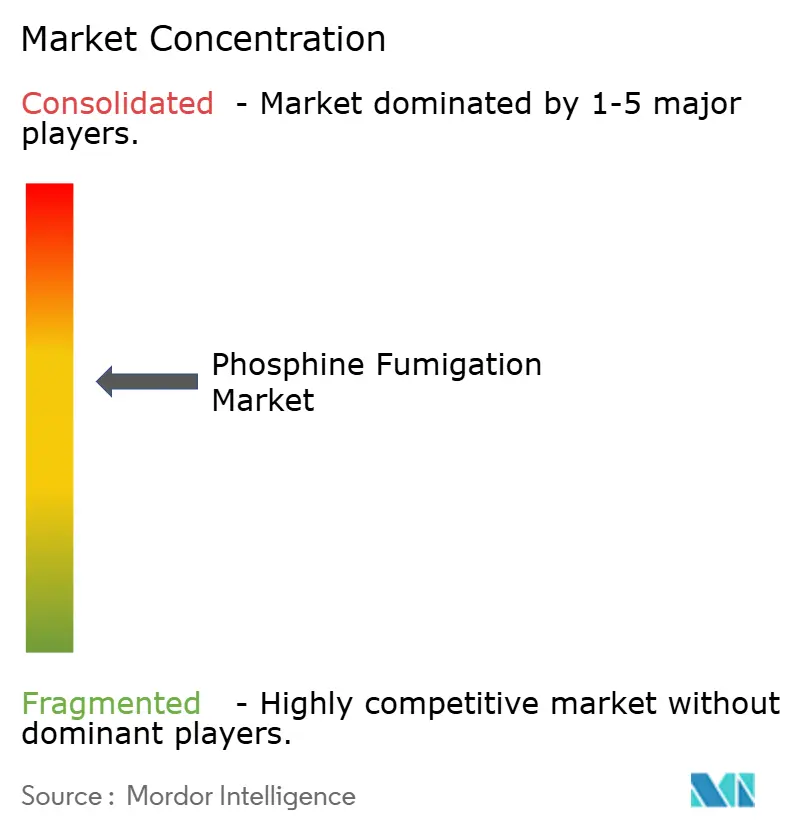

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Phosphine Fumigation Market Analysis by Mordor Intelligence

The phosphine fumigation market size stands at USD 1.90 billion in 2025 and is forecast to reach USD 2.41 billion by 2030, advancing at a 4.9% compound annual growth rate (CAGR). Demand centers on phosphine’s broad-spectrum efficacy, cost advantage over rivals, and alignment with tightening global phytosanitary standards. Record investments in sealed grain-storage infrastructure reinforce growth, rapid shift from methyl bromide, and accelerating adoption of Internet of Things (IoT)-enabled gas monitoring that improves safety compliance. Competitive activity revolves around controlled-release technologies and vertically integrated service models that combine fumigant supply, application, and residue analytics. Simultaneously, documented pest resistance, lower workplace exposure limits, and trained-operator shortages are raising service costs and prompting interest in combination treatments.

Key Report Takeaways

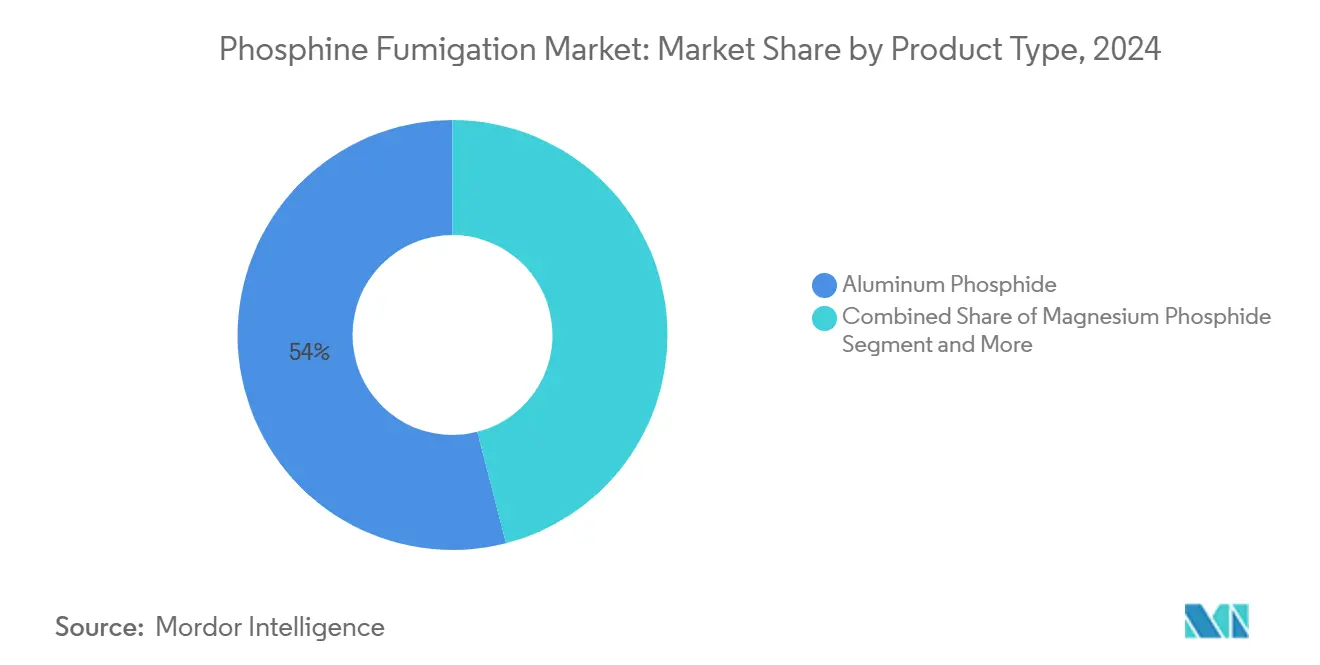

- By product type, aluminum phosphide led with 54% phosphine fumigation market share in 2024, while magnesium phosphide is projected to grow at a 5.9% CAGR to 2030.

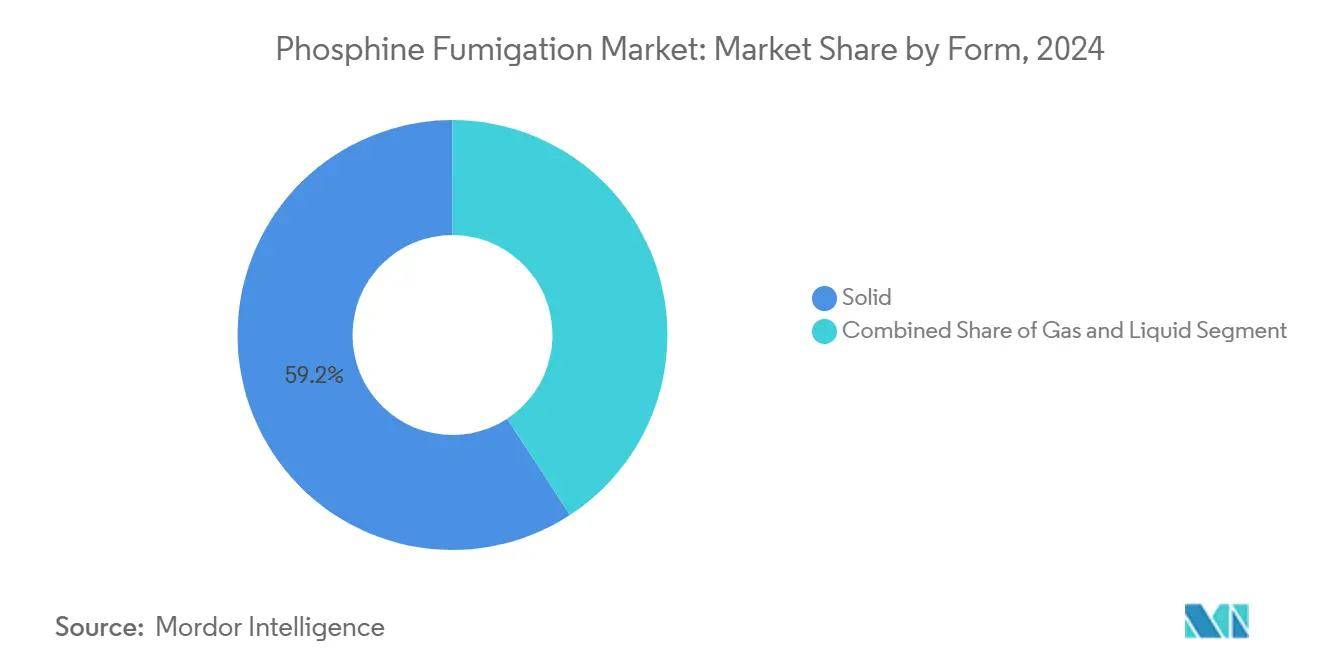

- By form, solid tablets and pellets captured 59.2% share of the phosphine fumigation market size in 2024, gas cylinders and generators offer the fastest expansion at 6.2% CAGR.

- By application, warehouse fumigation accounted for 41.5% of the phosphine fumigation market share in 2024, and raw agricultural commodities are advancing at a 5.4% CAGR through 2030.

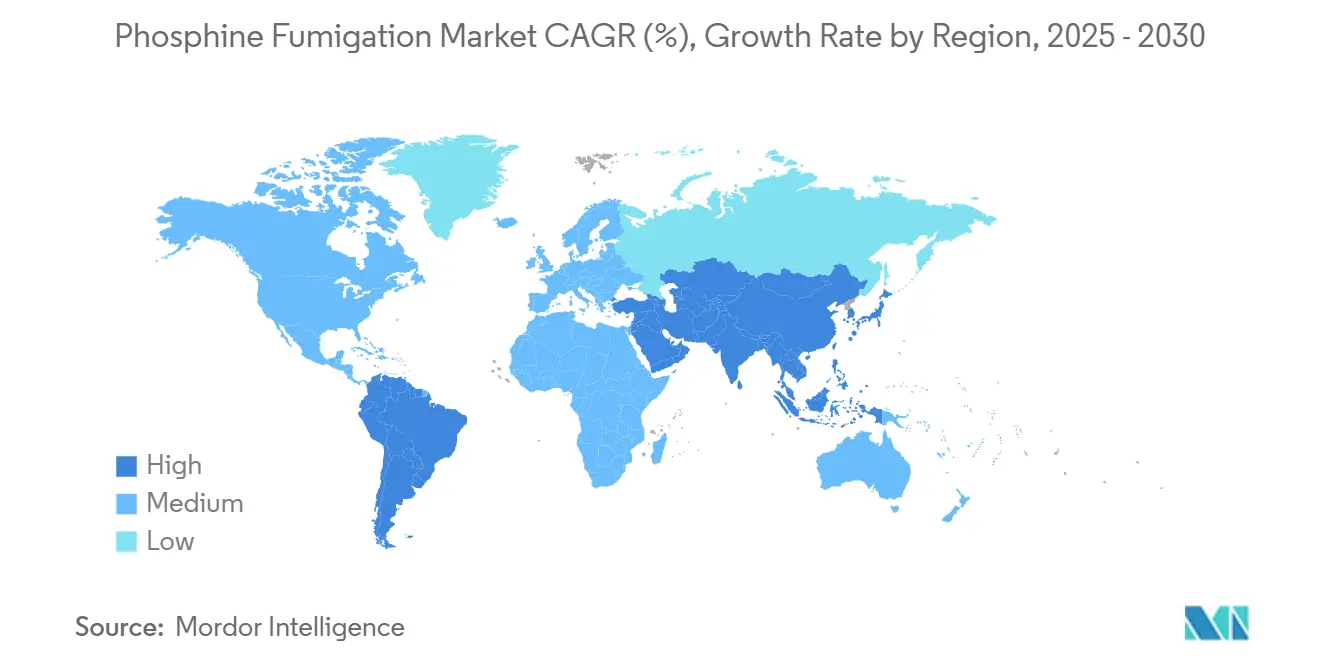

- By geography, North America held a 35.8% share of the phosphine fumigation market size in 2024, while Asia-Pacific is on track for a 6.8% CAGR to 2030.

Global Phosphine Fumigation Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global grain-storage capacity investments | +1.2% | Asia-Pacific, Africa, and South America | Medium term (2–4 years) |

| Accelerated phase-out of methyl bromide in quarantine applications | +0.8% | European Union, North America, and Australia | Long term (≥ 4 years) |

| Tighter phytosanitary rules in cross-border agricultural trade | +0.7% | Major grain-exporting nations worldwide | Short term (≤ 2 years) |

| Lower cost per cubic meter versus alternative fumigants | +0.6% | Price-sensitive emerging markets | Short term (≤ 2 years) |

| IoT-enabled controlled-release phosphine systems | +0.4% | North America and Europe, expanding to Asia-Pacific | Medium term (2–4 years) |

| Surge in on-farm silo installations across emerging economies | +0.5% | Asia-Pacific, South America, and Africa | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising global grain-storage capacity investments

Grain-storage construction programs are the strongest engine behind phosphine fumigation market growth. India’s USD 15 billion plan to add 70 million metric tons of airtight capacity, Egypt’s EUR 153 million (USD 168.3 million) Suez Canal project, and silo expansions across sub-Saharan Africa are reshaping regional demand. Modern sealed bins require scheduled phosphine treatments to maintain commodity quality during longer holding periods. Contractors now design ventilation ducts, pressure-testing protocols, and fumigant recapture systems into blueprints, ensuring phosphine compatibility from the outset. As state food-security funds flow toward rural storage, procurement tenders increasingly specify tablet dosage ranges, gas-tight coatings, and real-time gas sensors, embedding demand for professional fumigation services over the coming decade.[1]Source: Farm Progress, “Farmer interest in biologicals continues to grow,” farmprogress.com

Accelerated phase-out of methyl bromide in quarantine applications

Compliance with the Montreal Protocol has narrowed methyl bromide exemptions, steering quarantine and pre-shipment users toward phosphine. Guidance notes issued by European Union regulators and national plant-protection organizations now list cylinderized phosphine formulations as the preferred alternative for wood packaging and bulk commodity treatments. Research shows that combined phosphine and reduced methyl bromide doses maintain mortality targets while lowering ozone-depleting emissions, giving operators a transitional path that still raises overall phosphine volumes. As exporters update standard operating procedures, suppliers report double-digit order growth for pre-calibrated phosphine cylinders that fit existing fumigation chambers.[2]Source: MDPI Insects, “Chemical and Non-Chemical Control in Stored Product Protection,” mdpi.com

Tighter phytosanitary rules in cross-border agricultural trade

Bilateral agreements, notably under International Standards for Phytosanitary Measures 15, now mandate fumigation certificates with traceable residue data. Phosphine benefits from its long regulatory record and negligible chemical residues, enabling shippers to meet zero-tolerance pest thresholds. In Asia-Pacific trade lanes, customs authorities request electronic uploads of gas-concentration curves, favoring operators equipped with IoT sensors that timestamp every exposure reading. These requirements have driven a spike in service contracts that bundle application, monitoring, and online documentation into one package.

Lower cost per cubic meter versus alternative fumigants

At USD 7.56–USD 9.02 per kilogram for aluminum phosphide, treatment costs undercut sulfuryl fluoride and nitrogen control, especially in large warehouses. Savings are amplified when factoring in lower equipment outlays, minimal energy use, and compatibility with existing tarpaulins. Budget-constrained cooperatives in Southeast Asia increasingly select phosphine tablets over cylinderized fluorides, converting price advantage into rapid market penetration.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent operator-safety and toxicity regulations | -0.9% | Developed markets worldwide | Short term (≤ 2 years) |

| Documented phosphine resistance in key grain-pest species | -0.6% | Areas with intensive fumigation history | Medium term (2–4 years) |

| Licensed-fumigator labor shortages increasing service costs | -0.4% | North America and Europe, spreading globally | Short term (≤ 2 years) |

| Rising demand for residue-free consumer labels | -0.3% | High-income markets with organic focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent operator-safety and toxicity regulations

Australia’s decision to cut workplace phosphine exposure limits from 0.3 parts per million to 0.05 parts per million by December 2026 typifies the global safety clampdown. Similar proposals circulate in the United States Occupational Safety and Health Administration and the European Chemicals Agency. Compliance now requires continuous-read monitors, self-contained breathing apparatus, and third-party exposure audits, adding capital and training expenses. Smaller operators often exit rather than retrofit, nudging customers toward larger providers with certified crews and redundant monitoring gear.[3]Source: University of Iowa, “Meet phosphine, a gas commonly used for industrial fumigation that can damage your lungs, heart and liver,” research.uiowa.edu

Documented phosphine resistance in key grain-pest species

Field studies in Australia and India show higher survival rates of Rhyzopertha dominica and Sitophilus oryzae after standard exposures. Resistance forces fumigators to extend treatment times, raise dosage, or blend phosphine with carbon dioxide or ethyl formate, inflating chemical use and labor hours. Researchers are mapping resistance genes and trialing rotation chemistries, yet commercial scalability remains uncertain, creating short-to-medium-term headwinds.

Segment Analysis

By Product Type: Aluminum Phosphide Maintains Commanding Share as Magnesium Phosphide Gains Traction

Aluminum phosphide captured 54% of the phosphine fumigation market share in 2024 on the back of proven efficacy, abundant global supply, and mature stewardship guidelines. Its contribution to the phosphine fumigation market size remains dominant even as buyers scrutinize safety norms, because handlers are already trained on dosage charts and disposal protocols. The segment benefits from economies of scale, with over one hundred registered manufacturers in India alone offering competitive pricing that locks in customer loyalty.

Magnesium phosphide is expanding at a 5.9% CAGR through 2030 by addressing evolving safety requirements. Its moisture-activated controlled-release profile reduces peak gas concentrations and lowers ignition risks, features that appeal to operators bound by tighter occupational limits. Cylinderized blends that combine magnesium phosphide with carbon dioxide further differentiate the segment, allowing non-flammable delivery and remote activation. Calcium phosphide and niche zinc phosphide products occupy specialized pockets such as rodent bait production, but they do not materially shift overall market dynamics.

Note: Segment shares of all individual segments available upon report purchase

By Form: Solid Tablets Dominate While Gas Systems Accelerate

Solid tablets and pellets accounted for 59.2% of the phosphine fumigation market size in 2024, underlining decades of operational familiarity. Rural cooperatives value their straightforward insertion into silo headspaces and the absence of high-pressure storage vessels. Tablet sales align closely with seasonal harvest peaks, creating predictable demand cycles that sustain widespread distributor networks.

Gas cylinders and generators, though starting from a smaller base, record the fastest expansion at 6.2% CAGR. Next-generation products such as ECO2FUME premix phosphine with carbon dioxide to suppress flammability and allow continuous flow through metered valves, enabling precise concentration control compliant with stringent safety codes. Liquid on-site generation, meanwhile, addresses mega-facilities where centralized dosing units feed multiple bins via manifold systems. The shift toward gas systems dovetails with increased automation and remote monitoring, particularly in North American export terminals where downtime penalties are steep.

Note: Segment shares of all individual segments available upon report purchase

By Application: Warehouses Lead but On-Farm Commodity Storage Rises Fast

Warehouses represented 41.5% of the market share in 2024. Large commercial elevators and logistics hubs schedule routine treatments that integrate with inventory management software and residue-reporting dashboards. The segment’s scale supports specialized service providers that operate nationwide fleets of applicator trucks and maintain in-house analytical labs for post-treatment clearance.

Raw agricultural commodities stored on farms are forecast for the highest CAGR at 5.4% through 2030 as growers invest in sealed silos and flat storage to hedge volatile commodity prices. Tablet starter kits bundled with low-cost gas detectors empower producers to self-treat, expanding the customer base beyond traditional elevator networks. Processed food storage maintains a steady demand where food safety audits require fumigants with minimal residues. Other uses, spanning quarantine treatments and tobacco warehouses, remain niche yet command premium service fees owing to strict treatment specifications.

Geography Analysis

North America retained the largest share of the market at 35.8% in 2024. Extensive grain export corridors, notably the Mississippi River system and Pacific Northwest ports, rely on routine phosphine treatments to comply with importing nations' requirements. Regulatory agencies have issued detailed guidance on sensor calibration, cylinder handling, and worker reentry intervals, positioning the region as an early adopter of IoT-enabled monitoring. Canada contributes through pulse and canola export logistics, while Mexico’s maize import program enforces fumigation certificates for every railcar.

Asia-Pacific posts the fastest CAGR at 6.8% through 2030, propelled by sovereign food-security agendas. India’s USD 15 billion plan to triple wheat storage, China’s modernization of state reserves, and Australia’s upgrade of bulk export terminals combine to lift regional fumigant volumes. Government tenders increasingly specify phosphine-ready aeration floors and gas-tight seals, embedding demand during construction. Developed economies such as Japan maintain high service intensity due to strict residue limits on imported rice and feed grains.

Europe represents a mature yet regulatory-driven market. Restrictions on methyl bromide and carbon-intensive fumigants elevate phosphine as the default option for portside grain and wood-packaging treatments. Government subsidies encourage the adoption of non-flammable cylinder blends and real-time gas analytics that cut operator exposure. Africa and the Middle East, though smaller today, experience rapid infrastructure build-outs; Egypt’s EUR 153 million (USD 168.3 million) Suez Canal facility exemplifies turnkey projects that embed fumigation robotics and cloud-based reporting from day one. South America maintains a steady demand, mirrored by soybean and corn export flows, with Brazilian cooperatives increasingly outsourcing to full-service fumigation contractors.

Competitive Landscape

The phosphine fumigation market is moderately concentrated; the top five companies command 55.2% combined share. UPL leads global volume with its QuickPhos tablets and pellets packaged in humidity-tight aluminum flasks and backed by comprehensive stewardship manuals. Syensqo, formerly Solvay, differentiates through ECO2FUME and VAPORPH3OS cylinderized blends that deliver non-flammable mixtures and integrate with digital flow regulators. Douglas Products markets PH3 tablets via distributor alliances such as Farmers Business Network Direct, expanding rural reach and supplying detailed safety documentation.

Detia Degesch GmbH and Draslovka round out the leading group, emphasizing research on stabilized formulations and resistance-management protocols. Competitive strategies increasingly center on vertical integration: manufacturers acquire regional service companies to secure downstream margins and control application quality. Technology partnerships with gas-sensor specialists aim to embed telemetry in every cylinder, enabling subscription revenue from cloud dashboards that track concentration curves and generate compliance certificates. Mid-tier regional operators capitalize on local customer relationships but face cost pressure as regulatory audits demand capital-intensive safety gear and data-logging systems.

Innovation is accelerating: CaptSystemes launched PhosCapt-MP for large bins, automating gas circulation via fan-assisted manifolds and reducing concentration variability. Central Life Sciences updated insect-growth-regulator blends to complement fumigation schedules and delay resistance onset. Rollins Incorporated’s Industrial Fumigant Company reported double-digit growth after adding drone-based leak inspections and customer portals displaying real-time gas readings.

Phosphine Fumigation Industry Leaders

-

Detia Degesch GmbH

-

Douglas Products

-

Draslovka

-

UPL Ltd

-

Nufarm Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: UPL integrated its post-harvest business (DECCO) with Advanta Seeds to streamline agricultural solutions. This integration strengthened its phosphine-based fumigation portfolio through a unified agricultural technology strategy.

- February 2025: Douglas Products established a partnership with Target Specialty Products to distribute ProFume and Vikane fumigants across the United States. The fumigants serve post-harvest and structural pest control applications, expanding Douglas Products' presence in agricultural fumigation.

- April 2024: Draslovka consolidated its agricultural fumigation business under the new brand INTRESO Group. INTRESO now manages EDN, BLUEFUME, and eFUME globally, with a focus on developing sustainable fumigation alternatives to phosphine.

Global Phosphine Fumigation Market Report Scope

| Aluminum Phosphide |

| Magnesium Phosphide |

| Calcium Phosphide |

| Others (Zinc Phosphide, Hydrogen Cyanide, etc.) |

| Solid (Tablets / Pellets) |

| Gas (Cylinders / Generators) |

| Liquid (On-site Gas Generation) |

| Stored Processed Food |

| Raw Agricultural Commodities |

| Warehouses |

| Others (Quarantine Treatments, Tobacco Warehouses, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Aluminum Phosphide | |

| Magnesium Phosphide | ||

| Calcium Phosphide | ||

| Others (Zinc Phosphide, Hydrogen Cyanide, etc.) | ||

| By Form | Solid (Tablets / Pellets) | |

| Gas (Cylinders / Generators) | ||

| Liquid (On-site Gas Generation) | ||

| By Application | Stored Processed Food | |

| Raw Agricultural Commodities | ||

| Warehouses | ||

| Others (Quarantine Treatments, Tobacco Warehouses, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the phosphine fumigation market?

The phosphine fumigation market is valued at USD 1.90 billion in 2025.

How fast is the phosphine fumigation market expected to grow?

The market is projected to expand at a 4.9% CAGR and reach USD 2.41 billion by 2030.

Which product segment leads in phosphine fumigation?

Aluminum phosphide holds the largest share at 54% in 2024.

Why is phosphine preferred over methyl bromide?

Phosphine offers broad-spectrum efficacy without ozone-depletion issues and meets evolving phytosanitary regulations.

Page last updated on: