Nuclear Battery Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

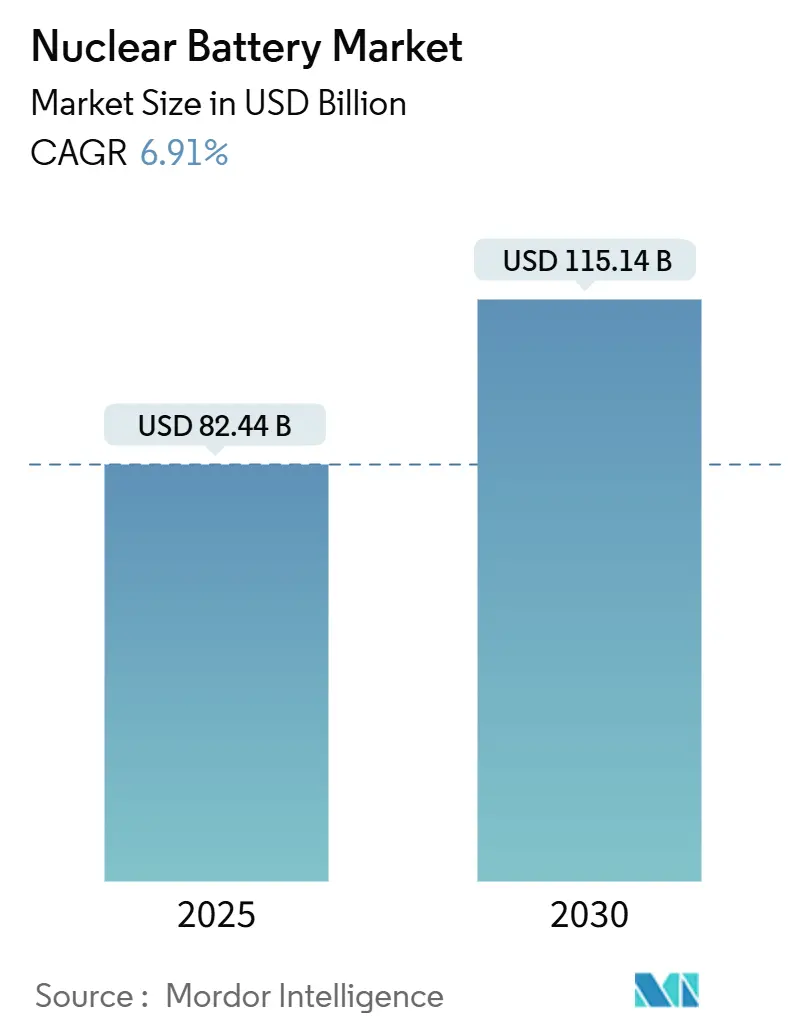

| Market Size (2025) | USD 82.44 Billion |

| Market Size (2030) | USD 115.14 Billion |

| Growth Rate (2025 - 2030) | 6.91% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Nuclear Battery Market Analysis by Mordor Intelligence

The Nuclear Battery Market size is estimated at USD 82.44 billion in 2025, and is expected to reach USD 115.14 billion by 2030, at a CAGR of 6.91% during the forecast period (2025-2030).

Consistent deep-space mission funding, exponential growth of long-life IoT sensors, and rapid gains in diamond-semiconductor conversion efficiency are expanding the addressable opportunity. Space agencies continue to favor radioisotope power sources for missions beyond Jupiter’s orbit, where solar panels lose effectiveness. Simultaneously, commercial ventures are standardizing nuclear batteries for fifty-year remote sensor deployments that remove costly field maintenance. Ongoing government isotope production programs mitigate supply risk, while venture funding accelerates pilot production lines for betavoltaic cells. Together, these forces position the nuclear battery market for sustained double-digit demand growth even as RTGs defend their incumbency in high-power applications.

Key Report Takeaways

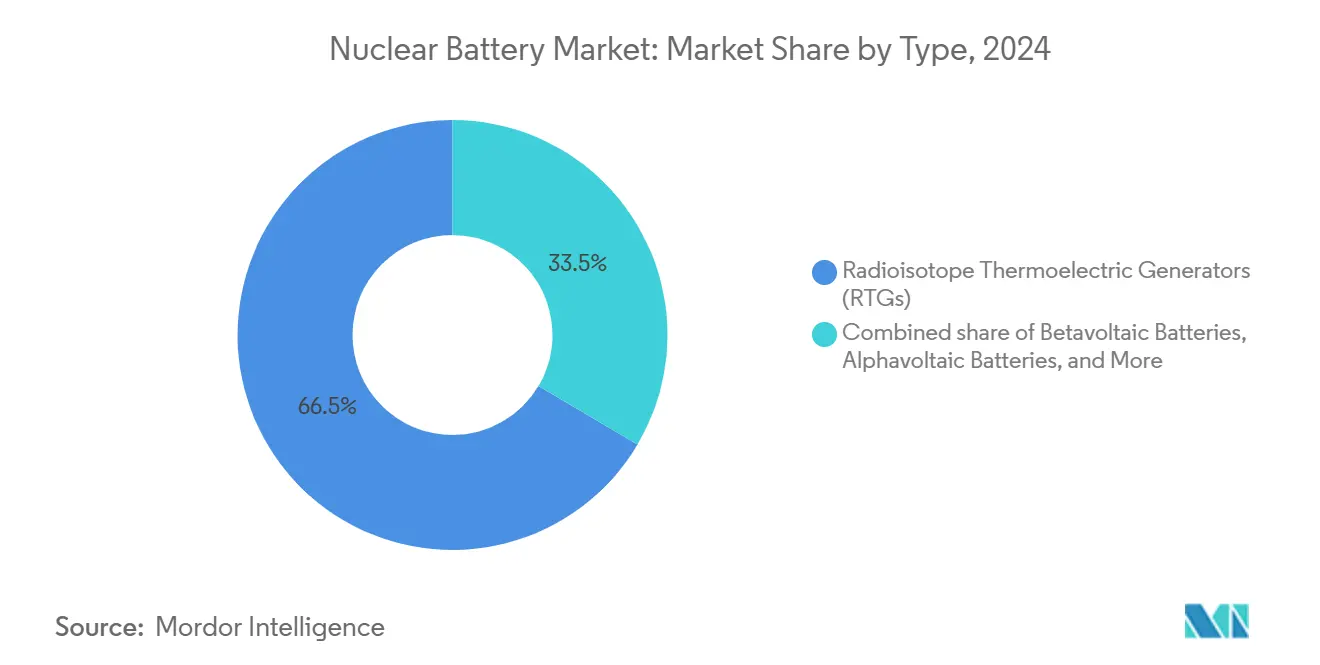

- By type, Radioisotope Thermoelectric Generators commanded 66.5% of the nuclear battery market share in 2024. Betavoltaic batteries are forecast to expand at a 15.8% CAGR through 2030.

- By application, aerospace and spacecraft held 58.9% of the nuclear battery market size in 2024. Medical implants and devices will advance at a 16.5% CAGR between 2025-2030.

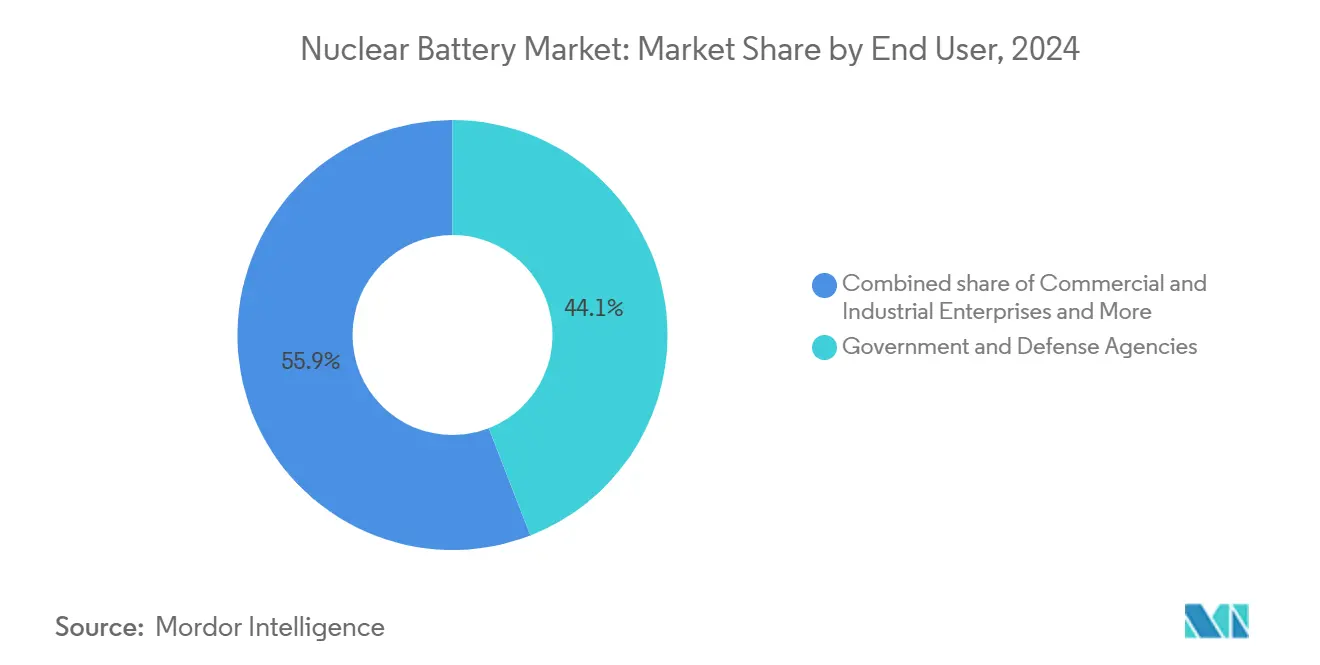

- By end user, government and defense agencies accounted for 44.1% of the nuclear battery market share in 2024, whereas commercial and industrial enterprises will post the fastest 14.2% CAGR.

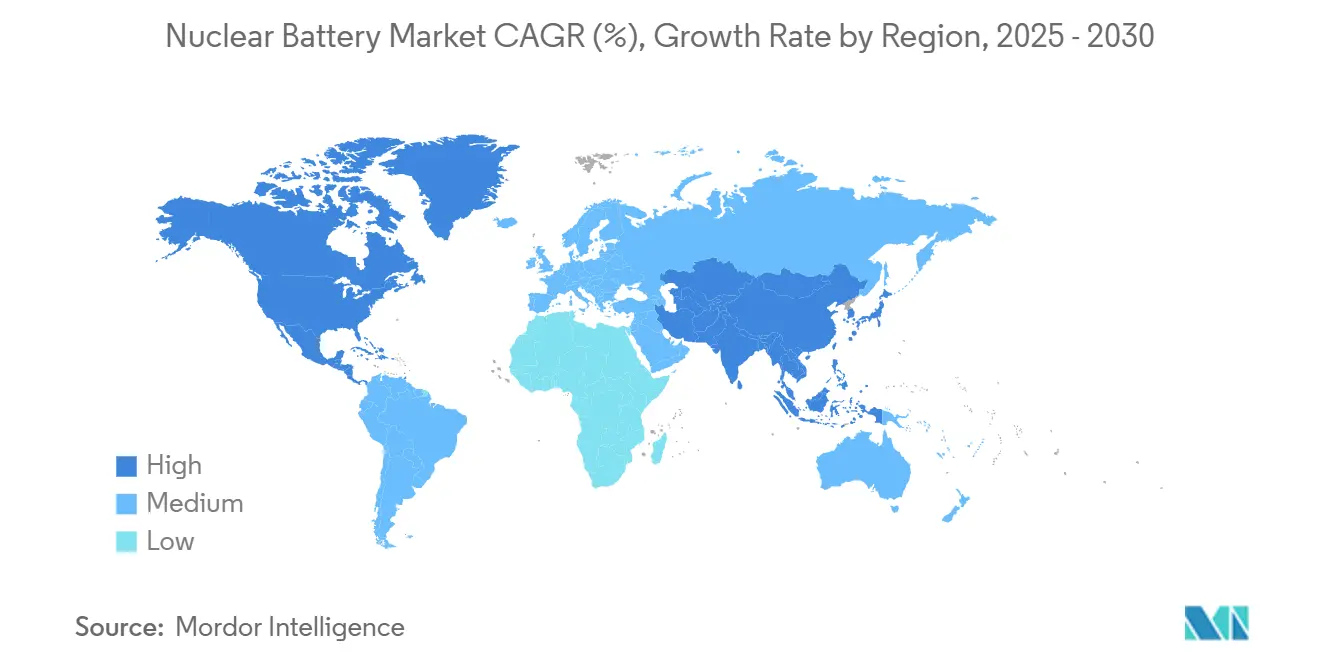

- Regionally, North America led with 43.7% revenue share in 2024, while Asia-Pacific is set to record the highest 13.4% CAGR through 2030.

Global Nuclear Battery Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mainstream RTG demand for deep-space missions | +1.80% | North America & EU, spill-over to APAC | Long term (≥ 4 years) |

| Surge in IoT devices requiring 50-year micro-power | +2.10% | Global, early adoption in North America & APAC | Medium term (2-4 years) |

| Government isotopes-for-space production programs | +1.20% | North America & EU core, limited APAC | Long term (≥ 4 years) |

| Rising defense funding for unattended sensors | +1.40% | North America & EU, selective APAC | Medium term (2-4 years) |

| Breakthrough diamond-semiconductor betavoltaics | +0.90% | Global technology hubs | Short term (≤ 2 years) |

| Radio-waste up-cycling into Am-241 feedstock | +0.70% | EU & North America, emerging APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mainstream RTG demand for deep-space missions

NASA’s Nuclear Power Assessment Study confirms radioisotope power systems as the only proven option for probes under 1 kWe operating far beyond the asteroid belt. Europe is following suit with americium-powered generators for Mars rover programs. Commercial space miners also view RTGs as the only path to autonomous asteroid operations. This deep-space momentum secures a baseline of high-value orders for the nuclear battery market well into the next decade.

Surge in IoT devices requiring 50-year micro-power

Industrial operators are rolling out sensor grids across pipelines, bridges, and refineries that must function for decades without a truck roll. Betavolt’s BV100 delivers 100 µW at 3 V in a 15 mm package and promises a fifty-year service life. When replacement visits exceed USD 10,000 per site, nuclear batteries become the economical choice, creating a volume growth engine for the nuclear battery market.

Government isotopes-for-space production programs

The U.S. Department of Energy added USD 183.9 million to its FY 2025 isotope budget to scale plutonium-238 output.(1)Source: Department of Energy, “FY 2025 Congressional Budget Request,” energy.gov Oak Ridge National Laboratory recently produced 250 g of Pu-238 that meets NASA purity specs, moving toward a 1.5 kg annual target. Europe and China are running parallel initiatives, collectively easing a critical supply constraint and reducing risk premiums in project bids.

Rising defense funding for unattended sensors

Persistent surveillance requirements in contested terrain have fueled U.S. Space Force investments in nuclear-powered payloads. Betavoltaic keys that hold cryptographic material for twenty years without recharge are now entering classified communication suites. These programs translate into steady, budget-protected demand for the nuclear battery market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Isotope supply bottlenecks (Pu-238, Ni-63) | -1.90% | Global, acute in North America & EU | Medium term (2-4 years) |

| High unit-cost vs. Li-ion alternatives | -1.30% | Global, price-sensitive APAC | Short term (≤ 2 years) |

| Public radiological-risk perception | -0.80% | EU & North America | Long term (≥ 4 years) |

| Export-control pinch on beta-device IP | -0.60% | Global, strict U.S.–China corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Isotope supply bottlenecks (Pu-238, Ni-63)

The GAO warns that existing Pu-238 stockpiles cannot support mission manifests beyond 2030 without capacity additions.(2)Source: U.S. Government Accountability Office, “Radioisotope Power Systems Supply,” gao.gov Nickel-63 remains concentrated in one Russian facility, complicating supply chains. Alternative americium-241 harvesting from nuclear waste shows promise, yet regulatory clearance may span years.

High unit-cost vs. Li-ion alternatives

A nuclear cell can cost 10-100 times a comparable lithium-ion pack. While lifecycle economics favor nuclear in remote sites, sticker shock delays adoption in consumer applications. Pilot fabs now seek volume yields to close that gap, but cost pressure remains a near-term drag on the nuclear battery market.

Segment Analysis

By Type: RTGs dominate as betavoltaics accelerate

RTGs held a 66.5% market share of the nuclear battery market in 2024, backed by proven mission reliability. The ongoing Mars and outer-planetary programs rely on Multi-Mission RTGs that have already logged fourteen years of continuous operation. Betavoltaic units, however, are scaling faster; their 15.8% CAGR reflects breakthroughs, such as a 28% diamond-based conversion efficiency, that unlock aircraft, sensor, and consumer use cases. Direct-energy conversion cells occupy a modest niche where instantaneous power delivery offsets lower total output. Alphavoltaic and radiophotovoltaic concepts remain in R&D yet could upset incumbent shares once isotope sourcing hurdles are eased. Therefore, the nuclear battery market will balance RTG stability against betavoltaic momentum through 2030.

Betavoltaic commercialization is shifting perception from exotic lab devices to practical coin-size batteries shipping in thousands of units. Betavolt’s mass-production line marks a watershed, expanding the nuclear battery market size for micro-power cells beyond pilot scale. RTG manufacturers are responding by miniaturizing Stirling convertors and securing long-term isotope contracts. Competitive moats will center on conversion efficiency patents, safety packaging, and end-use certifications rather than raw power output alone, guiding capital flows across the nuclear battery industry.

Note: Segment shares of all individual segments available upon report purchase

By Application: Medical devices surge beyond aerospace

Aerospace and spacecraft claimed 58.9% of the nuclear battery market in 2024, whereas medical devices now post the fastest growth rate of 16.5% CAGR. Cardiac pacemakers and neurostimulators aim for decade-plus lifetimes to reduce revision surgeries, which increase infection risk and associated costs.(3)Source: New England Journal of Medicine, “Pacemaker Replacement Risks,” nejm.org Carbon-14 betavoltaic prototypes meet biocompatibility standards while delivering multi-decade energy.

Industrial IoT nodes form the next demand wave, replacing field battery swaps with micro-power that lasts for decades. Oil-and-gas operators deploy nuclear-powered leak detectors across thousands of miles of pipeline. Unlike solar panels, defense systems add stealth advantages because nuclear cells lack electromagnetic signatures. These use cases diversify revenue streams, shielding the nuclear battery market from fluctuations in aerospace budgets.

By End User: Commercial enterprises widen demand base

Government and defense agencies secured 44.1% of the nuclear battery market share in 2024, primarily due to the use of classified payloads and mission-critical platforms. Nonetheless, commercial and industrial enterprises are expected to post the highest 14.2% CAGR as they retrofit legacy sensor fleets and deploy new autonomous assets.

Venture-backed firms such as Zeno Power are tailoring standardized modules for shipping, mining, and telecom customers. Dual-use procurement policies further blur customer segments, letting commercial volumes amortize R&D funded by defense contracts. Research institutions contribute foundational work on new isotopes and conversion chemistries, ensuring a steady pipeline of intellectual property for the broader nuclear battery industry.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America commanded 43.7% of the nuclear battery market share in 2024, propelled by NASA budgets and a USD 3.46 billion U.S. Navy nuclear command aircraft award. The region benefits from Oak Ridge’s Pu-238 line but faces medium-term supply gaps flagged by GAO. Canada expands its partnerships with Curtiss-Wright on AP-1000 projects, while Mexico explores nuclear sensors for grid modernization.

Asia-Pacific is the fastest-growing territory at a 13.4% CAGR. China targets 70 GW nuclear capacity by 2025 and is commercializing 50-year batteries for drones and smartphones. India, Japan, and South Korea contribute semiconductor know-how that lifts betavoltaic yields. Australia leverages nuclear cells for remote mine monitoring, and ASEAN nations study nuclear options to cut diesel reliance.

Europe holds steady growth, anchored by the EURATOM frameworks that support isotope diversification away from Russian supply. The bloc’s 21.8% share of electricity from nuclear plants creates a natural installed base for battery-powered monitoring. Germany’s waste-to-americium trials indicate regional leadership in radiowaste upcycling. France and the U.K. drive export opportunities through small modular reactor programs that standardize nuclear battery interfaces for safety systems.

Competitive Landscape

The nuclear battery market is infested with heritage aerospace primes and nimble startups. Lockheed Martin and Northrop Grumman deploy decades of RTG domain knowledge and government contracting strength. New entrants such as Betavolt and Zeno Power secure venture rounds exceeding USD 40 million to build automated fabs serving commercial volumes. M&A is rising; Curtiss-Wright paid USD 200 million for Ultra Energy, adding safety-critical monitoring to its portfolio.

Competitive advantage hinges on isotope access and semiconductor IP. Firms with long-term Pu-238 or Ni-63 contracts gain pricing power, while those innovating with americium-based feedstock may bypass chokepoints. Patent filings around diamond and lanthanide coordination polymers have spiked, signaling impending technology segmentation between high-efficiency micro-cells and high-power RTGs.

As the nuclear battery market matures, leaders will differentiate on manufacturing scale, regulatory approvals, and turnkey integration services rather than raw efficiency alone. Partnerships with medical-device OEMs and IoT platform vendors will accelerate adoption beyond government channels, gradually raising market concentration even as fresh capital funds new challengers.

Nuclear Battery Industry Leaders

-

Exide Technologies

-

Lockheed Martin Space

-

City Labs, Inc.

-

NDB Inc.

-

Nusano, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Aalo Atomics raised USD 6.26 million in seed funding led by Fifty Years to commercialize small nuclear fission reactors targeting 3¢ per kWh cost, with participation from Valor Equity Partners and several angel investors to meet global clean energy demands.

- June 2025: Standard Nuclear secured USD 42 million in funding led by Decisive Point to accelerate TRISO nuclear fuel production for advanced reactors at industrial scale, reducing U.S. reliance on foreign nuclear technologies.

- May 2025: Zeno Power completed USD 50 million Series B funding round to expand nuclear battery manufacturing capabilities for maritime and space applications, building on over USD 60 million in U.S. Department of Defense and NASA contracts.

- May 2025: The Nuclear Company raised USD 46 million to develop massive reactor sites, indicating significant investment interest in nuclear technology infrastructure that supports nuclear battery application.

Global Nuclear Battery Market Report Scope

| Radioisotope Thermoelectric Generators (RTGs) |

| Direct Energy-Conversion Batteries |

| Betavoltaic Batteries |

| Alphavoltaic Batteries |

| Others |

| Aerospace and Spacecraft |

| Medical Implants and Devices |

| Remote Monitoring and IoT Sensors |

| Industrial and Oil-and-Gas Asset Integrity |

| Defense and Security Systems |

| Other Applications |

| Government and Defense Agencies |

| Commercial and Industrial Enterprises |

| Research Institutions and Universities |

| Space Agencies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Nordic Countries | |

| Russia | |

| Ukraine | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Radioisotope Thermoelectric Generators (RTGs) | |

| Direct Energy-Conversion Batteries | ||

| Betavoltaic Batteries | ||

| Alphavoltaic Batteries | ||

| Others | ||

| By Application | Aerospace and Spacecraft | |

| Medical Implants and Devices | ||

| Remote Monitoring and IoT Sensors | ||

| Industrial and Oil-and-Gas Asset Integrity | ||

| Defense and Security Systems | ||

| Other Applications | ||

| By End User | Government and Defense Agencies | |

| Commercial and Industrial Enterprises | ||

| Research Institutions and Universities | ||

| Space Agencies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Ukraine | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the nuclear battery market?

The nuclear battery market is valued at USD 82.44 billion for 2025.

How fast will demand grow through 2030?

Revenue is forecast to rise to USD 115.14 billion by 2030, equal to a 6.91% CAGR.

Which application segment is expanding most rapidly?

Medical implants and devices lead with a 16.5% CAGR through the forecast period.

Why are betavoltaic batteries gaining attention now?

Diamond-semiconductor designs have pushed conversion efficiency above 28%, enabling cost-effective micro-power cells for IoT and healthcare.

Which region offers the strongest growth outlook?

Asia-Pacific shows the highest 13.4% CAGR thanks to China’s large-scale commercialization and nuclear capacity build-out.

What is the biggest barrier to wider adoption?

Limited availability of key isotopes such as Pu-238 and Ni-63 constrains manufacturing scale and pricing.

Page last updated on: