GCC ICT Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 141.32 Billion |

| Market Size (2030) | USD 222.37 Billion |

| Growth Rate (2025 - 2030) | 9.49% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

GCC ICT Market Analysis by Mordor Intelligence

The GCC ICT market size stands at USD 141.32 billion in 2025 and is forecast to reach USD 222.37 billion by 2030, expanding at a 9.49% CAGR over the period. This momentum reflects vision-led digital-economy budgets, hyperscale cloud region build-outs, and near-universal 5G deployment targets that together anchor demand for advanced connectivity, cloud, and AI services. Sovereign wealth funds are financing indigenous technology capacity, while mandatory digitization of public services creates structural demand that cushions the GCC ICT market from cyclicality. Gaming, esports, and edge computing solutions are emerging as outsized growth pockets, supported by youth demographics and smart-city mega-projects. At the same time, the region’s chronic cyber-skills gap and water-scarcity pressures on hyperscale cooling infrastructure temper the otherwise robust outlook.

Key Report Takeaways

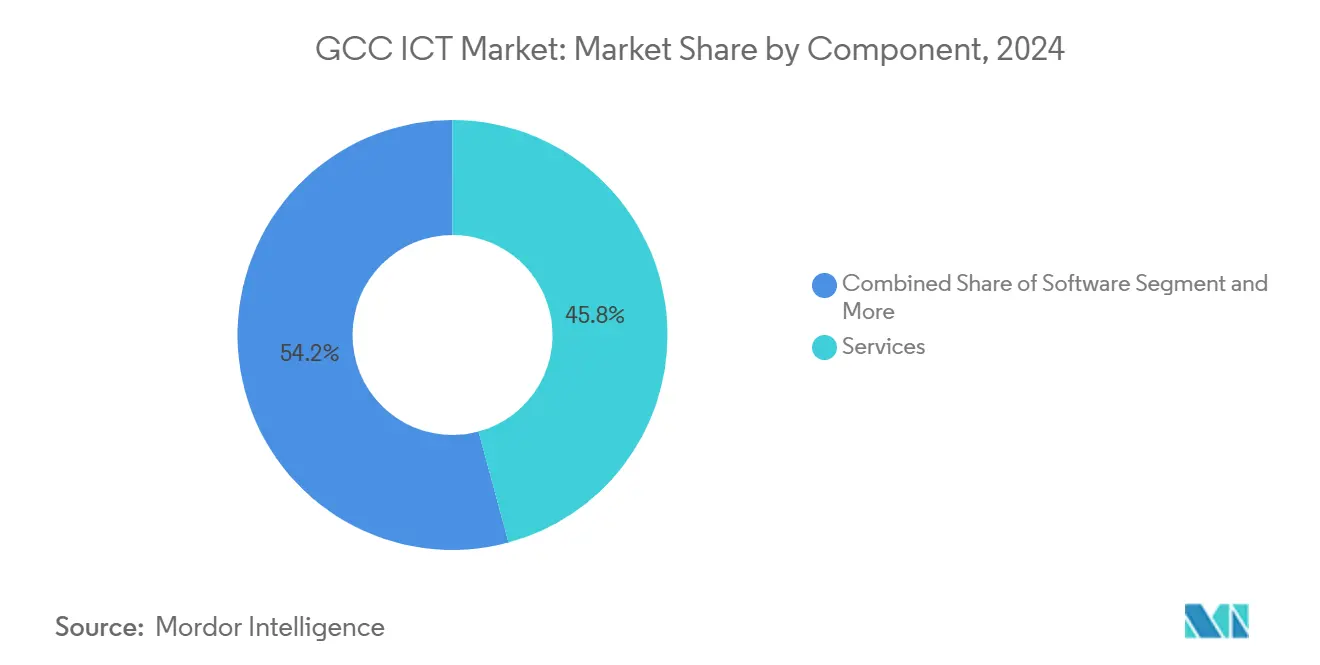

- By component, IT Services held 34.2% of the GCC ICT market share in 2024, while IT Infrastructure is advancing at a 15.0% CAGR to 2030.

- By enterprise size, Large Enterprises controlled 61.9% of spending in 2024; Small and Medium Enterprises are projected to grow at an 11.5% CAGR through 2030.

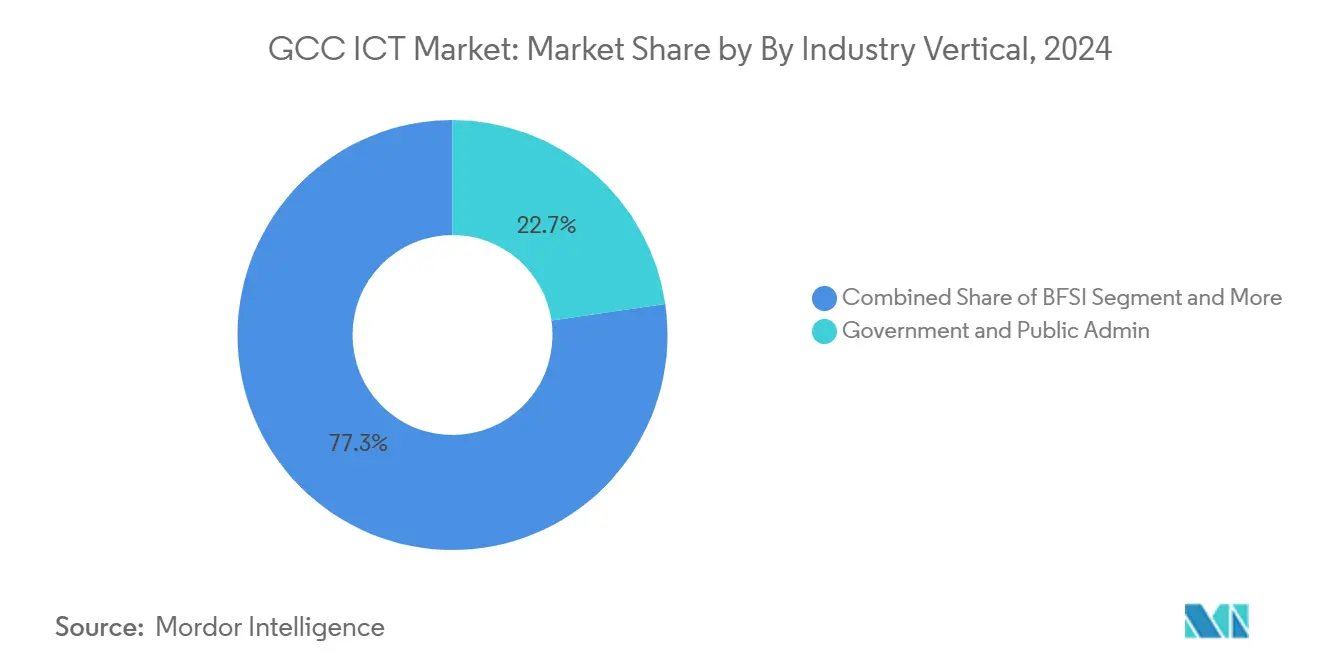

- By industry vertical, Government and Public Administration captured 22.7% of the GCC ICT market size in 2024, whereas Gaming and Esports is expanding at a 20.1% CAGR to 2030.

- By deployment model, cloud-only environments accounted for 25.9% of spending in 2024 and are growing at a 23.6% CAGR to 2030.

- By geography, Saudi Arabia and the United Arab Emirates jointly represented about 70% of regional outlays in 2024 and together are forecast to sustain double-digit growth through 2030.

- AWS, Microsoft, and Oracle dominated regional hyperscale investments, while e&, Ooredoo, and stc collectively held more than 55% of telecom cloud and managed service revenues in 2024.

GCC ICT Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision-led digital-economy budgets | +2.1% | Saudi Arabia, UAE primary | Long term (≥ 4 years) |

| 5G/FTTx urban coverage ≥ 95% by 2027 | +1.8% | GCC-wide | Medium term (2-4 years) |

| Hyperscale cloud region build-outs | +1.6% | Saudi Arabia, UAE | Medium term (2-4 years) |

| Smart-city mega-projects | +1.3% | Saudi Arabia, UAE | Long term (≥ 4 years) |

| Sovereign AI capital pools | +1.0% | Saudi Arabia, UAE | Long term (≥ 4 years) |

| Green-hydrogen MoUs for data-center OPEX | +0.7% | GCC-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision-led Digital-Economy Budgets Drive Unprecedented ICT Investments

National transformation programs are anchoring long-term demand as governments allocate ring-fenced budgets for cloud, AI, and cybersecurity. Saudi Arabia earmarked USD 40 billion for AI and launched a USD 1 billion accelerator that mandates on-shore operations for foreign firms, thereby stimulating local capacity building. The UAE’s We the UAE 2031 targets 11 million daily digital interactions, compelling agencies to modernize core systems. Qatar, Kuwait, and Oman are adopting scaled variants, which together create predictable multiyear project pipelines across the GCC ICT market.

5G/FTTx Infrastructure Rollouts Accelerate Digital Service Adoption

Telecom operators are racing toward ≥ 95% urban 5G and fiber coverage, enabling low-latency use cases that spur incremental spending on edge computing and IoT. Saudi Telecom Company deployed Nokia’s AI-driven MantaRay SON to optimize 5G performance during peak events. The UAE’s e& became the first regional operator to integrate Ciena’s WaveLogic 6 Extreme optics, raising backbone capacity to 1.6 Tbit/s. Such rollouts position the GCC ICT market for rapid uptake of cloud gaming, autonomous mobility, and remote surgery services.

Hyperscale Cloud Region Build-outs Transform Service Delivery Models

AWS committed USD 5.3 billion for local zones in Saudi Arabia, while Microsoft and G42 launched sovereign cloud regions in Abu Dhabi, reducing latency and meeting data-residency rules. Oracle is adding a second regional hub and pairing with Google Cloud for multicloud data services. These investments enable enterprises to decommission legacy on-premises estates, reinforcing cloud-only momentum within the GCC ICT market.

Smart-City Mega-Projects Create Technology Integration Opportunities

Projects such as NEOM, Masdar City, and Dubai Silicon Oasis function as living labs for integrated AI, IoT, and renewable-powered data-center fabrics. NEOM signed a USD 5 billion deal with DataVolt to build a 1.5 GW AI data-center campus, paired with Samsung C&T for construction robotics that can cut manual labor by 80%. Successful pilots in these mega-projects cascade across municipal smart-city deployments, broadening addressable demand for integrators and platform vendors in the GCC ICT market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-skills gap—import dependency > 65% | -1.4% | GCC-wide | Short term (≤ 2 years) |

| Oil-price cyclicality throttling cloud spend | -1.1% | Kuwait, Oman, Bahrain | Short term (≤ 2 years) |

| Water-scarcity constraints on DC cooling | -0.8% | GCC-wide | Medium term (2-4 years) |

| Divergent data-residency mandates | -0.6% | GCC-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Chronic Cyber-Skills Gap Constrains Implementation Capabilities

With only 35% of required specialists available locally, organizations must import expertise, inflating project costs and delaying go-lives. Saudi and UAE initiatives aim to train 20,000 AI professionals, yet near-term shortages persist. Smaller economies experience deeper deficits, complicating cybersecurity posture across the GCC ICT market.

Oil-Price Cyclicality Impacts Enterprise Technology Spending

When Brent prices dip, Kuwait, Oman, and Bahrain often defer discretionary IT upgrades, dampening short-term cloud migration pipelines. Although diversification is reducing sensitivity, pockets of volatility remain a restraint on sustained uptake, particularly outside Saudi Arabia and the UAE.

Segment Analysis

By Component: Services Leadership Amid Infrastructure Acceleration

IT Services contributed 34.2% of 2024 revenue, underscoring the preference for end-to-end project delivery partners in the GCC ICT market. Hyperscale data-center build-outs and 5G rollouts are propelling IT Infrastructure to a 15.0% CAGR, signaling a pivot toward hardware refreshes and edge nodes that underpin AI workloads. Zain KSA’s cloud-based BSS/OSS migration cut product launch times by 50%, illustrating infrastructure modernizations that drive incremental service revenues [1]Netcracker Technology, “Zain KSA Completes Major Digital Transformation Program,” netcracker.com. The interplay between new hardware demand and managed services implies robust multi-year growth trajectories.

At the same time, GCC governments favor framework agreements that bundle consulting, integration, and support into multiyear contracts, sustaining IT Services dominance. However, hardware suppliers are capturing share in high-density servers, liquid cooling, and photonics interconnects as AI training clusters proliferate. This balanced expansion anchors long-term opportunities for vendors across the GCC ICT market.

Note: Segment shares of all individual segments available upon report purchase

By Enterprise Size: SME Acceleration Challenges Large-Enterprise Dominance

Large Enterprises accounted for 61.9% of expenditure in 2024, reflecting resource advantages in adopting multi-cloud and zero-trust architectures. Yet SMEs are registering an 11.5% CAGR to 2030 as SaaS subscription models democratize advanced capabilities. Ooredoo’s Kloudville marketplace brings AI, cybersecurity, and ERP tools to more than 400,000 regional SMEs via pay-as-you-grow plans. This model reduces capital barriers and narrows the digital divide within the GCC ICT market.

Government grants and incubation zones in Dubai Silicon Oasis and Bahrain’s FinTech Bay further accelerate SME digitalization. As localized AI copilots and no-code platforms mature, SMEs are expected to account for progressively larger slices of the GCC ICT market size across support, commerce, and creative sectors.

By Industry Vertical: Government Leadership Amid Gaming Sector Disruption

Government and Public Administration held 22.7% of outlays in 2024, driven by citizen-service portals, interoperable ID frameworks, and defense cybersecurity grids. Mandatory e-invoicing and cross-border customs digitization programs sustain steady demand. Simultaneously, Gaming and Esports is surging at a 20.1% CAGR as Saudi Arabia’s Public Investment Fund injects billions into studios, IP acquisition, and tournament infrastructure. Regional 5G rollouts eliminate latency barriers, catalyzing cloud gaming adoption and diversifying revenue streams within the GCC ICT market.

Banks, insurers, and energy firms continue modernizing core systems, yet face regulatory scrutiny on data localization. Healthcare’s permanent shift to telehealth and e-pharmacy platforms post-pandemic reinforces cross-vertical demand for secure cloud and analytics solutions.

Note: Segment shares of all individual segments available upon report purchase

By Deployment Model: Cloud-Only Momentum Reshapes Infrastructure Strategies

Cloud-only environments captured 25.9% share in 2024 and are rising at a 23.6% CAGR, aided by sovereign cloud zones that meet data-residency norms. Microsoft’s tie-up with G42 underpins a national AI-native government push, catalyzing lift-and-shift as well as cloud-native development[2]Microsoft. "Microsoft and G42 partner to accelerate AI innovation in UAE and beyond." April 15, 2024. https://blogs.microsoft.com/blog/2024/04/15/microsoft-and-g42-partner-to-accelerate-ai-innovation-in-uae-and-beyond/. Hybrid models remain prevalent for regulated workloads, yet the cost-performance advantages of regional hyperscale nodes are accelerating full cloud adoption across the GCC ICT market.

Edge zones integrated with national 5G cores cut latency below 5 milliseconds, enabling industrial robotics and AR-assisted field maintenance. As zero-trust frameworks mature, security concerns that once favored on-premises deployments are diminishing.

Geography Analysis

Saudi Arabia and the UAE jointly generated nearly 70% of 2024 spending, underpinned by USD 100 billion AI allocations and USD 18 billion data-center commitments that dwarf regional peers. Saudi Arabia’s data-center capacity is projected to reach 854 MW by 2029, supporting multiple sovereign AI workloads. The UAE hosts 38 operational data centers and is expanding into green-powered facilities linked to its renewable portfolio. Both countries leverage diversified economies that sustain ICT outlays irrespective of oil-price volatility, positioning them as technology adoption bellwethers for the broader GCC ICT market.

Qatar maintains momentum through National Vision 2030 and mega-event infrastructure upgrades. Ooredoo’s 13% total shareholder return between 2019-2023 underscores telecom sector value creation, while a USD 550 million financing boosts regional data-center capacity beyond 120 MW [3]SAMENA Council, “Qatar’s Ooredoo Secures Position as Ninth Highest Value Creator,” samenacouncil.org . Qatar’s focus on AI-optimized data centers augments its role as a managed-service export hub to smaller GCC economies.

Kuwait, Oman, and Bahrain pursue selective modernization. Oman’s Vision 2040 emphasizes e-government and logistics tech, while Bahrain’s open-banking regulations spur fintech cloud uptake. Cross-border interconnection projects enable these markets to piggyback on Saudi and Emirati hyperscale regions, ensuring access to advanced cloud and AI services without duplicative capital spends. Collectively, diversified strategies across member states sustain resilient growth within the GCC ICT market.

Competitive Landscape

Top Companies in GCC ICT Market

Global hyperscalers AWS, Microsoft, Google Cloud, and Oracle are injecting multi-billion dollar capital to localize infrastructure, intensifying competitive pressure yet opening partnership avenues for telecom operators and local integrators. e&, Ooredoo, stc, Zain KSA, and du are evolving from connectivity providers to end-to-end digital solution orchestrators by bundling managed security, IoT, and edge services. Their combined revenue share in telecom cloud exceeded 55% in 2024, exemplifying incumbent strength within the GCC ICT market.

Systems integrators such as Accenture, IBM, and Tata Consultancy Services vie with regional specialists for complex transformation deals that require Arabic localization and compliance expertise. G42’s acquisition of cybersecurity firm CPX creates an AI-infused security stack that differentiates it against international peers [4]AIbase, “G42 Acquires Abu Dhabi Cybersecurity Company CPX,” aibase.com . Vendor success increasingly hinges on local capacity building, joint venture structures, and talent-development commitments that align with sovereign priorities.

Emerging disruptors include fintech, health-tech, and gaming studios leveraging cloud-native architectures to scale rapidly at lower cost. Government accelerators and sandboxes reduce go-to-market friction, encouraging niche innovators to challenge incumbents. The resulting ecosystem balances the dominance of global majors with a vibrant cadre of homegrown players, shaping a moderately concentrated yet dynamic GCC ICT market.

GCC ICT Industry Leaders

-

Google LLC (Alphabet Inc.)

-

IBM Corporation

-

Microsoft Corporation

-

HP Inc.

-

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Abu Dhabi, Microsoft, and G42 announced a multi-year sovereign cloud partnership underpinning 11 million daily digital interactions.

- March 2025: Zain KSA completed a cloud-BSS/OSS overhaul with Netcracker, halving product launch cycles.

- March 2025: e& and Samsung Electronics signed an MoU to co-develop AI-powered connectivity solutions.

- March 2025: Ooredoo partnered with Kloudville to launch an SME digital marketplace across six MENA nations.

GCC ICT Market Report Scope

The GCC ICT market includes the amalgamation and adoption of different Information and Communications Technologies (ICT), such as big data, mobility, storage, outsourcing, and cloud computing in the GCC countries for the purpose of digitization, digital transformation, and tracking the revenue accrued through the sale of technology-related solutions.

The GCC ICT market is segmented by technology (big data analytics, mobility and telecom, cloud computing, storage, and business process outsourcing), component (hardware/devices, software and services, and communication and connectivity), and end-user industry (oil, gas and utilities, travel and hospitality, healthcare, financial services, manufacturing and construction, and other end-user industries). The market size and forecasts are provided in terms of value (USD) for all the above segments.

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | Managed Services |

| Business Process Services | |

| Business Consulting Services | |

| Cloud Services | |

| IT Infrastructure | |

| IT Security | |

| Communication Services |

| Small and Medium Enterprises |

| Large Enterprises |

| Government and Public Administration |

| Banking, Financial Services and Insurance |

| Energy and Utilities |

| Retail, E-commerce and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| Oil and Gas (Up-/Mid-/Down-stream) |

| Gaming and Esports |

| Other Verticals |

| On-premises |

| Cloud-only |

| Hybrid |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Oman |

| Kuwait |

| Bahrain |

| By Component | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | Managed Services | |

| Business Process Services | ||

| Business Consulting Services | ||

| Cloud Services | ||

| IT Infrastructure | ||

| IT Security | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By Industry Vertical | Government and Public Administration | |

| Banking, Financial Services and Insurance | ||

| Energy and Utilities | ||

| Retail, E-commerce and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| Oil and Gas (Up-/Mid-/Down-stream) | ||

| Gaming and Esports | ||

| Other Verticals | ||

| By Deployment Model | On-premises | |

| Cloud-only | ||

| Hybrid | ||

| By Country | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Oman | ||

| Kuwait | ||

| Bahrain | ||

Key Questions Answered in the Report

How large is the GCC ICT market in 2025 and how fast is it growing?

It is valued at USD 141.32 billion in 2025 and is projected to grow at a 9.49% CAGR to USD 222.37 billion by 2030.

Which component contributes the most revenue?

IT Services leads with 34.2% share, reflecting preference for end-to-end transformation partners.

What segment is expanding the fastest?

Gaming and Esports is forecast to rise at a 20.1% CAGR through 2030, fueled by youth demographics and public investment.

Why are cloud-only deployments accelerating?

Regional hyperscale zones satisfy data-residency rules, reduce latency, and offer cost advantages that drive rapid migration.

Page last updated on: