Landscaping Tools Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

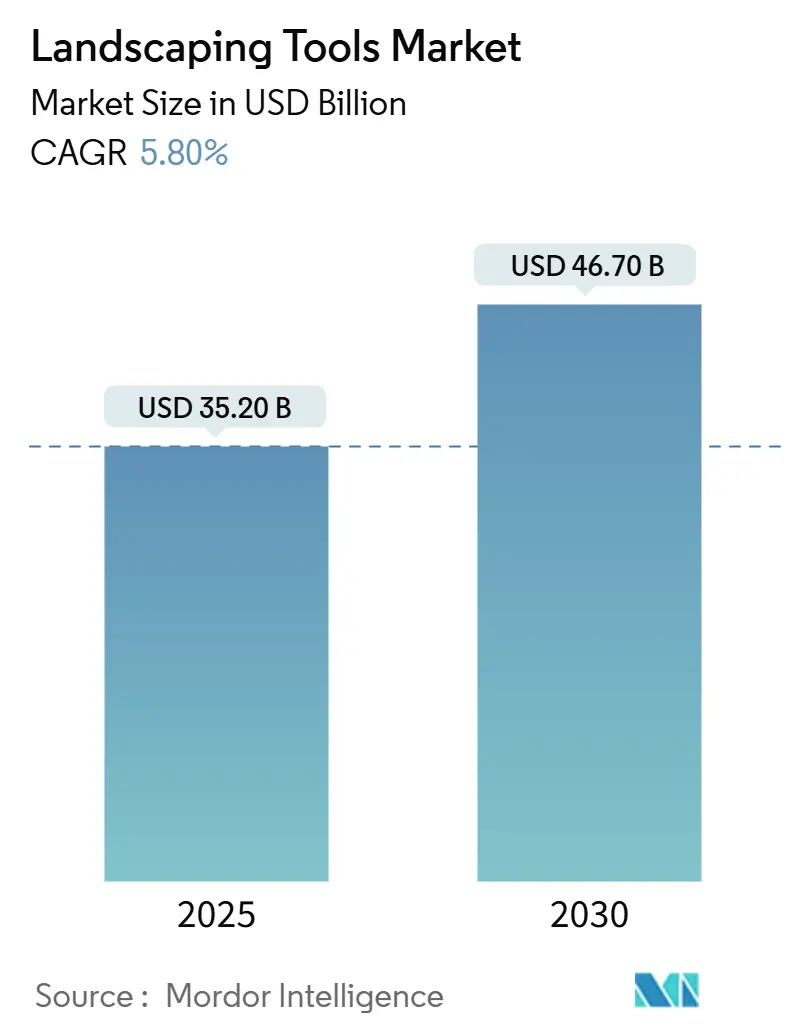

| Market Size (2025) | USD 35.20 Billion |

| Market Size (2030) | USD 46.70 Billion |

| Growth Rate (2025 - 2030) | 5.80% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Landscaping Tools Market Analysis by Mordor Intelligence

The landscaping tools market stands at USD 35.20 billion in 2025 and is forecast to reach USD 46.70 billion by 2030, advancing at a 5.80% CAGR. Rising do-it-yourself lawn care, public-sector carbon-neutral targets, and rapid battery cost declines are reshaping product demand, with North America maintaining its market leadership, while the Asia-Pacific region shows the highest growth rate. Equipment electrification is accelerating as lithium-ion prices fall below USD 100 per kWh, pushing battery-powered models toward cost parity with gasoline units. Municipal rebate schemes in California and similar initiatives in Europe are boosting zero-emission purchases, and robotic mowers are gaining traction as labor shortages constrain contractor capacity[1]Source: California Air Resources Board, “Zero-Emission Landscaping Equipment Incentive Programs,” arb.ca.gov. Competitive intensity remains moderate, the top five companies control half of global revenue, yet category fragmentation still creates entry points for specialists focused on automation and connected-fleet services.

Key Report Takeaways

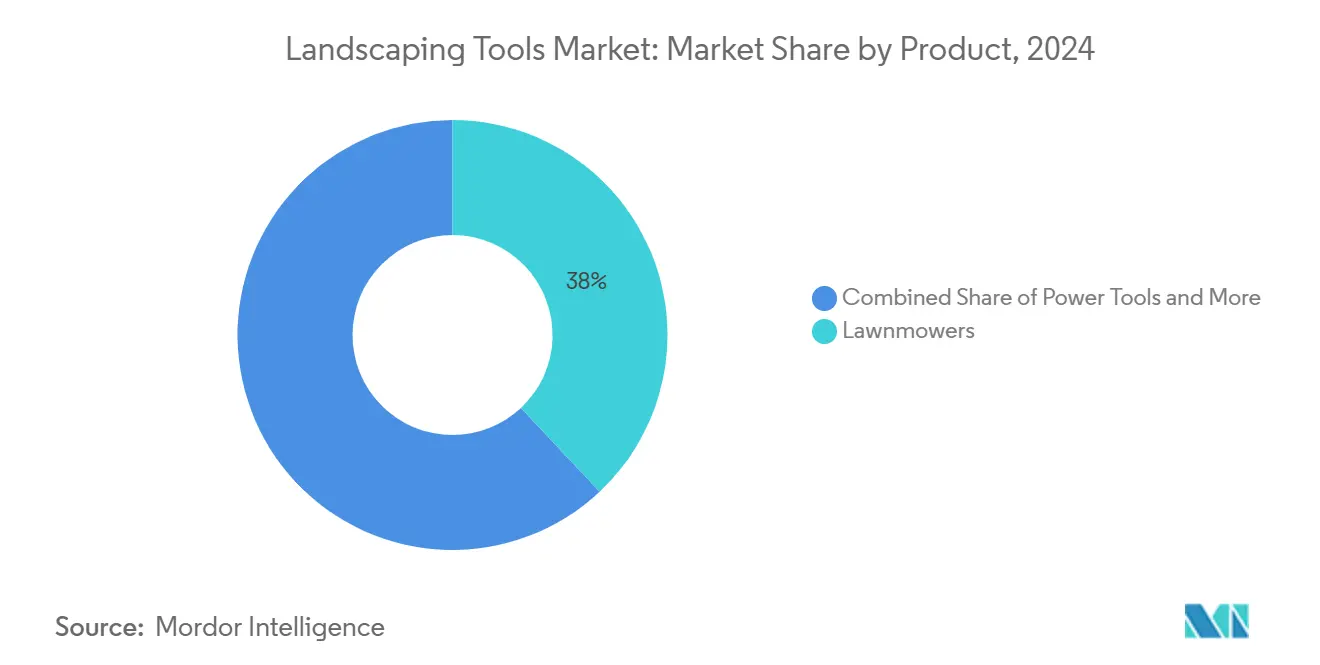

- By product, lawn mowers maintain market dominance with a 38% share in 2024, while Power tools emerge as the fastest-growing category at 9.4% CAGR through 2030.

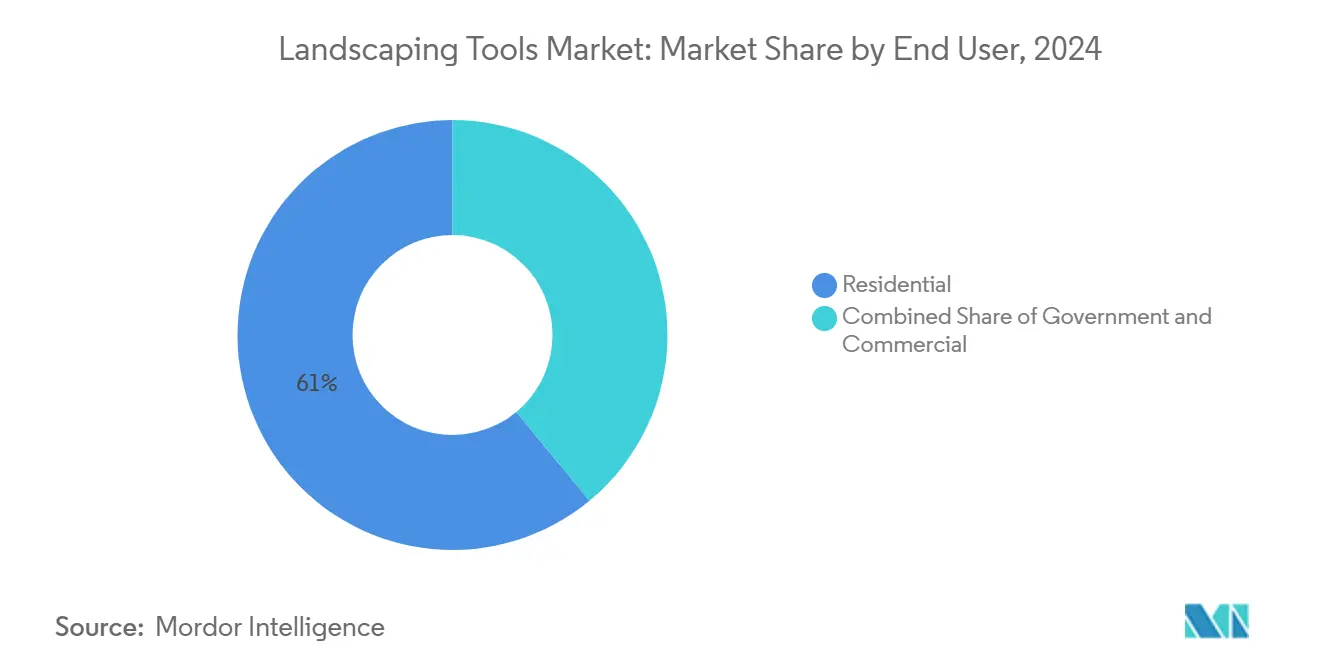

- By end user, residential users account for 61% market size in 2024,while the Government representst the fastest-growing segment at 8.6% CAGR through 2030.

- North America generated 38% of largest market size in 2024, while Asia-Pacific represents the fastest-growing segment at a 7.4% CAGR through 2030.

- The top five manufacturers, Deere and Company, Husqvarna AB, The Toro Company, Stanley Black and Decker Inc., and Robert Bosch GmbH collectively hold the largest share of worldwide revenue, indicating a moderately concentrated competitive environment.

Global Landscaping Tools Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging DIY (Do it Yourself) lawn‐care culture in suburban housing | +1.2% | North America, Western Europe, high-income Asia | Medium term (2-4 years) |

| Rapid urban adoption of green roofs and vertical gardens | +0.8% | Global tier-one metros | Long term (≥ 4 years) |

| Battery pack price declines below USD 100 /kWh | +1.5% | Global | Short term (≤ 2 years) |

| Integration of IoT-enabled fleet management for commercial landscaping | +0.7% | North America, and Europe | Medium term (2-4 years) |

| Municipal carbon-neutral targets boosting electric tool procuremen | +1.0% | North America, Europe, select Asia | Medium term (2-4 years) |

| Landscaping robots bundled with subscription-maintenance services | +0.6% | North America, Europe, premium Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging DIY (Do it Yourself) Lawn‐Care Culture in Suburban Housing

Suburban housing expansion across developed markets is driving unprecedented demand for residential landscaping tools as homeowners increasingly embrace DIY (Do it Yourself) maintenance practices. Work-from-home trends established during 2020-2021 have created sustained engagement with outdoor property improvement, with homeowners investing in professional-grade equipment previously reserved for commercial users. The shift toward DIY (Do it Yourself) culture reflects both cost consciousness and lifestyle preferences, as property owners seek greater control over maintenance schedules and quality standards. Dealers report rising demand for modular power-head systems that accept multiple attachments. Manufacturers able to bundle batteries with cross-platform compatibility gain repeat sales as consumers expand their tool sets.

Rapid Urban Adoption of Green Roofs and Vertical Gardens

Urban sustainability mandates are creating specialized demand for lightweight, precision landscaping tools designed for green infrastructure applications. Green roof installations require equipment capable of operating in weight-constrained environments, typically limiting loads to 80-150 pounds per square foot compared to traditional ground-level applications. This constraint drives demand for compact, battery-powered tools with specialized attachments for irrigation system maintenance, drainage management, and plant care in vertical growing systems. Compact cordless trimmers and irrigation-service attachments now feature quick-swap batteries and compact transport cases that fit standard roof access hatches.

Battery Pack Price Declines Below USD 100 /Kwh

Lithium-ion battery cost reductions are fundamentally altering the total cost of ownership equation between gasoline and electric landscaping equipment. Battery pack prices approaching USD 100 per kilowatt-hour enable electric tools to achieve cost parity with gasoline alternatives over 3-5 year ownership periods, particularly when factoring in reduced maintenance requirements and fuel costs. EGO Power Plus demonstrates this shift with cost analysis showing 5-year savings of EUR 5,068 (USD 5,947.80) for professional users switching from petrol to cordless equipment, driven primarily by the elimination of fuel and servicing costs after the initial year.

Integration of Iot-Enabled Fleet Management for Commercial Landscaping

Commercial landscaping operations are adopting IoT-enabled fleet management systems to address labor shortages and improve operational efficiency through real-time equipment monitoring and route optimization. Contractors deploy telematics modules that report location, run-time hours, and battery state of charge, improving route planning and proof-of-service documentation. Platforms from equipment makers now push over-the-air firmware updates that fine-tune cutting algorithms and extend runtime through optimized blade speed.The integration of IoT capabilities directly into landscaping tools creates opportunities for subscription-based service models and predictive maintenance programs that enhance customer retention and recurring revenue streams.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of trained landscaping labo | −0.8% | North America, and Europe | Short term (≤ 2 years) |

| High upfront cost of commercial-grade cordless tools | −1.2% | Global | Medium term (2-4 years) |

| Grid-edge power limitations in large parks restricting electrification | −0.4% | North America, and Europe | Long term (≥ 4 years) |

| Rising noise-pollution bylaws curbing gas-powered tool usage windows | −0.6% | North America, Europe, select Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Trained Landscaping Labor

The landscaping industry's labor shortages restrict market growth by limiting service capacity and increasing operational costs across equipment categories. In 2024, H-2B visa applications for seasonal workers exceeded the United States cap of 66,000 by nearly 50%. While contractors are increasing automation adoption to address crew shortages, they continue to face challenges in meeting peak-season schedules, which affects equipment turnover. The National Association of Landscape Professionals advocates changing statutory language from "may authorize" to "shall authorize" for presidential H-2B visa approvals to improve workforce planning certainty. This labor constraint simultaneously drives automation adoption while restricting market expansion, as contractors cannot scale operations despite equipment availability.

High Upfront Cost of Commercial-Grade Cordless Tools

Capital cost barriers significantly constrain electric equipment adoption among small contractors and price-sensitive market segments, despite favorable total cost of ownership over multi-year periods. Commercial electric riding mowers range from USD 30,000-40,000 compared to USD 13,000 for equivalent gasoline models, while battery replacement costs add USD 10,000-15,000 every 3-5 years. The IRA commercial clean vehicle tax credit provides partial relief with 30% coverage up to USD 7,500 for qualifying commercial mowers, but this still leaves substantial cost gaps for smaller operators. Financing and leasing programs are emerging as critical adoption enablers, with equipment rental companies like Ashtead Group expanding into landscaping tool categories to provide flexible access models that reduce upfront capital requirements [2]Source: Ashtead Group, “Annual Report 2024,” ashtead-group.com.

Segment Analysis

By Product: Lawnmowers Maintain Leadership While Power Tools Accelerate

Lawnmowers maintain market dominance with a 38% share in 2024, driven by essential lawn maintenance needs across residential and commercial segments. Traditional walk-behind and riding mowers benefit from established distribution networks and proven reliability, and face increasing competition from robotic alternatives that eliminate labor requirements and reduce operational complexity.

Power tools emerge as the fastest-growing category at 9.4% CAGR through 2030, led by battery-powered hedge trimmers, chainsaws, and blowers. Power tools capitalize on electrification trends and regulatory mandates that favor battery-powered alternatives over gasoline engines, with manufacturers like STIHL launching multi-tool systems such as the KMA 120 R that connect to 12 interchangeable implements through quick-coupling mechanisms.

Note: Segment shares of all individual segments available upon report purchase

By End User: Residential Leadership Meets Commercial Growth

Residential users account for 61% market size in 2024, driven by suburban housing expansion, DIY (Do it Yourself) culture adoption, and work-from-home trends that increase property maintenance engagement among homeowners. The residential segment benefits from equipment rental growth, with companies like Ashtead Group expanding into landscaping tool categories to serve occasional-use customers who prefer rental over ownership

Government segments exhibit the highest growth potential at 8.6% CAGR as public sector sustainability commitments drive electric equipment procurement and carbon-neutral operational mandates. Government procurement increasingly specifies environmental criteria and lifecycle cost considerations that favor electric equipment despite higher upfront costs, creating market signals that influence private sector adoption decisions.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America retained 38% of 2024 global revenue. Widespread suburban lawns, mature contractor networks, and state-level zero-emission regulations combine to support sustained demand. Market volatility is tied to H-2B visa allocations that cap seasonal labor, nudging firms toward autonomous platforms. SiteOne Landscape Supply, the region’s largest distributor, posted USD 4.54 billion in 2024 sales after 66 acquisitions, illustrating ongoing consolidation.

Europe holds a significant market share due to stringent sustainability regulations and high disposable incomes. Ireland's 2025 procurement regulations increase the demand for battery-powered equipment in public tenders. European suppliers benefit from their proximity to regional buyers, while the United Kingdom faces import challenges due to post-Brexit trade barriers.

Asia-Pacific is the fastest-growing region at a 7.4% CAGR. Urbanization and rising middle-class incomes underpin residential sales, while local manufacturers scale robotic exports. Chinese producer Ninebot reported RMB 595 million (USD 82 million) in lawn-mower robot revenue for the first nine months of 2024. Japan and South Korea show early adoption of high-precision cordless platforms, whereas India presents upside once infrastructure for battery charging advances.

Competitive Landscape

The landscaping tools market is moderately consolidated with many large, small, and medium-sized manufacturers. The top players in the market include Deere and Company, Husqvarna AB, The Toro Company, Stanley Black and Decker Inc., and Robert Bosch GmbH. Product innovations and acquisitions are the primary strategies followed by these companies to increase their market share and improve their production capabilities using innovative technology.

Market moderately consolidates, reflecting diverse customer needs across residential, commercial, and municipal segments that favor different product attributes, price points, and service models. The competitive landscape increasingly emphasizes electrification capabilities, with companies investing heavily in battery technology, autonomous features, and IoT connectivity to differentiate offerings and capture premium pricing.

Strategic activity centers on electrification and digital integration. Husqvarna partnered with Flex in 2025 to divest a United States factory while securing long-term supply at a lower cost. Deere introduced its first autonomous stand-on mower earlier the same year, positioning itself for high-margin software upgrades. Chinese entrants pressure price points in robotic categories, compelling incumbents to emphasize brand reputation and after-sales service. Distributor consolidation, exemplified by SiteOne’s acquisition roll-up, creates purchasing scale that shifts bargaining power away from smaller suppliers.

Landscaping Tools Industry Leaders

-

Deere and Company

-

Husqvarna AB

-

The Toro Company

-

Stanley Black and Decker Inc.

-

Robert Bosch GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2024: Sunseeker introduced the wire-free robotic lawn mower series Orion X7. Equipped with the AONaviTM Positioning and Navigation System, the Orion X7 seamlessly integrates Real-time Kinematic (RTK) technology with Virtual Simultaneous Localization and Mapping (VSLAM). This combination guarantees centimeter-level precision in positioning, even in intricate settings. The mower is designed to offer the ultimate mowing solution for diverse landscapes, making lawn care a breeze.

- September 2023: John Deere formed a strategic partnership with EGO and its parent company Chevron, which supplies products to the Outdoor Power Equipment (OPE) and Power Tool industries. Through this agreement, John Deere dealers will offer EGO battery-powered lawn care equipment to homeowners.

- May 2023: California Air Resources Board implemented statewide Zero-Emission Landscaping Equipment Incentive Programs across multiple air districts, offering rebates through the Carl Moyer Program with funding up to USD 15,000 for commercial ride-on mower

Global Landscaping Tools Market Report Scope

The landscaping tools such as lawnmowers, power tools, hand tools, and other tools are used to maintain lawns and gardens. The landscaping tools used for industrial and construction purposes are excluded from the study. The Landscaping Tools Market is Segmented by Product (Lawnmowers, Power Tools, Hand Tools, and Other Landscaping Tools), End User (Residential, and Commercial), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The report offers market estimates and forecasts in Value (USD) for all the above segments.

| Lawnmowers |

| Power Tools |

| Hand Tools |

| Other Landscaping Tools |

| Residential |

| Commercial |

| Government |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product | Lawnmowers | |

| Power Tools | ||

| Hand Tools | ||

| Other Landscaping Tools | ||

| By End User | Residential | |

| Commercial | ||

| Government | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is global spending on landscaping tools in 2025?

The market totals USD 35.20 billion in 2025 and is projected to reach USD 46.70 billion by 2030.

Which product category generates the most revenue?

Lawnmowers lead with 38% of global sales in 2024, although power tools are growing fastest.

What region is expanding the quickest?

Asia-Pacific posts the highest growth at a 7.4% CAGR driven by urbanization and green infrastructure projects.

Who are the top five players hold largest shares in this market?

Asia-Pacific posts the highest growth at a 7.4% CAGR driven by urbanization and green infrastructure projects.

Page last updated on: