Orthopedic Navigation Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

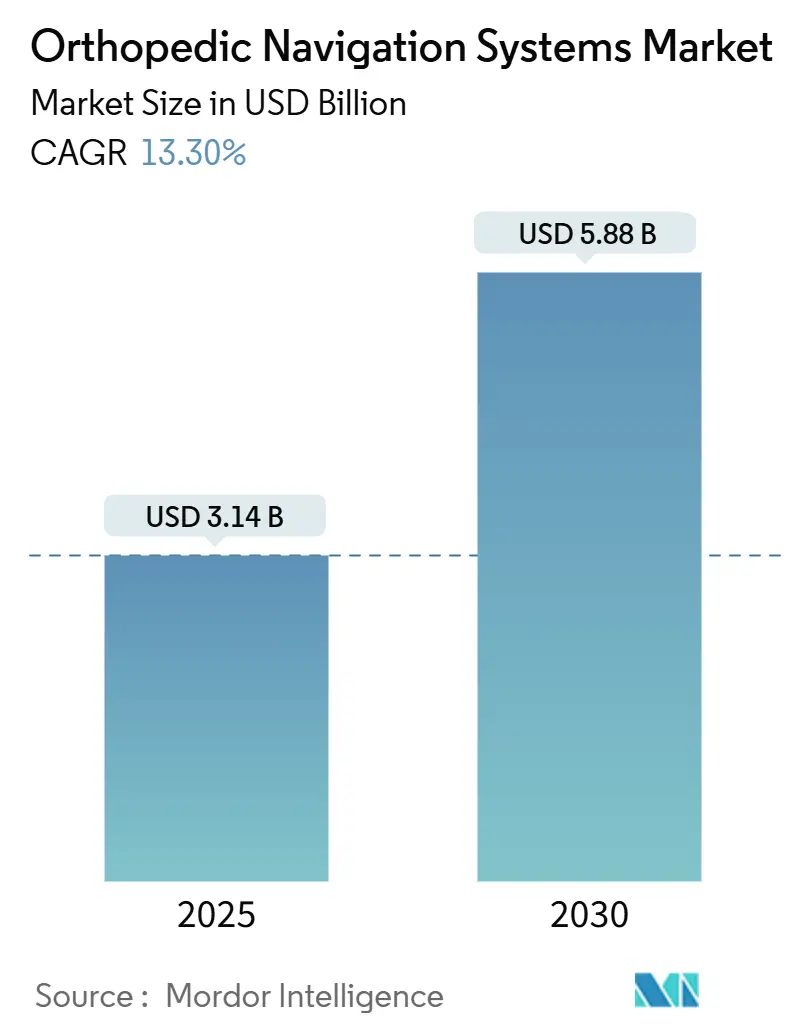

| Market Size (2025) | USD 3.14 Billion |

| Market Size (2030) | USD 5.88 Billion |

| Growth Rate (2025 - 2030) | 13.30% CAGR |

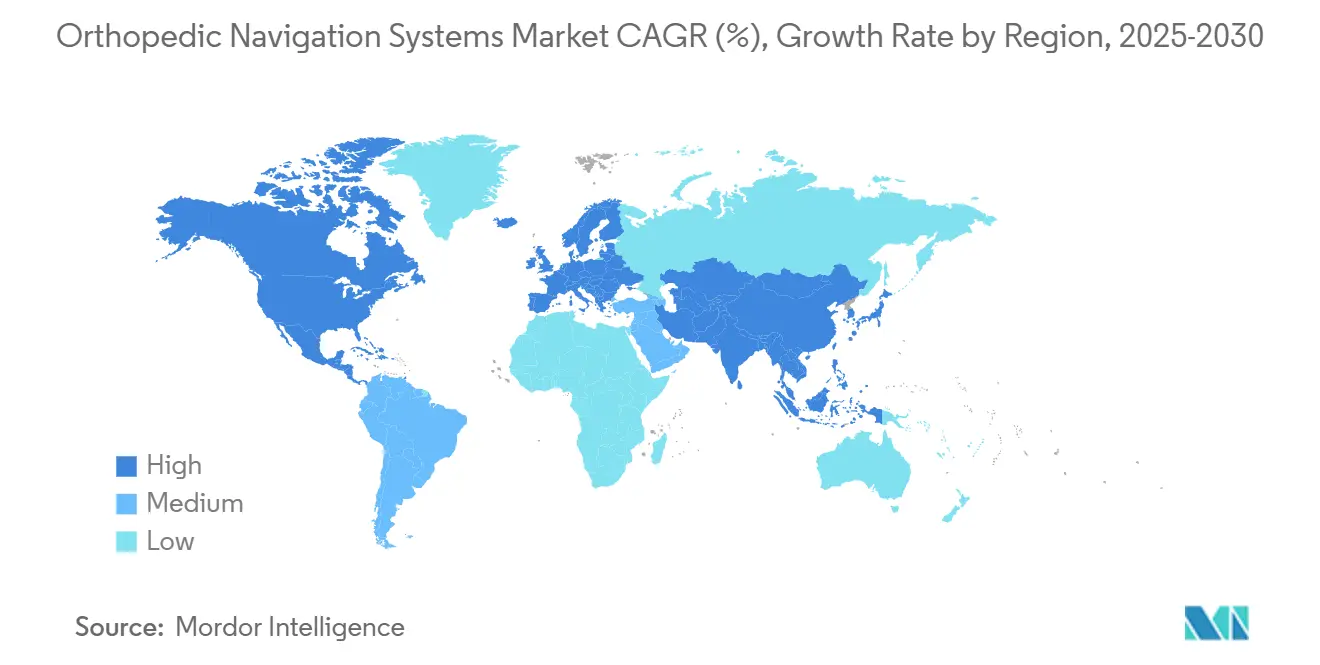

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

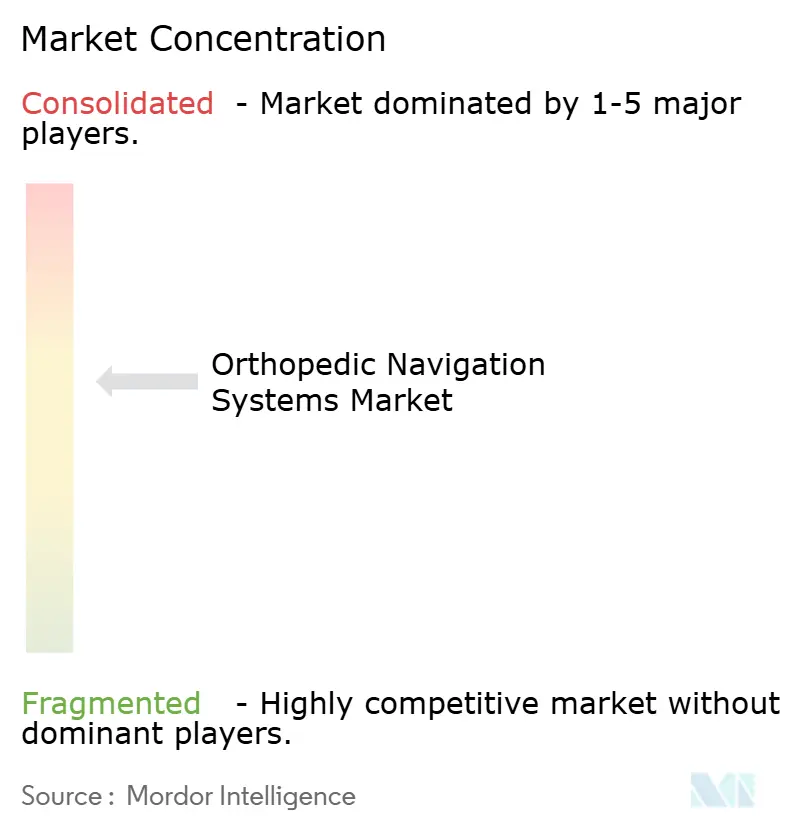

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Orthopedic Navigation Systems Market Analysis by Mordor Intelligence

The orthopedic navigation systems market reached USD 3.14 billion in 2025 and is projected to climb to USD 5.88 billion by 2030, translating to a 13.30% CAGR. Growth stems from a convergence of aging populations, rising minimally invasive procedure volumes, and continuous imaging and software innovations that allow precise implant placement even in constrained anatomies. Health-system cost-containment initiatives now favor first-time surgical accuracy, encouraging hospitals and ambulatory surgical centers (ASCs) to invest in guidance platforms that reduce revision risk. Technology vendors are responding with integrated optical, electromagnetic, and augmented-reality (AR) solutions that shorten setup times and improve intra-operative workflow. At the same time, value-based purchasing in North America and Europe rewards lower complication rates, while emerging markets in Asia Pacific are scaling orthopedic capacity and demanding the same precision standards. Together, these factors underpin the current momentum of the orthopedic navigation systems market.

Key Report Takeaways

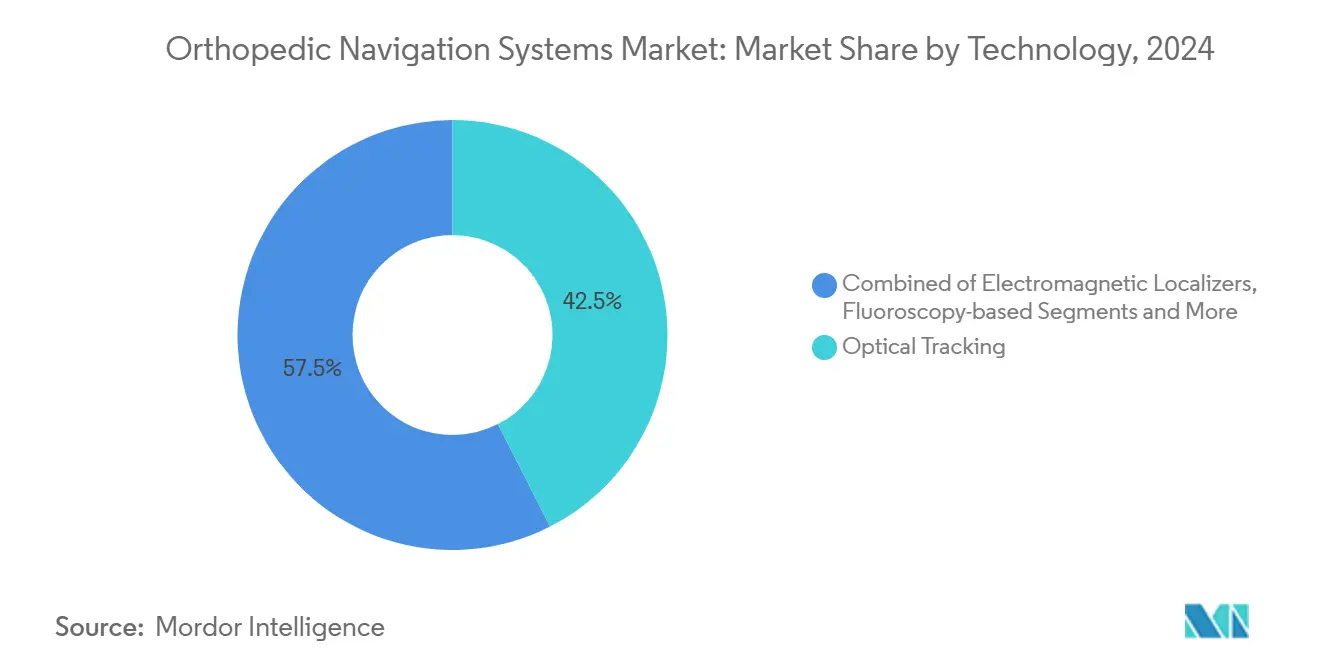

- By technology, optical tracking led with 42.5% of the orthopedic navigation systems market share in 2024, while AR/mixed-reality is forecast to expand at 18.6% CAGR through 2030.

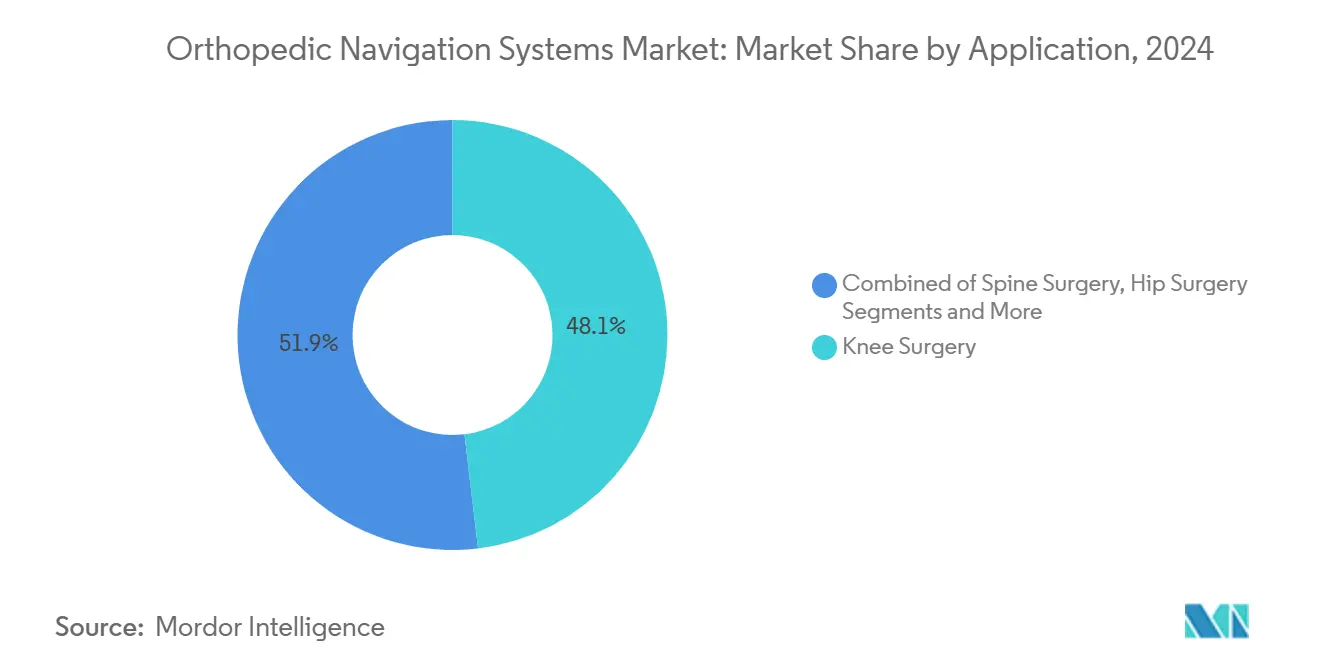

- By application, knee surgery accounted for 48.1% of the orthopedic navigation systems market size in 2024; shoulder and upper-extremity procedures are advancing at 14.2% CAGR to 2030.

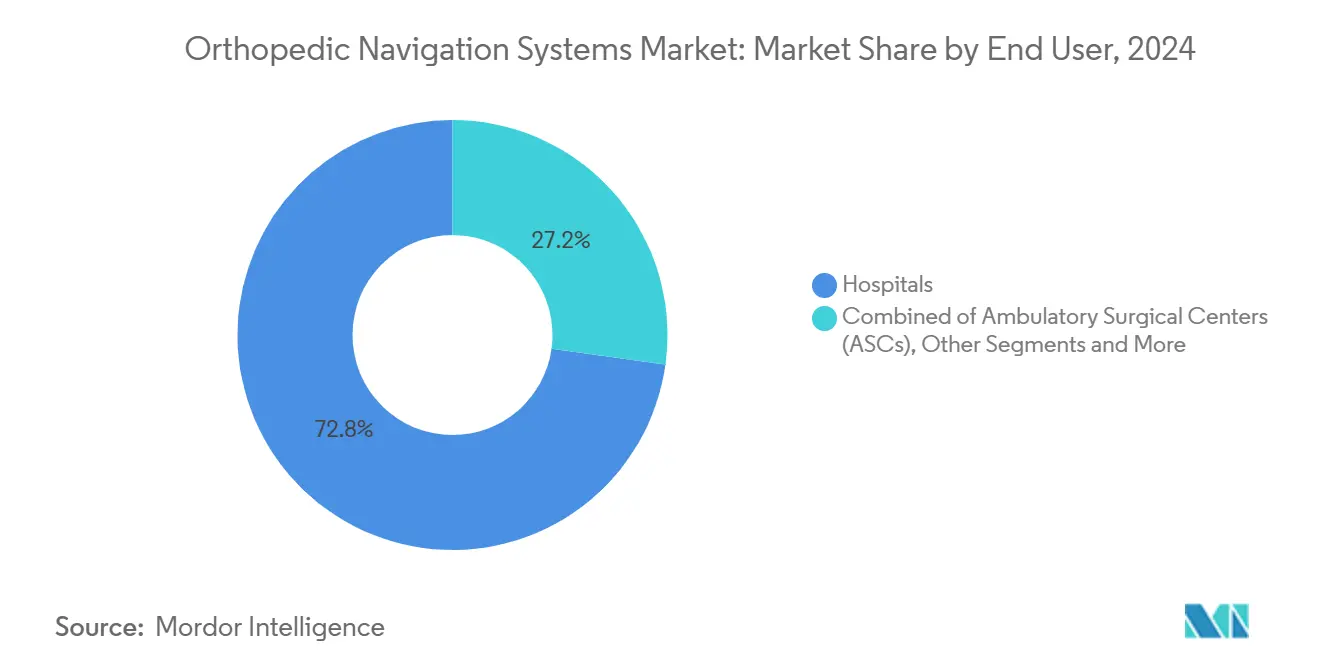

- By end user, hospitals retained 72.8% revenue share of the orthopedic navigation systems market in 2024, whereas ASCs are growing fastest at 11.9% CAGR through 2030.

- By geography, North America held 41.2% share of the orthopedic navigation systems market in 2024, while Asia Pacific is the fastest-growing region at 9.8% CAGR.

Global Orthopedic Navigation Systems Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of minimally invasive orthopedic procedures | +2.80% | Global; early gains in North America & EU | Medium term (2-4 years) |

| Expanding installed base of robotic-assisted surgery platforms | +2.10% | North America core; spill-over to APAC | Long term (≥4 years) |

| Advances in real-time imaging & sensor fusion for intra-op guidance | +1.90% | Global; high-volume centers | Short term (≤2 years) |

| Growing burden of musculoskeletal disorders in ageing populations | +2.30% | Global; developed markets | Long term (≥4 years) |

| Hand-held & pin-less low-cost devices targeting ASC settings | +1.70% | North America & EU; expanding to APAC | Medium term (2-4 years) |

| FDA Real-World Evidence programs accelerating post-market data use | +1.20% | US-centric; global spillover | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Minimally Invasive Orthopedic Procedures

Surgeons increasingly favor smaller incisions that minimize tissue trauma yet still demand sub-millimeter implant accuracy. Navigation assists by guiding instruments in three-dimensional space, enabling 93% alignment within ±2° during total knee arthroplasty.[1]W. Hee, “Computer-Assisted Total Knee Arthroplasty Accuracy,” Hindawi, hindawi.comEconomic benefits accrue when shorter inpatient stays and quicker rehabilitation reduce payer spend. Fluoroscopy-integrated systems further cut radiation exposure by 91.8% compared with conventional methods.

Expanding Installed Base of Robotic-Assisted Surgery Platforms

Hospitals that already rely on robotics are layering navigation software on existing arms to form comprehensive ecosystems. Stryker’s forthcoming Mako 4 release extends its footprint from hips and knees to spine and shoulders, embedding the Q Guidance module for seamless imaging–robot synchronization. Peer-reviewed research shows robotic navigation flattens the learning curve in hip arthroplasty for early-career surgeons, achieving veteran-level accuracy sooner.[3]N. Kayani et al., “Robotic Hip Arthroplasty Learning Curve,” Bone & Joint Open, boneandjointopen.boneandjoint.org.uk

Advances in Real-Time Imaging & Sensor Fusion for Intra-Op Guidance

Machine-vision cameras, optical trackers, and electromagnetic coils now merge data streams to produce live anatomic maps. In pediatric scoliosis corrections, such fusion cut fluoroscopy time 68% and radiation 66%. AR overlays place holographic anatomical landmarks directly on the field of view, reducing cognitive load, while AI algorithms predict drill trajectories that avert cortical breaches before they happen.

Growing Burden of Musculoskeletal Disorders in Ageing Populations

The growing burden of musculoskeletal diseases is likely to increase demand for orthopedic navigation systems is anticipated to boost the segment growth. For instance, according to the study published in the Journal of Indian Rheumatology Association, the overall prevalence of primary knee in big cities of India was 33.2%, 19.3% in small cities, 18.3% in towns, and 29.2% in villages. The study also demonstrated that the prevalence of symptomatic primary osteoarthritis knee in urban areas is much higher than reported in rural regions in India. Older bone often presents atypical anatomy, making precision crucial to avoid early loosening. Navigation reduces revision rates and delivers quality-adjusted life-year gains at USD 45,554 per QALY in knee replacement.[2]M. Kalra, “Radiation Dose Reduction in Knee Replacement,” AJR, ajronline.org

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & per-procedure costs of navigation platforms | -2.40% | Global; acute in emerging markets | Medium term (2-4 years) |

| Steep learning curve & workflow disruption for surgical teams | -1.80% | Global; varies by institution | Short term (≤2 years) |

| Stringent multi-region regulatory approval & device-recall risk | -1.60% | US & EU zones | Medium term (2-4 years) |

| Competitive cannibalization by fully integrated orthopedic robots | -1.40% | North America & EU; expanding to APAC | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Capital & Per-Procedure Costs of Navigation Platforms

Systems list from USD 475,000 to more than USD 1 million, while disposables can add USD 442–1,500 each case. Reimbursement gaps often push facilities to self-fund upgrades. Some evidence shows neutrality is achieved when navigation averts 17 spine revisions per center. Lower-cost handheld models are gradually easing the financial barrier for mid-size hospitals and ASCs.

Steep Learning Curve & Workflow Disruption for Surgical Teams

Surgeons may need 20–30 cases before operative times normalize; early cases lengthen by 6–15 minutes. OR staff must adjust positioning, cable management, and sterile technique, adding friction. Surveys indicate 63.5% of spine surgeons cite longer times as a drawback, yet AI-guided interfaces that automate registration are driving faster mastery.

Segment Analysis

By Technology: Optical Leadership, AR/MR Momentum

Optical systems controlled 42.5% of the orthopedic navigation systems market in 2024, thanks to well-validated camera arrays that deliver sub-millimeter accuracy during high-volume knee replacements. Augmented- and mixed-reality solutions now post the segment’s fastest 18.6% CAGR, propelled by head-mounted displays that place holographic guides inside the surgeon’s field of view and remove line-of-sight constraints common to fixed cameras. Electromagnetic trackers are gaining ground for spine work where metallic instruments obscure optical markers, whereas fluoroscopy-based guidance remains a staple in trauma rooms needing instant imaging. MRI-specific platforms hold a niche for soft-tissue-driven tumor resections that depend on detailed contrast.

Competition is intensifying as incumbents meld sensors, GPUs, and cloud analytics into single packages. Smith+Nephew’s TESSA Spatial Surgery System runs in real-time on NVIDIA chips to guide ACL reconstruction without external cameras, illustrating the shift toward compact hybrid devices. Proprietary AI modules now auto-segment bone on intra-op scans and fine-tune instrument paths, trimming manual steps. With optical reliability already proven, companies seek differentiation by shrinking footprints, cutting cables, and integrating AR. As price points drop, the orthopedic navigation systems market will likely see technology overlap rather than a single-modality winner.

Note: Segment shares of all individual segments available upon report purchase

By Application: Knee Dominance, Shoulder Surge

Knee procedures generated 48.1% of 2024 revenue share as decades of randomized evidence show axis alignment within ±2° in over 90% of navigated knees, compelling payers to reimburse guidance for complex deformities. Spine surgeries capture an expanding share because misplaced pedicle screws risk neurologic harm, prompting adoption even in lower-resource settings that cannot afford full robotics. Hip arthroplasty is also benefiting from direct-anterior approaches, which demand precise cup inclination and version.

Shoulder and upper-extremity operations are poised for 14.2% CAGR, the fastest within the orthopedic navigation systems industry, as athletes and aging populations pursue motion-preserving implants. Stryker’s Tornier portfolio now couples 3D planning with intra-op trackers that confirm glenoid axis, pushing adoption in centers of excellence. Trauma and sports medicine groups favor handheld devices that enable quick deployment at odd hours. Emerging subspecialties, such as foot-and-ankle reconstruction, will further diversify demand once disposable pricing aligns with ambulatory margins.

Note: Segment shares of all individual segments available upon report purchase

By End User: Hospitals Hold Sway as ASCs Accelerate

Hospitals retained 72.8% of the orthopedic navigation systems market share in 2024 by leveraging capital budgets and multi-specialty case volumes that amortize equipment quickly. Academic centers prioritize navigation for resident training and as live-data generators feeding registries that benchmark implant longevity. Integration with electronic health records lets hospitals mine outcomes and negotiate bundled-payment premiums from insurers keen on predictable results.

ASCs are the fastest riser at 11.9% CAGR, encouraged by policy shifts that reimburse more joint replacements outside hospital walls. Portable, pin-less devices weighing under 3 kg fit tight operating suites and avoid lengthy turnover. Sg2 projects double-digit orthopedic case migration to ASCs, and navigation helps these centers defend quality metrics needed for payer contracts. Specialty clinics and global charity hospitals represent smaller segments but illustrate how stripped-down guidance platforms can thrive in varied economic contexts.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America accounted for 41.2% of sales in 2024, reflecting early adoption, clear CPT codes that reimburse navigation in complex joints, and the presence of vendors able to provide 24/7 field support. Migration of hip and knee replacements to ASCs intensifies demand for compact platforms that replicate hospital-level precision. A 26% cost reduction versus hospital outpatient departments has been documented when ASCs deploy navigated protocols for joint work. Canada mirrors this path with provincial funding programs that incentivize data-verified outcomes, while Mexico gains from cross-border device trade and private hospital growth.

Europe forms the next largest block, with Germany, the United Kingdom, and France adopting stringent evidence-based guidelines favoring navigation when alignment accuracy predicts longevity of high-priced implants. Diverse reimbursement regimes mean uptake varies—statutory payers in Germany cover navigation disposables, whereas southern markets rely on private insurers or self-pay models. Academic hubs such as Charité in Berlin and Oxford University Hospitals publish robust registries that validate technology, influencing continental standards. Emerging Central-Eastern nations now modernize orthopedic departments with EU recovery funds and see navigation as a path to curb expensive revisions.

Asia Pacific is the fastest-growing region, posting a 9.8% CAGR to 2030 as demographic aging meets rising income levels. India’s arthroplasty implant sector is expanding near 25% CAGR, yet limited awareness of joint-replacement options caps immediate volumes. China’s penetration remains low, with only 8.31% of hip surgeons using navigation or robotics, but state 5-year plans targeting advanced healthcare are expected to lift utilization. Japan and South Korea already operate mature reimbursement schemes, while Australia’s national joint registry proves the link between navigation and lower revision risk, reinforcing adoption. Southeast Asian markets draw medical tourists seeking high-tech surgery, nudging private hospitals to invest in navigation as a competitive differentiator.

Competitive Landscape

The orthopedic navigation systems market is moderately fragmented. Global device majors bundle navigation into broad implant portfolios, giving them cross-selling leverage and multi-year service contracts. Stryker unifies its Mako robots with the Q Guidance camera platform, offering one interface across hips, knees, shoulders, and spine procedures. Zimmer Biomet’s acquisition of OrthoGrid brings AI-driven fluoroscopy analytics, rounding out its ROSA robot line. Smith & Nephew enters spatial surgery with TESSA, underscoring a shift from passive tracking to immersive AR guidance.

Specialists such as Brainlab, 7D Surgical, and OrthAlign carve niches through ultra-fast camera registration, flash imaging, or disposable-only business models that remove capital hurdles. New entrants exploit machine-learning algorithms licensed from academic labs to deliver tracker-less navigation that depends solely on intra-operative imaging, sidestepping bulky arrays. Partnerships flourish: Smith & Nephew collaborates with JointVue for ultrasound planning, while Zimmer Biomet distributes THINK Surgical’s wireless knee robot for ASCs. Vendors also mine data lakes created by connected robots to build predictive maintenance and derive implant-longevity insights, strengthening post-sale relationships.

Competitive cannibalization arises as fully integrated robots threaten stand-alone navigation sales. Yet hospitals still purchase camera systems where volume or budget cannot justify full robotics, keeping the addressable base wide. Handheld, pin-less products appeal in cost-sensitive geographies and among surgeons resistant to large consoles. Over the forecast, differentiation will center on AI-powered automation, reduced learning curves, and interoperability with operating-room integration platforms rather than on pure tracking accuracy, which is now table stakes.

Orthopedic Navigation Systems Industry Leaders

-

Stryker

-

Zimmer Biomet

-

Smith + Nephew

-

Medtronic

-

NuVasive

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Smith & Nephew launched the TESSA Spatial Surgery System with NVIDIA GPU processing for ACL reconstruction, introducing real-time navigation blended with AR overlays.

- March 2025: Stryker unveiled Mako 4, featuring integrated Q Guidance for spine and shoulder, plus the first robotic hip-revision capability ahead of its late-2025 commercial release.

- February 2025: Enovis agreed to acquire LimaCorporate for EUR 800 million (USD 860 million), adding 3D-printed Trabecular Titanium implants to its reconstruction portfolio.

- August 2024: Zimmer Biomet closed the OrthoGrid Systems purchase, bringing fluoroscopy-based Hip AI metrics into its navigation suite.

- July 2024: Stryker gained FDA 510(k) clearance for Spine Guidance 5 with Copilot, which pairs smart instruments with auditory feedback for enhanced precision.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines orthopedic navigation systems as integrated hardware-software platforms that transform pre-operative imaging data into live, three-dimensional guidance, allowing surgeons to align implants accurately during knee, hip, spine, and other musculoskeletal procedures. Solutions covered include optical, electromagnetic, fluoroscopy-based, and emerging augmented-reality trackers sold as capital equipment, single-use disposables, and bundled service contracts.

Scope Exclusion: Veterinary and purely diagnostic imaging tools are out of scope.

Segmentation Overview

- By Technology

- Electromagnetic Localizers

- Optical Tracking

- Fluoroscopy-based

- MRI-based

- Augmented / Mixed Reality Systems

- Other Emerging Technologies

- By Application

- Knee Surgery

- Spine Surgery

- Hip Surgery

- Shoulder & Upper-Extremity

- Trauma & Sports Injury

- Other Applications

- By End User

- Hospitals

- Ambulatory Surgical Centers (ASCs)

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed orthopedic surgeons across North America, Europe, and Asia Pacific, procurement heads at hospital chains, ASC finance managers, and product managers at device OEMs. These discussions validated price bands, adoption hurdles, refresh cycles, and regional mix shifts that secondary sources alone could not capture.

Desk Research

We began with public datasets such as the OECD Health Surgery Statistics, WHO Global Health Observatory, United States FDA 510(k) clearance files, and Eurostat hospital discharge records, which anchor procedure counts and regulatory timelines. Additional insight came from orthopedic trade associations, peer-reviewed journals like The Journal of Arthroplasty, company 10-K filings, and paid intelligence from D&B Hoovers that clarifies corporate revenue splits. This list is illustrative; numerous other open and subscription sources were consulted for fact-checking and context building.

Market-Sizing & Forecasting

A top-down procedure-reconstruct model converts annual knee, hip, and spine surgery volumes into potential navigation placements, which are then tested with selective bottom-up roll-ups of installed base data and average selling price checks. Key variables include elective knee replacement volumes, ASC share of orthopedic cases, capital expenditure budgets, optical versus electromagnetic system mix, and average device life. Multivariate regression on these drivers, tempered by surgeon-informed scenario analysis, produces the 2025-2030 forecast. Gaps in bottom-up counts, especially in emerging markets, are bridged by calibrated penetration rates drawn from primary interviews.

Data Validation & Update Cycle

Outputs move through anomaly screening, senior-analyst peer review, and a final pre-publish refresh. We update the model each year, and sooner if material events, major recalls, reimbursement changes, or landmark approvals shift market fundamentals.

Why Mordor's Orthopedic Navigation Systems Baseline Earns Decision-Maker Confidence

Published estimates often diverge because firms choose different product mixes, pricing assumptions, and refresh cadences. By anchoring volumes to audited procedure statistics and vetting every ASP with front-line clinicians, our team delivers a figure buyers can trace back to recognizable levers.

Key gap drivers behind other numbers include narrower scopes that exclude hardware service revenues, aggressive or conservative uptake rates for robotics-ready systems, and less frequent model refreshes that overlook recent ASC expansion.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.14 Bn (2025) | Mordor Intelligence | - |

| USD 3.26 Bn (2025) | Global Consultancy A | Counts navigation revenues only from listed manufacturers, with limited surgery-volume triangulation |

| USD 0.35 Bn (2024) | Trade Journal B | Treats navigation purely as software add-ons, excluding capital consoles and long-term service contracts |

These comparisons underscore how our disciplined variable selection and annual refresh cadence give clients a balanced, transparent baseline they can rely on for strategic planning.

Key Questions Answered in the Report

What is the current Orthopedic Navigation Systems Market size?

The Orthopedic Navigation Systems Market is projected to register a CAGR of 10.01% during the forecast period (2025-2030)

Who are the key players in Orthopedic Navigation Systems Market?

Stryker, Zimmer Biomet, Smith + Nephew, Medtronic and NuVasive are the major companies operating in the Orthopedic Navigation Systems Market.

Which is the fastest growing region in Orthopedic Navigation Systems Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Orthopedic Navigation Systems Market?

In 2025, the North America accounts for the largest market share in Orthopedic Navigation Systems Market.

What years does this Orthopedic Navigation Systems Market cover?

The report covers the Orthopedic Navigation Systems Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Orthopedic Navigation Systems Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: