Geothermal Drill Bits Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

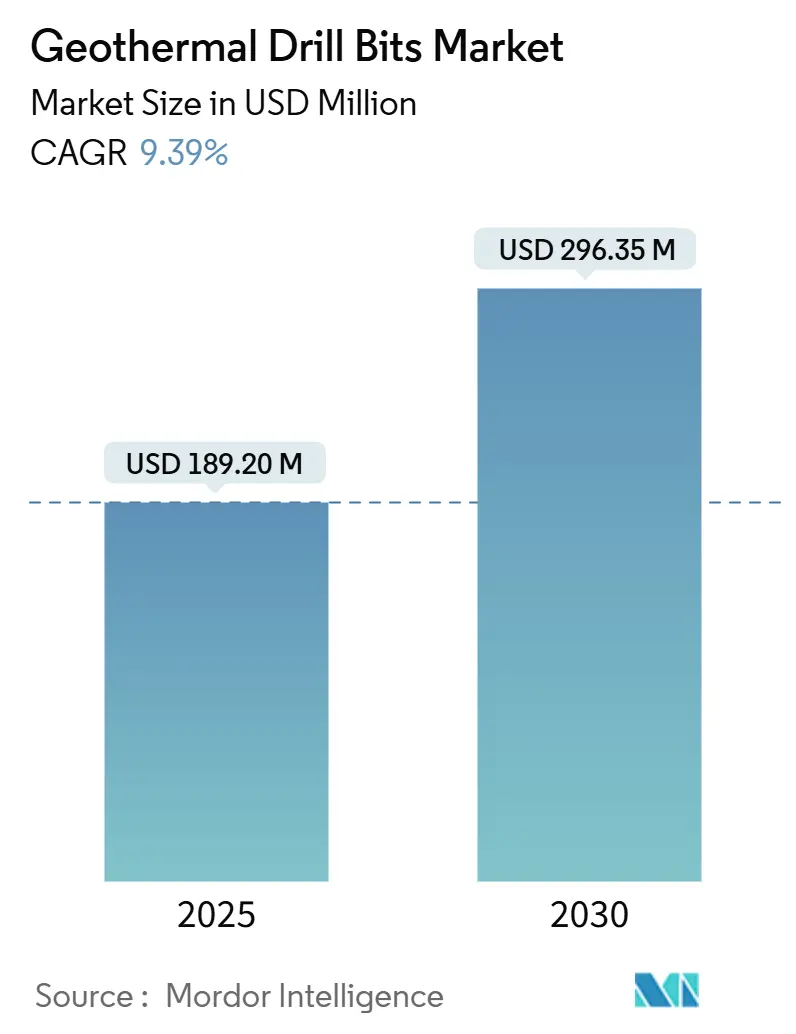

| Market Size (2025) | USD 189.20 Million |

| Market Size (2030) | USD 296.35 Million |

| Growth Rate (2025 - 2030) | 9.39% CAGR |

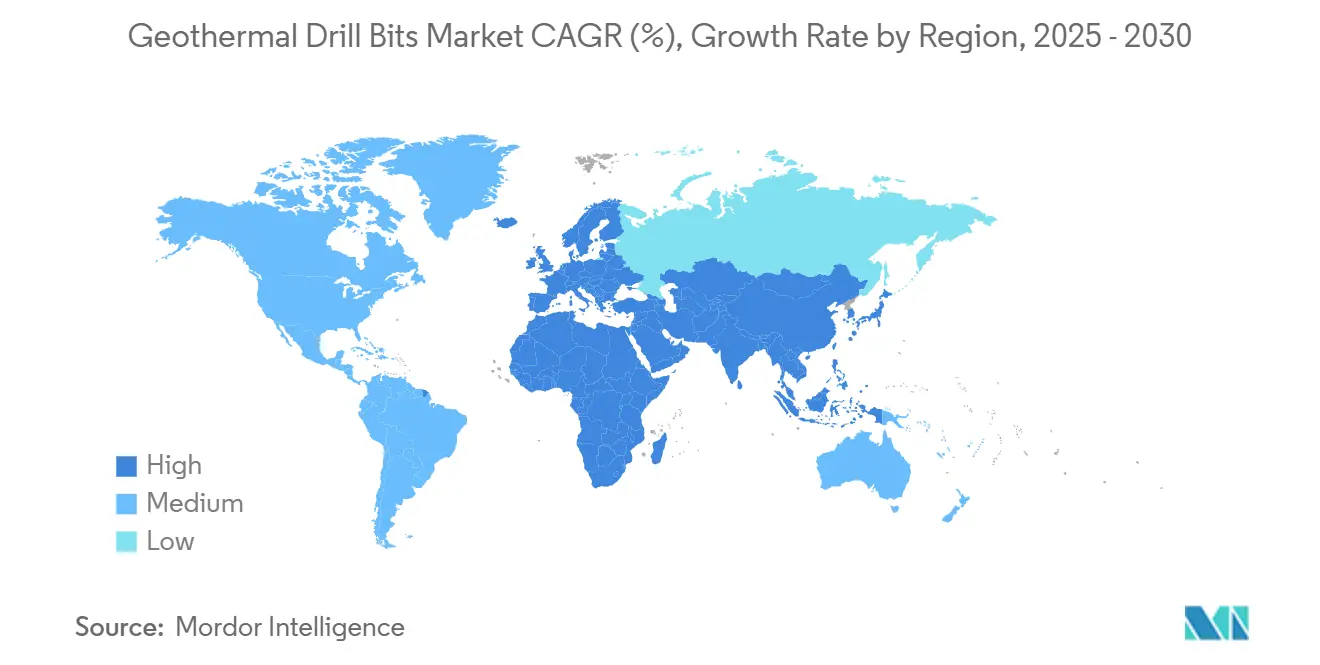

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Geothermal Drill Bits Market Analysis by Mordor Intelligence

The Geothermal Drill Bits Market size is estimated at USD 189.20 million in 2025, and is expected to reach USD 296.35 million by 2030, at a CAGR of 9.39% during the forecast period (2025-2030).

This trajectory reflects intensifying efforts to decarbonize baseload electricity, where reliable geothermal power depends on cost-effective subsurface access. The widespread adoption of high-performance polycrystalline diamond compact (PDC) and hybrid bits, combined with sharper policy incentives and technology transfers from oil and gas drilling, collectively underpin a 56.6% cumulative expansion in the geothermal drill bits market. The onshore segment still accounts for more than three-quarters of total demand; yet, offshore initiatives, particularly on shallow continental shelves, are accelerating on the back of marine-drilling expertise. Meanwhile, supply-chain constraints in tungsten carbide and synthetic diamonds present short-term headwinds, but breakthroughs in high-temperature elastomers and advanced cutter designs continue to widen long-term growth opportunities in the geothermal drill bits market.

Key Report Takeaways

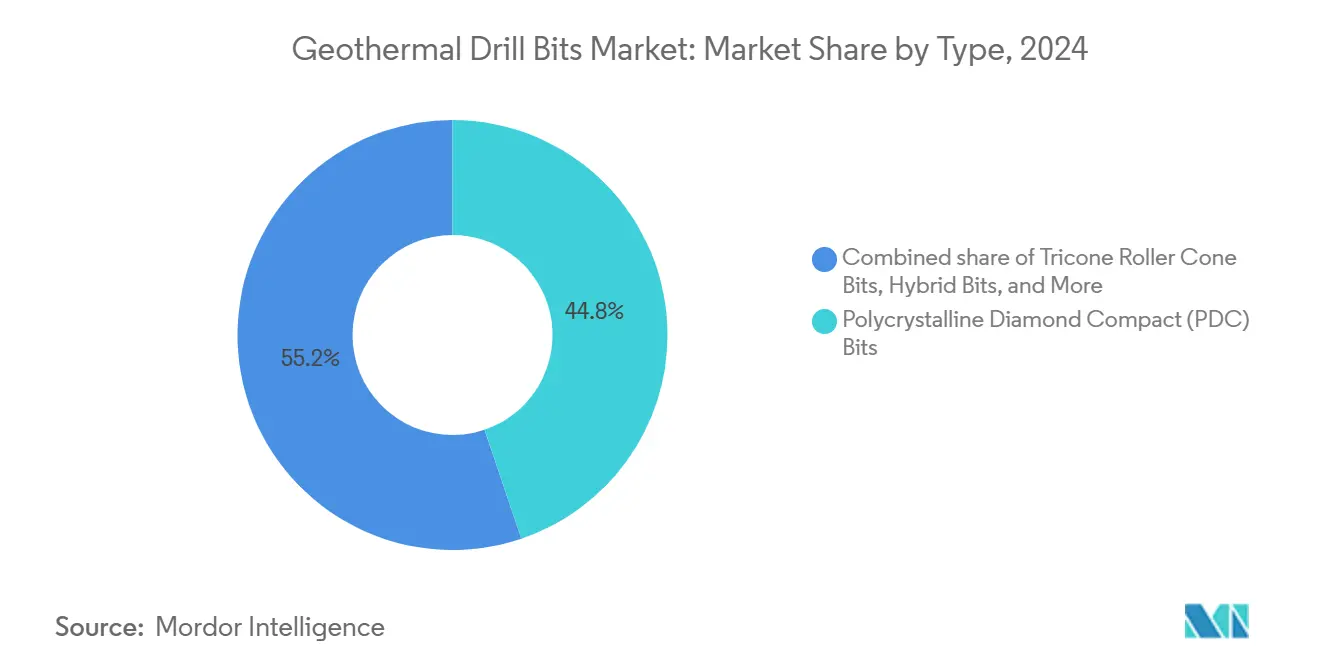

- By type, PDC bits held 44.8% of the geothermal drill bits market share in 2024, while tricone roller cone bits recorded the quickest 13.6% CAGR through 2030.

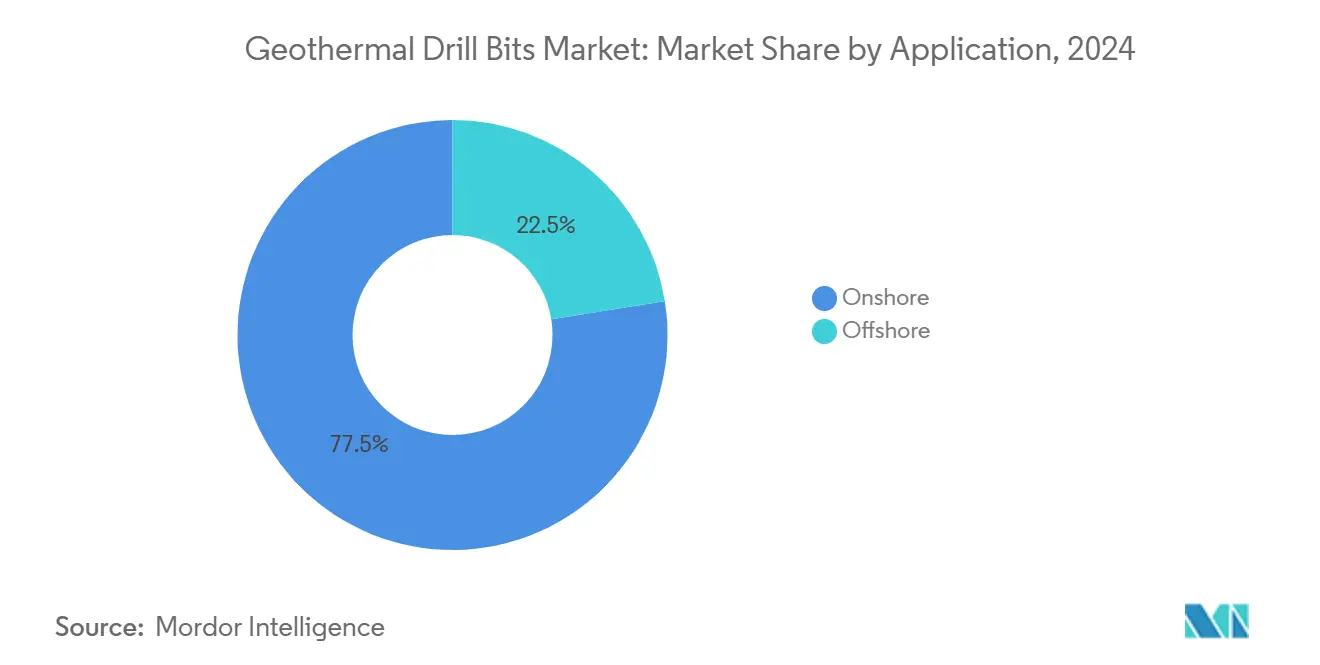

- By application, onshore drilling commanded 77.5% of the geothermal drill bits market size in 2024, whereas offshore wells expanded at a 12.5% CAGR to 2030.

- By geography, North America led with a 35.3% revenue share in 2024; the Asia-Pacific region shows the highest 11.9% CAGR over the forecast horizon.

Global Geothermal Drill Bits Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global renewable baseload targets accelerating geothermal capacity additions | +2.80% | Global (notably US, China, Indonesia) | Medium term (2-4 years) |

| Rapid penetration of PDC & hybrid bits lowering cost-per-foot | +2.10% | North America & Europe, expanding to APAC | Short term (≤ 2 years) |

| Fiscal incentives & clean-energy mandates across key regions | +1.90% | North America, Europe, select APAC markets | Medium term (2-4 years) |

| Oil & gas service firms repurposing idle rigs & logistics to geothermal | +1.60% | North America, Europe, Middle East | Short term (≤ 2 years) |

| Long-term offtake deals from data-center operators unlocking new wells | +1.30% | North America, select European markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Global Renewable Baseload Targets Accelerating Geothermal Capacity Additions

International commitments to triple renewable energy capacity by 2030 position geothermal power as the only dispatchable renewable energy source capable of 24/7 generation, thereby raising drilling intensity across both mature and frontier fields. The International Energy Agency estimates that geothermal resources could meet 15% of worldwide electricity demand by 2050, translating into thousands of new wells that require advanced bits capable of cutting through high-temperature, hard-rock reservoirs. Enhanced Geothermal Systems (EGS) expand accessible resources to an estimated 300,000 exajoules within 8 km depth, delivering 4,000 petawatt-hours of technical potential—roughly 150 times 2025 global demand. The current installed capacity reached 16,355 MW in 2023 and is projected to climb to 28 GW by 2030, then 110 GW by mid-century, providing a steady project pipeline for geothermal drill bit market suppliers. Government climate policies and energy-security priorities reinforce this momentum, ensuring sustained procurement of robust, temperature-resistant bit technologies.

Rapid Penetration of PDC & Hybrid Bits Lowering Cost-Per-Foot

The diffusion of PDC technology from hydrocarbon wells into geothermal operations is slashing cost-per-foot and compressing drilling timelines. Sandia National Laboratories documented drilling time cuts of more than 70% in Utah EGS wells using PDC bits that combine diamond cutters and optimized hydraulics.(1)Sandia National Laboratories, “PDC Bit Performance in Utah FORGE,” ENERGY.GOV NOV’s Phoenix Series with ION+ cutters, purpose-built for geothermal abrasiveness, pushes penetration rates while extending bit life, translating into lower trip counts and reduced non-productive time.(2)NOV, “ION+ Cutter Technology for Geothermal Applications,” DRILLINGCONTRACTOR.ORGHybrid designs that merge PDC and roller-cone elements further widen the performance envelope across mixed lithologies commonly encountered in single geothermal trajectories. Because drilling can account for 75% of total project spend, every incremental efficiency improvement directly shifts project economics, cementing PDC and hybrid bits as a central growth lever for the geothermal drill bits market.

Fiscal Incentives & Clean-Energy Mandates Across Key Regions

Policy instruments are lowering project risk and accelerating capital formation. In the United States, the Inflation Reduction Act provides USD 51 billion in Production Tax Credits and over USD 60 billion in Investment Tax Credits, which directly benefit geothermal developments. Additional USD 84 million in federal grants target EGS research, while states such as Colorado allocate dedicated budgets and streamline permitting to compress timelines. G20 economies collectively invested USD 168 billion in renewable energy support in 2023, a portion of which underwrites the development of geothermal exploration wells and pilot plants. Similar fiscal frameworks in Europe and selected Asia-Pacific markets are boosting financial returns on drilling equipment, thereby reinforcing order books for geothermal drill bit manufacturers.

Oil & Gas Service Firms Repurposing Idle Rigs & Logistics to Geothermal

Veteran oilfield service companies are redeploying idle capacity toward geothermal ventures, shortening the learning curve and improving supply-chain resilience. Halliburton’s portfolio includes 127 geothermal patents, while Baker Hughes’ Wells2Watts consortium retrofits decommissioned hydrocarbon wells into closed-loop geothermal demonstrators. SLB collaborates with Star Energy Geothermal and Ormat Technologies to integrate advanced logging, completion, and bit technologies refined in deep-water oil campaigns. Leveraging existing rig fleets and logistics cuts mobilization costs and mitigates execution risk, supporting faster scale-up of geothermal programs worldwide.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront well-drilling risk & CAPEX | -1.80% | Global (especially emerging markets) | Medium term (2-4 years) |

| Limited availability of high-temperature elastomers & bearings | -1.20% | Global supply chain, niche producers | Short term (≤ 2 years) |

| Critical-mineral (WC, synthetic diamond) supply bottlenecks | -1.10% | Global, dependency on China for WC | Short term (≤ 2 years) |

| Lengthy permitting for super-critical (> 450 °C) projects | -0.90% | Developed markets with complex rules | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Well-Drilling Risk & CAPEX

Drilling accounts for up to 75% of capital expenditures (capex) for a geothermal development, and uncertainties in subsurface permeability, temperature, and pressure expose investors to significant failure risk. Enhanced Geothermal Systems compound that risk through added costs for reservoir stimulation, with final productivity hard to predict despite advanced modeling. Prolonged timelines of 5–7 years from exploration to commercial operation inflate financing charges and expose projects to shifting regulations. Mitigation measures such as government-backed risk-sharing and unitized insurance pools are gaining traction, and continuous improvements in seismic imaging, data analytics, and automated drilling partially offset the restraint.

Limited Availability of High-Temperature Elastomers & Bearings

The operational life of bottom-hole assemblies is often constrained by elastomer degradation and bearing fatigue at temperatures exceeding 300 °C, with only a handful of suppliers qualified to deliver Y267 EPDM or KALREZ perfluoro-elastomers in sufficient volume. The U.S. Department of Energy’s harsh-environment materials roadmap flags gaps in scale-up pathways for next-generation seals, sleeves, and bearing alloys. Production constraints lengthen lead times and increase costs, hindering rapid deployment, particularly for pilot EGS wells that exceed temperature envelopes of 350 °C. Ongoing R&D into ceramic composites and additive manufacturing is promising but unlikely to fully resolve near-term shortages.

Segment Analysis

By Type: PDC Dominance Drives Innovation

PDC bits captured 44.8% share of the geothermal drill bits market size in 2024, reflecting their exceptional abrasion resistance and penetration efficiency in crystalline rock. The advantage owes much to oil-and-gas-sector R&D that matured synthetic diamond sintering and cutter geometry, now repurposed for geothermal heat extremes. Because the rate of penetration is a primary cost determinant, operators are increasingly prioritizing real-time torque and weight-on-bit optimization algorithms that pair seamlessly with PDC tools, thereby boosting overall field economics.

Tricone roller cone bits, although traditional, are expected to register a robust 13.6% CAGR to 2030, signaling renewed interest in their ability to tackle heterogeneous formations without excessive vibration. Hybrid configurations integrating PDC cutters on roller cones offer a compromise that widens bit applicability, especially in multi-stage holes intersecting contrasting lithologies. Diamond-impregnated core bits retain a niche for slim-hole reconnaissance and coring, while emerging plasma-assisted and laser-enhanced systems remain at technology-readiness levels below widespread commercialization. Continuous design refinement, such as NOV’s ION+ cutters and Baker Hughes’ Kymera Mach 5, assures that innovation remains brisk across every product category in the geothermal drill bits market.

Note: Segment shares of all individual segments available upon report purchase

By Application: Onshore Leadership with Offshore Acceleration

Onshore wells accounted for 77.5% of the geothermal drill bits market share in 2024, a dominance underpinned by decades of hydrothermal development and the rapid rise of Enhanced Geothermal Systems in continental basins. Mature networks of service yards, rig fleets, and road infrastructure further tilt economics toward terrestrial projects, keeping drilling activity concentrated in resource-rich corridors from the U.S. Great Basin to Indonesia’s volcanic arcs. The prolific expansion of horizontal EGS wells, with documented 35% learning curve effects by Fervo Energy, underscores the scalability of onshore technologies.

Offshore geothermal, although nascent, is projected to expand at a 12.5% CAGR through 2030, catalyzed by shallow-shelf ventures that recycle jack-up rigs from wind and oil fields. European players have initiated seismic campaigns off the Dutch and Norwegian coasts, while Asia-Pacific firms explore Japan’s Okinawa Trough. The synergy between subsea power transmission already built for offshore wind and potential co-location cost savings raises the strategic profile of offshore geothermal, signaling fresh demand segments for corrosion-resistant, pressure-balanced bit assemblies.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America accounted for 35.3% of global revenue in 2024, driven by 3,900 MW of installed capacity across California, Nevada, and Utah. The Inflation Reduction Act funnels over USD 110 billion in combined tax credits for geothermal, while USD 84 million is earmarked for EGS research to sustain technology innovation pipelines.(3)Third Way, “Clean Energy Tax Incentives Explained,” THIRDWAY.ORG Emergency permitting reforms shorten approval windows, and cross-sector collaborations—such as Baker Hughes teaming with Continental Resources—tap existing hydrocarbon skill sets to scale drilling productivity. Canada’s integration of geothermal heat networks heightens offtake diversity beyond electricity, whereas Mexico’s 976 MW base signals incremental expansion tied to industrial cogeneration needs.

Europe’s steady growth relies on renewable energy directives that mandate a 42.5% clean energy share by 2030. Germany and Italy push pilot EGS holes deeper than 5 km, while Iceland exports drilling expertise worldwide through the new Elemental Energies venture. Regulatory clarity is improving; Scotland released a dedicated geothermal permitting framework in 2024, which reduces documentation by 25% year on year. The integration of geothermal energy with district-heating schemes, especially in Nordic countries, drives consistent demand for tools, even in the absence of major electricity capacity additions.

Asia-Pacific posts the highest regional CAGR at 11.9%, propelled by China’s record-breaking 5,200-m Hainan well and India’s launch of 10 GW exploration blocks. Indonesia’s 2,418 MW operating base and vast 29.5 GW potential ensure continuous rig mobilizations, and the Philippines maintains above-average capacity factors that justify reinvestment in durable bit technologies. Japan’s policy shift to expedite seismic exploration—supported by SGD 16 million in Singapore’s advanced-imaging R&D—broadens the addressable market for geothermal drill bits across the wider region.

Competitive Landscape

The geothermal drill bits market is moderately fragmented. Large diversified service companies—Baker Hughes, SLB, and Halliburton—capitalize on decades of high-temperature drilling experience. Halliburton alone filed 127 geothermal-related patents between 2002 and 2022, illustrating a sustained commitment to extreme-environment technologies. Baker Hughes markets Vanguard geothermal bits and Kymera Mach 5 hybrids, while SLB integrates downhole telemetry and bit design through collaborations with Ormat and Star Energy.

Specialist manufacturers concentrate on segment-specific innovation. NOV’s ReedHycalog division emphasizes cutter metallurgy with its ION+ line engineered for abrasive volcanic formations. Mincon Group and Varel Energy Solutions supply region-tailored designs to operators in Indonesia and the Philippines, leveraging agile manufacturing to customize for local lithology. Technology differentiation is increasingly pivoting on materials science—high-temperature elastomers, nano-toughened PDC substrates, and erosion-resistant matrix bodies—areas where smaller firms can out-innovate conglomerates.

Strategic partnerships and acquisitions are reshaping market dynamics. Drilling Tools International’s 2024 acquisition of Titan Tools Services expanded its European distribution channels, while Star Equity Holdings acquired Alliance Drilling Tools to gain access to premium thread manufacturing. Combined with cross-border joint ventures such as Elemental Energies and Iceland Drilling, these moves suggest a gradual consolidation phase aimed at scaling R&D and securing raw-material supply against volatile tungsten carbide and synthetic diamond markets.

Geothermal Drill Bits Industry Leaders

-

Baker Hughes Co.

-

SLB (Schlumberger NV)

-

Halliburton Company

-

NOV Inc.

-

Epiroc AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: XGS Energy secured an additional USD 13 million in funding to accelerate geothermal deployment, bringing total funding to over USD 100 million with 183 MW of offtake agreements from hyperscaler customers, demonstrating strong data center demand for geothermal solutions.

- February 2025: Elemental Energies and Iceland Drilling launched a global geothermal joint venture to enhance project development capabilities, combining Iceland's specialized geothermal expertise with international expansion capabilities.

- February 2025: Baker Hughes announced collaborations with Eden Geothermal for UK geothermal opportunities and PETROVIETNAM for enhanced drilling operations, expanding international geothermal service capabilities.

- January 2025: SLB and Star Energy Geothermal announced a technology collaboration to accelerate advanced geothermal asset development, focusing on subsurface characterization and production technologies.

Global Geothermal Drill Bits Market Report Scope

| Tricone Roller Cone Bits |

| Polycrystalline Diamond Compact (PDC) Bits |

| Hybrid (PDC-Roller Cone) Bits |

| Diamond Impregnated Core Bits |

| Others |

| Onshore | Conventional Hydrothermal Fields |

| Enhanced Geothermal Systems (EGS) | |

| Super-critical and Deep (Above 5 km) | |

| Offshore | Shallow-water Continental Shelf |

| Deep-water Prospects |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Tricone Roller Cone Bits | |

| Polycrystalline Diamond Compact (PDC) Bits | ||

| Hybrid (PDC-Roller Cone) Bits | ||

| Diamond Impregnated Core Bits | ||

| Others | ||

| By Application | Onshore | Conventional Hydrothermal Fields |

| Enhanced Geothermal Systems (EGS) | ||

| Super-critical and Deep (Above 5 km) | ||

| Offshore | Shallow-water Continental Shelf | |

| Deep-water Prospects | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the geothermal drill bits market in 2025?

The geothermal drill bits market size is USD 189.20 million in 2025, with a 9.39% CAGR projected through 2030.

Which bit type currently dominates sales?

PDC bits lead with 44.8% market share in 2024 owing to their durability in hard-rock, high-temperature reservoirs.

What region is expanding fastest?

Asia-Pacific posts the highest regional CAGR at 11.9% thanks to aggressive drilling programs in China, India, and Indonesia.

How do data-center offtake agreements affect demand?

Long-term power purchase agreements from hyperscale data centers improve project bankability and stimulate additional drilling activity.

What are the main supply-chain risks for manufacturers?

Dependence on tungsten carbide and synthetic diamonds, particularly from China, and limited high-temperature elastomer production present key supply risks.

Are offshore geothermal projects a near-term opportunity?

Shallow-shelf pilots are underway and drive a 12.5% CAGR for offshore applications, but deep-water prospects remain longer-term plays.

Page last updated on: