Convenience Store Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

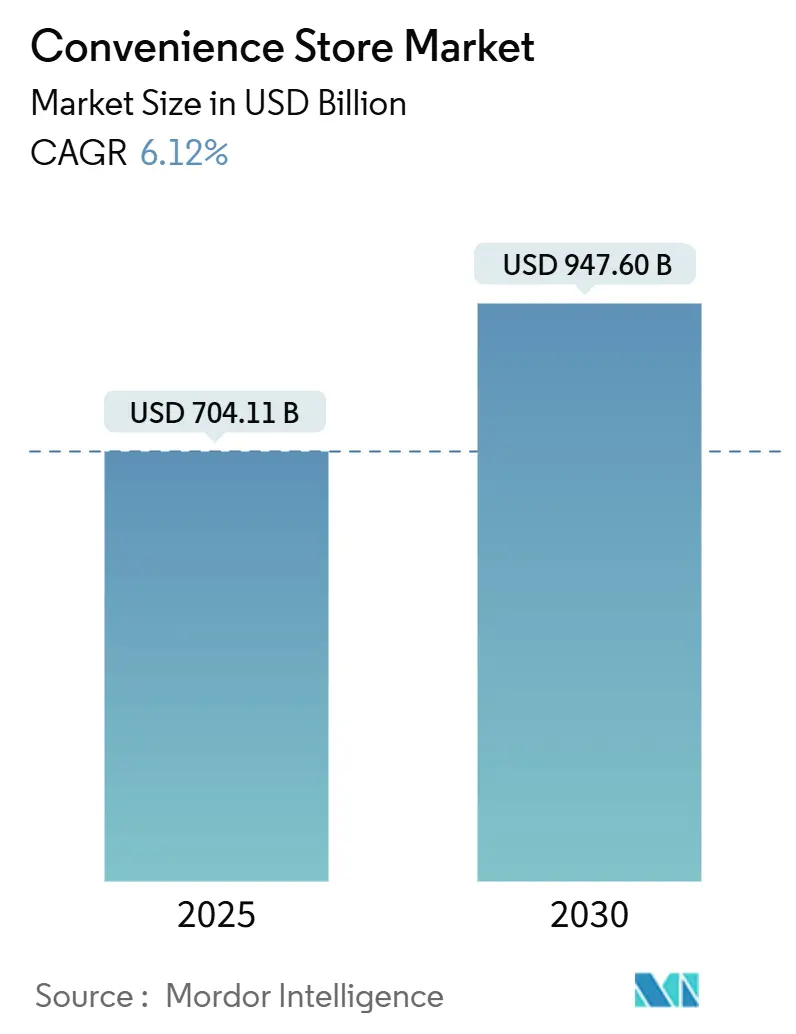

| Market Size (2025) | USD 704.11 Billion |

| Market Size (2030) | USD 947.60 Billion |

| Growth Rate (2025 - 2030) | 6.12% CAGR |

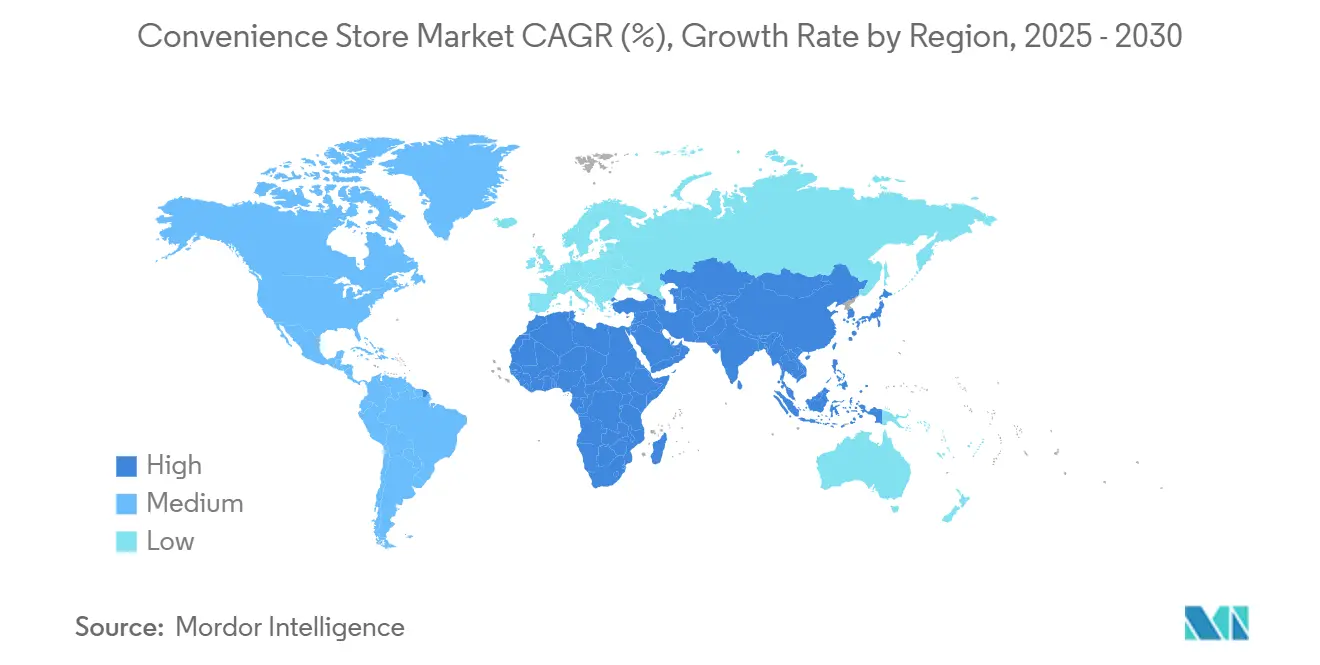

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

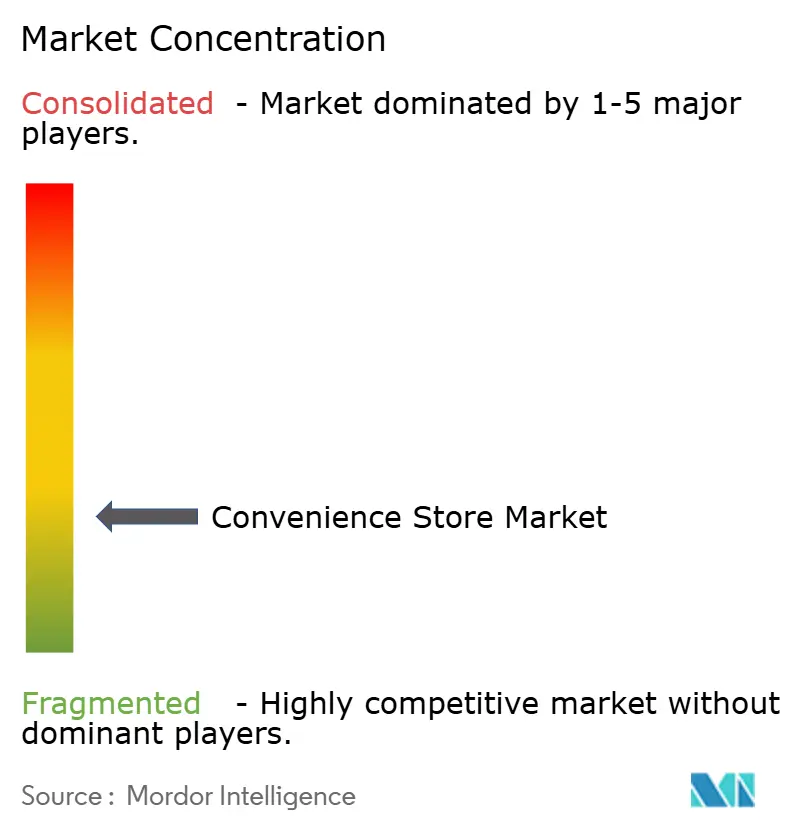

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Convenience Store Market Analysis by Mordor Intelligence

The convenience store market size reached USD 704.11 billion in 2025 and is forecast to expand at a 6.12% CAGR to USD 947.61 billion by 2030. Momentum comes from urban migration, rising demand for instant‐gratification shopping, and the digital integration of ordering, loyalty, and payment tools across formats. Operators are enlarging prepared-food menus, embedding electric-vehicle charging, and applying real-time analytics to shorten replenishment cycles, all of which lift basket value even when fuel volumes soften. Private-equity roll-ups and corporate M&A remain active because the sector delivers predictable cash flows and resilient customer footfall, while regulatory incentives for alternative-energy infrastructure open fresh revenue streams. The competitive intensity within the market remains moderate, as the top chains account for only a limited portion of global revenue. This scenario creates opportunities for mid-tier and regional players to establish a competitive edge by focusing on localization strategies, expanding their product portfolios, and leveraging data-driven promotional activities to attract and retain customers.

Key Report Takeaways

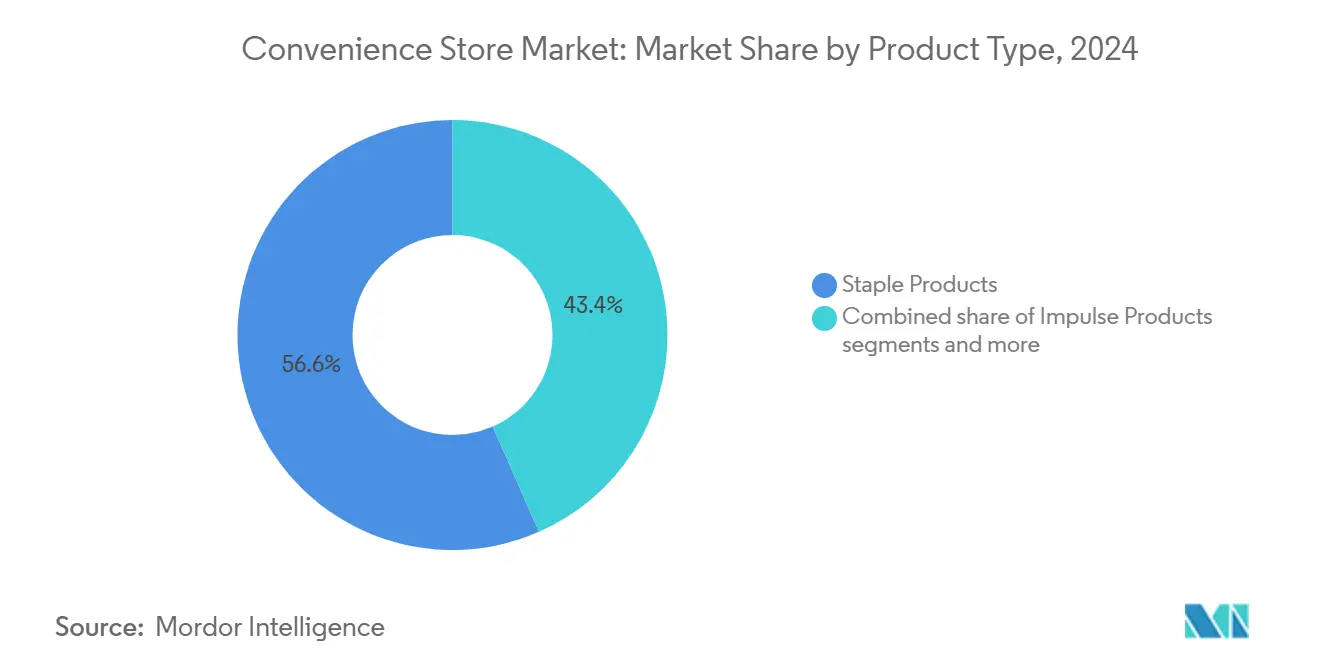

- By product category, staple products led with 56.64% of the convenience store market share in 2024; emergency products are projected to rise at a 9.72% CAGR to 2030.

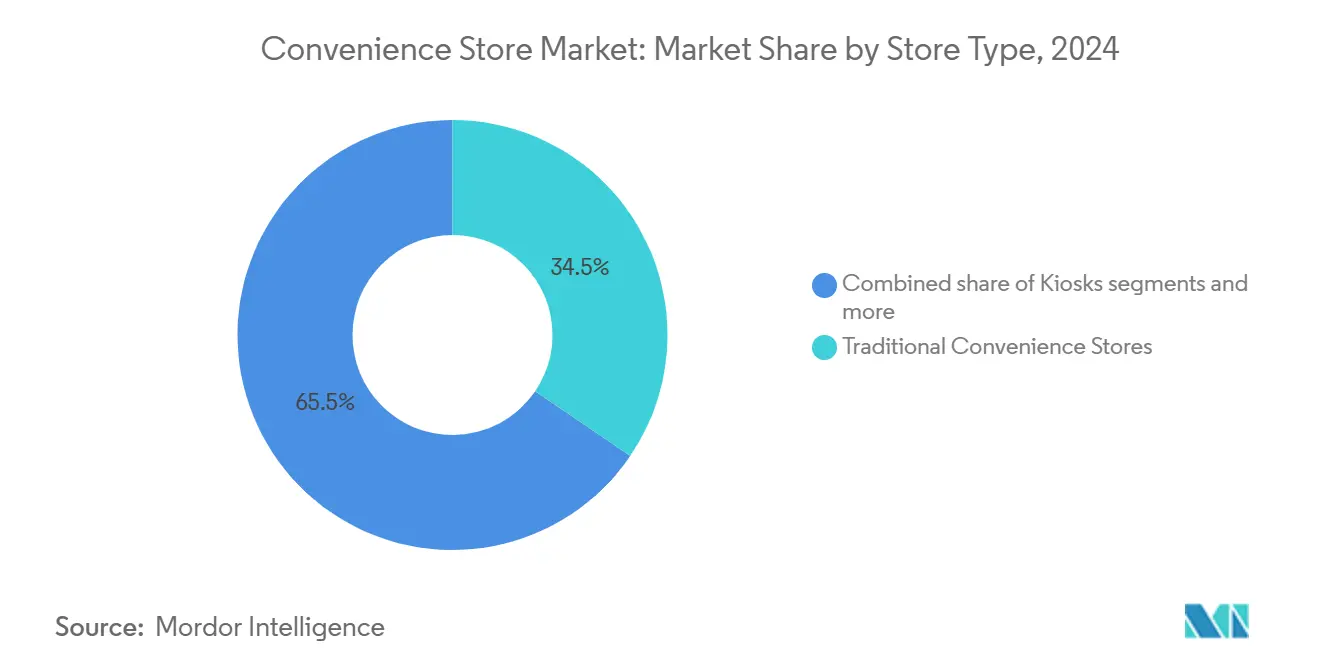

- By store type, traditional convenience stores held 34.48% revenue share of the convenience store market in 2024, while hyper convenience stores are advancing at a 10.83% CAGR through 2030.

- By ownership model, corporate-owned chains accounted for 47.48% of the convenience store market size in 2024; franchise stores are poised to grow at a 9.87% CAGR over the forecast period.

- By geography, North America commanded 38.47% of the 2024 revenue of the convenience store market, whereas Asia-Pacific is expected to post the fastest regional CAGR of 8.38% to 2030.

Global Convenience Store Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban Micro-Fulfilment Demand Spike | +1.2% | Global, concentrated in dense urban areas | Medium term (2-4 years) |

| Cash-Rich Private-Equity Roll-Ups | +0.8% | North America & Europe primarily | Short term (≤ 2 years) |

| Digital Lottery & Gaming Commissions | +0.6% | North America, expanding to APAC | Medium term (2-4 years) |

| EV-Charger Foot-Traffic Boost | +1.1% | North America & EU leading, APAC following | Long term (≥ 4 years) |

| Subscription-Based Meal-Kits Pick-Up | +0.4% | Urban North America & Europe | Medium term (2-4 years) |

| Real-Time Planogram Analytics | +0.7% | Global, technology-advanced markets first | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Urban Micro-Fulfilment Demand Spike

Dense city cores increasingly rely on convenience stores as last-mile hubs for two-hour and same-day delivery services, allowing operators to serve both walk-in and digital orders from the same shelf location. In 2024, Casey's completed the acquisition of a Star Food Store located in Texas, strategically enhancing its presence in delivery-friendly zones. This acquisition is expected to generate incremental revenue while maintaining minimal growth in fixed costs, reflecting a calculated approach to operational expansion and resource optimization. Wawa’s 70-store Southeast expansion follows a similar logic, ensuring enough nodes to guarantee 15-minute delivery windows. Real-time planogram tools feed demand signals directly to distribution centres, keeping high-velocity SKUs in stock and trimming spoilage. Municipal zoning rules increasingly reserve curb-space permits for companies that maintain brick-and-mortar sites, tilting competitive advantage toward established convenience brands.

Cash-Rich Private-Equity Roll-Ups

First Reserve has explored a USD 1.5 billion sale of Refuel, underscoring how financial sponsors view the category as defensive, cash-generative, and exit-ready[1]Greg Lindenberg, “Casey’s Exceeds $1 Billion in EBITDA for First Time in C-Store Chain’s History,” CSP Daily News, cspdailynews.com . Arko Corp.’s decision to divest its company-operated stores, valued at USD 2 billion, reflects significant opportunities for both strategic acquirers and private equity sponsors. Casey’s recent acquisition of CEFCO sites demonstrates how corporations strategically utilize debt financing to compete with private capital, achieving operational efficiencies in areas such as fuel procurement and prepared-food logistics. These developments collectively drive the professionalization of operations, enhance data standardization, and improve access to capital within the convenience store market, fostering a more competitive and streamlined industry landscape.

Digital Lottery & Gaming Commissions

Online lottery approvals in Massachusetts and self-service terminal rollouts in Canada have added high-margin fee income that requires little additional labour. Digital channels significantly enhance the accessibility and distribution of ticket sales, enabling broader audience engagement. Meanwhile, physical stores serve as strategic touchpoints by facilitating prize-redemption activities, which, in turn, drive incremental revenue through increased ancillary sales. Age-verification modules integrate with existing POS hardware, a barrier for independent bodegas but a straightforward upgrade for chain operators. As U.S. states seek new tax revenue, more jurisdictions are expected to authorize digital lottery, sustaining this driver into the medium term.

EV-Charger Foot-Traffic Boost

Pilot Company, which operates a network of over 130 fast-charging stations, has reported significant growth in both customer traffic and revenue. This expansion highlights the increasing demand for electric vehicle (EV) infrastructure and its positive impact on business performance[2]Consumer Reports Staff, “Where to Charge Your Electric Car,” Consumer Reports, consumerreports.org . A considerable proportion of electric vehicle (EV) drivers make purchases of food or beverages during their charging sessions, which typically last several minutes. This behavior results in higher transaction values compared to visits by gasoline vehicle users. Federal tax incentives currently subsidize up to a significant portion of the installation expenses for direct-current fast chargers, thereby improving the return on investment for businesses adopting this technology. Additionally, early adopters gain a competitive advantage through locational exclusivity, as regulatory frameworks increasingly require the integration of EV infrastructure in new property developments.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Urban Lease Renewals | -1.4% | Global urban centres, particularly in North America | Short term (≤ 2 years) |

| Stricter HFSS Product Limits | -0.9% | Europe leading, expanding globally | Medium term (2-4 years) |

| Labour Shortage & Minimum-Wage Escalation | -1.1% | Developed markets globally | Short term (≤ 2 years) |

| Cyber-Security Liability for Self-Checkout | -0.6% | Technology-advanced markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Urban Lease Renewals

In the fourth quarter of 2024, the average rental rate for shopping centres in the United States reached USD 24.76 per square foot, reflecting the ongoing demand for retail spaces and the resilience of the commercial real estate market CBRE.COM. Cap-rate compression continues to sustain elevated property valuations, which, in turn, drive significant increases in renewal rates. This trend emerges at a time when macroeconomic challenges are exerting pressure on discretionary consumer spending. 7-Eleven shuttered 400 under-performing North American sites in late 2024, chiefly in rent-intensive metros, to recycle capital into high-return formats. Zoning laws often block relocation to cheaper districts without fuel-tank re-permitting, locking operators into escalators that compress margins.

Labour Shortage & Minimum-Wage Escalation

Casey’s trimmed labour hours for seven straight quarters, yet still faced a slight jump in same-store employee expense in fiscal 2024. Overnight shifts remain hardest to staff due to safety concerns and sparse transit options. Murphy USA has reported an increase in operating expenses, primarily driven by higher wages and maintenance costs. This trend is largely attributed to jurisdictions implementing minimum wage hikes at a rate that surpasses productivity improvements, thereby exerting upward pressure on store-level operating expenditures. Self-checkout, AI inventory, and automated fuel dispensers mitigate but do not fully offset the upward pressure, particularly for independents lacking scale to amortize technology.

Segment Analysis

By Product Type: Emergency Products Drive Premium Growth

Staple products controlled 56.64% of 2024 revenue within the convenience store market share, underscoring consumer dependence on beverages, snacks, and daily necessities. Emergency products, although smaller in absolute terms, are slated to expand at a 9.72% CAGR, capitalizing on weather disruptions and supply shocks that redirect shoppers from supermarkets to nearby stores. The COVID-19 crisis proved the format’s resilience as a quasi-public-service node when larger outlets faced curfews. Prepared foods sharpen differentiation: Casey’s lifted prepared-food and dispensed-beverage revenue 11.4% year-over-year to USD 349 million in Q3 2024, illustrating margin accretion from hot food lines[3]Melissa Kress, “Casey’s Turns in Solid Q3 2024 Boosted by Inside Sales,” Convenience Store News, csnews.com . Impulse products sit between the two, fuelled by strategic end-cap placement and promotional bundling that exploit immediate-consumption psychology.

Shoppers increasingly expect crisis-responsive assortments, portable chargers, bottled water, and OTC medication, driving SKU rationalization around high-turn, high-margin emergency items. Operators rely on real-time demand sensing to pre-stage these goods ahead of hurricanes or heat waves, protecting against stockouts and reinforcing brand trust. As climate volatility intensifies, emergency products could capture a larger slice of the convenience store market, especially in regions prone to extreme weather.

Note: Segment shares of all individual segments available upon report purchase

By Store Type: Hyper Convenience Stores Reshape Format Expectations

In 2024, traditional box formats contributed 34.48% to the overall turnover, maintaining their role as a legacy model that integrates fuel pumps with retail sales areas. On the other hand, hyper-convenience stores are transforming the operational and economic dynamics of the market. These stores leverage compact square-foot layouts to incorporate features such as barista bars, fresh kitchens, and expanded grocery aisles, which are driving a strong CAGR of 10.83% through 2030. The scalability of this format is exemplified by QuikTrip's truck-stop hybrids in Ohio and Nevada, which combine Class-8 diesel lanes with additional amenities, including sit-down dining options and shower facilities, catering to a diverse customer base and enhancing overall value propositions.

Limited-selection and mini convenience sites persist where zoning caps square footage or foot-traffic density rewards micro-formats, such as transit hubs. Kiosks remain viable in subway corridors and campus quads by focusing on speed and single-serve SKUs. Expanded convenience stores bridge the gap, enlarging cooler space and adding basic produce to attract fill-in shoppers. Diversified footprints let chains tailor capex to local demographics, sustaining relevance across urban, suburban, and rural grids within the convenience store market.

Note: Segment shares of all individual segments available upon report purchase

By Ownership Model: Franchise Growth Accelerates Market Penetration

Corporate ownership governed 47.48% of the 2024 convenience store market size, reflecting balance-sheet capacity and centralized decision-making advantages. Franchise stores, growing at 9.87% CAGR, offer asset-light expansion for brands while granting entrepreneurs proven playbooks, bulk purchasing, and tech platforms. Casey’s blend of acquisitions and franchising, adding 228 Fikes sites in Q3 2025, highlights a hybrid growth path that lifts systemwide sales without over-leveraging the parent.

Independents still anchor rural communities, often where large chains avoid low-volume routes. Yet they face capital hurdles for EV charging, data security, and wage regulation. Lending programs that preferentially back small businesses sustain the cohort, but consolidation momentum remains, evidenced by Nouria’s 2024 purchase of Enmarket’s 132 stores. Over time, franchise and corporate models are expected to absorb a larger slice of the convenience store market share, tightening procurement efficiencies and technology deployment.

Geography Analysis

In 2024, North America contributed 38.47% to the total turnover, primarily driven by well-established fuel integration strategies and a high prevalence of household car ownership. During Q3 2025, U.S.-based chains such as Casey’s reported robust fuel margins while strategically increasing the proportion of inside sales attributed to high-margin prepared food offerings. Concurrently, Canada emerged as a leader in sustainability initiatives, exemplified by 7-Eleven Canada’s 2023 collaboration with a food-waste app, which successfully prevented 130,000 meals from being wasted. This initiative also laid the groundwork for similar implementations in the U.S. market. On the consolidation front, Alimentation Couche-Tard’s USD 47.2 billion acquisition bid for Seven & i is anticipated to necessitate the divestiture of certain stores to comply with regulatory requirements, a move that could significantly alter the competitive dynamics within the region.

Asia-Pacific is poised for the highest growth at an 8.38% CAGR, led by compressed living spaces and rising disposable income that favour quick trips. Lawson plans to double overseas units to 14,000, and FamilyMart is reorganizing its China network while entering the U.S., underscoring cross-border ambitions. Japanese pioneers focus on proprietary hot foods and cashier-less tech; South Korea’s GS25 drives loyalty via super-app ecosystems that integrate payments, delivery, and media. The Middle East remains nascent yet promising: Saudi Arabia’s AL Sulaiman Group will ramp Circle K from 40 to 300 sites within five years, targeting hospitals, universities, and offices.

Europe presents maturity tempered by regulatory rigor. HFSS product caps push chains to reformulate snack lines and market better-for-you ranges, supplying a template later exported worldwide. Switzerland’s Coop Pronto optimizes small-box assortments and energy-efficient refrigeration to meet both profitability and environmental goals. Latin America, particularly Brazil’s 8,100-store network with 60% franchise penetration, showcases rising middle-class demand and provides strategic adjacency for North American majors expanding southward.

Competitive Landscape

Moderate fragmentation defines the convenience store industry, with seven-and-a-half U.S. chains covering just one-quarter of stores, leaving ample room for consolidators. 7-Eleven commands 8.2% of outlets, with Circle K trailing at roughly 5,833 locations. Technology adoption separates leaders from laggards: 7-Eleven’s retail-media network leverages loyalty data to sell targeted promotions, while Casey’s applies AI inventory models that cut stockouts and spoilage. Foodservice pivot remains key; 7-Eleven now books food as its largest U.S. category, overtaking cigarettes amid declining tobacco volumes.

White-space expansion targets rural underserved areas and urban deserts where full-line grocers exited. EV-charging integration also acts as a moat: Pilot’s coast-to-coast fast chargers attract higher-income motorists who convert to premium coffee or prepared-meal purchases. Quick-commerce platforms like DoorDash create symbiosis rather than competition by using convenience stores as dark-store nodes for 15-minute grocery delivery, importing incremental sales with no extra real estate.

Private capital accelerates change. Nouria’s Southeast move and Couche-Tard’s mega-bid spotlight the sector’s appeal amid inflation and volatile fuel demand. Cybersecurity remains an Achilles’ heel; a January 2025 payment-card breach at Gas Express, Circle K’s largest U.S. franchisee, triggered a chain-wide POS hardening initiative. Chains that master both digital resilience and operational efficiency will widen the performance gap as compliance costs rise.

Convenience Store Industry Leaders

-

7-Eleven (Seven & i Holdings)

-

Alimentation Couche-Tard (Circle K)

-

FamilyMart

-

Lawson

-

GS25 (GS Retail)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Alimentation Couche-Tard raised its offer for Seven & i to USD 47.2 billion, with CDPQ signaling financing support.

- October 2024: Nouria agreed to buy Enmarket’s 132 stores, extending its reach into the U.S. Southeast.

- August 2024: FEMSA’s OXXO brand bought Delek’s 249 U.S. stores for USD 385 million, marking its American debut.

- April 2024: Saudi Arabia’s Alsulaiman Group unveiled plans to scale Circle K from 40 to 300 GCC sites within five years.

Global Convenience Store Market Report Scope

A convenience store is a retail shop that makes available essential goods consisting of groceries like eggs, bread, butter, and milk, over-the-counter medicines, soft drinks, etc., with a few convenience stores selling limited alcohol products.

The convenience store market is segmented by product types, store types, and region. By product types, the market is sub-segmented into staple products, impulse products, and emergency products. By store types, the market is sub-segmented into kiosks, mini convenience stores, limited selection convenience stores, traditional convenience stores, expanded convenience stores, and hyper convenience stores. By region, the market is sub-segmented into North America, Latin America, Europe, the Middle East and Africa, and Asia Pacific.

The report offers market size and forecasts for the convenience store market in value (USD) for all the above segments.

| Staple Products |

| Impulse Products |

| Emergency Products |

| Kiosks |

| Mini Convenience Stores |

| Limited Selection Convenience Stores |

| Traditional Convenience Stores |

| Expanded Convenience Stores |

| Hyper Convenience Stores |

| Independent Stores |

| Franchise Stores |

| Corporate-Owned Chains |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX | Belgium | |

| Netherlands | ||

| Luxembourg | ||

| NORDICS | Denmark | |

| Finland | ||

| Iceland | ||

| Norway | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| South-East Asia | Singapore | |

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Philippines | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

| By Product Type | Staple Products | ||

| Impulse Products | |||

| Emergency Products | |||

| By Store Type | Kiosks | ||

| Mini Convenience Stores | |||

| Limited Selection Convenience Stores | |||

| Traditional Convenience Stores | |||

| Expanded Convenience Stores | |||

| Hyper Convenience Stores | |||

| By Ownership Model | Independent Stores | ||

| Franchise Stores | |||

| Corporate-Owned Chains | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Peru | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Spain | |||

| Italy | |||

| BENELUX | Belgium | ||

| Netherlands | |||

| Luxembourg | |||

| NORDICS | Denmark | ||

| Finland | |||

| Iceland | |||

| Norway | |||

| Sweden | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| South-East Asia | Singapore | ||

| Malaysia | |||

| Thailand | |||

| Indonesia | |||

| Vietnam | |||

| Philippines | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Saudi Arabia | ||

| United Arab Emirates | |||

| South Africa | |||

| Nigeria | |||

| Rest of Middle East and Africa | |||

Key Questions Answered in the Report

How large is the convenience store market in 2025?

The convenience store market size stands at USD 704.11 billion in 2025, expanding toward USD 947.61 billion by 2030 under a 6.12% CAGR.

Which product category grows fastest within convenience stores?

Emergency products show the highest momentum, projected to rise at a 9.72% CAGR through 2030 as shoppers seek crisis-ready items.

Why are hyper convenience stores gaining popularity?

Larger footprints support foodservice, wider grocery assortments, and EV charging, helping hyper formats post a 10.83% CAGR and outpace traditional boxes.

What region offers the strongest growth prospects?

Asia-Pacific leads regional expansion with an expected 8.38% CAGR, thanks to urbanization and rising disposable incomes.

How does EV charging benefit store revenue?

Stores equipped with fast charger’s report about 4% higher foot traffic and 5% higher sales because 89% of EV drivers make in-store purchases while waiting.

What is driving M&A activity in the sector?

Predictable cash flows, fragmented ownership, and synergies in fuel procurement and data analytics attract private-equity and corporate buyers alike.

Page last updated on: