Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

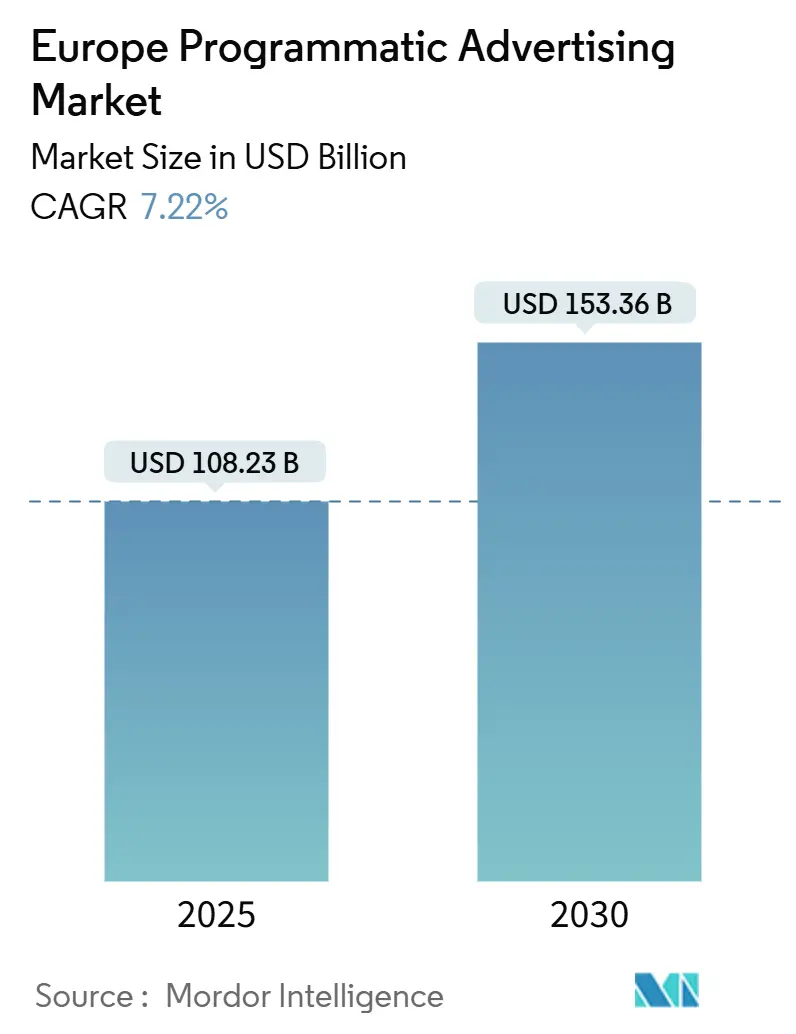

| Market Size (2025) | USD 108.23 Billion |

| Market Size (2030) | USD 153.36 Billion |

| Growth Rate (2025 - 2030) | 7.22% CAGR |

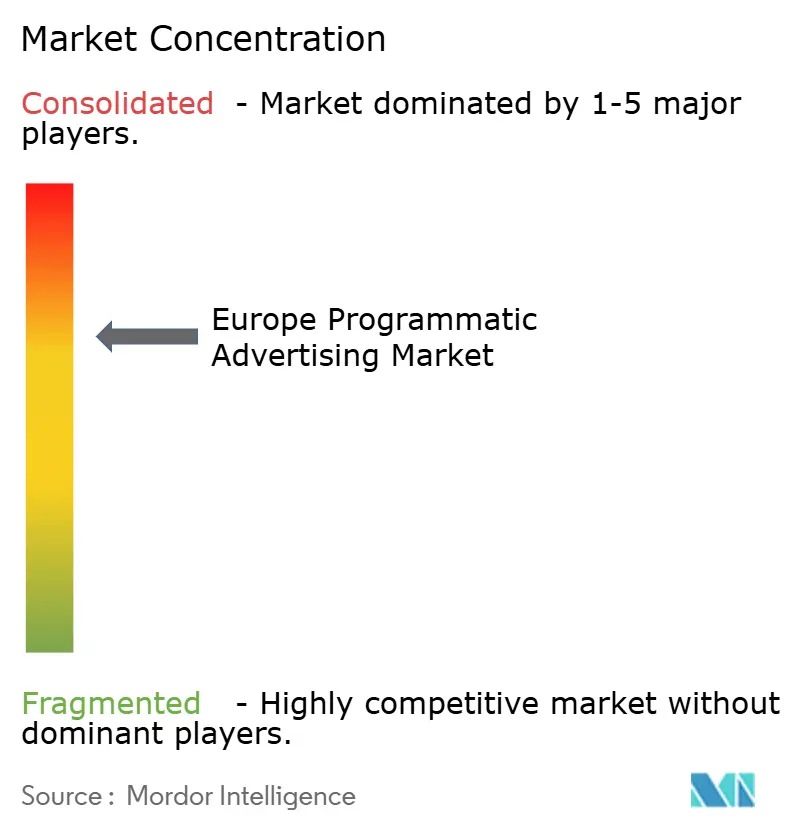

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Programmatic Advertising Market Analysis by Mordor Intelligence

The Europe Programmatic Advertising market size reached USD 108.23 billion in 2025 and is projected to expand to USD 153.36 billion by 2030, advancing at a 7.22% CAGR. This solid outlook stems from surging digital media consumption, rapid Connected TV (CTV) adoption, and the broad rollout of GDPR-compliant data strategies. Real-Time Bidding (RTB) continues to anchor automated trading, while programmatic guaranteed deals scale quickly as publishers seek revenue stability. Retail media networks deepen the addressable inventory pool, and investments in supply-chain transparency standards bolster advertiser confidence. Simultaneously, stringent privacy laws, rising sustainability expectations, and persistent ad-fraud pressures require ongoing technology and governance upgrades across the Europe Programmatic Advertising market.[1]IAB Europe, “AdEx Benchmark 2024 Report,” iabeurope.eu

Key Report Takeaways

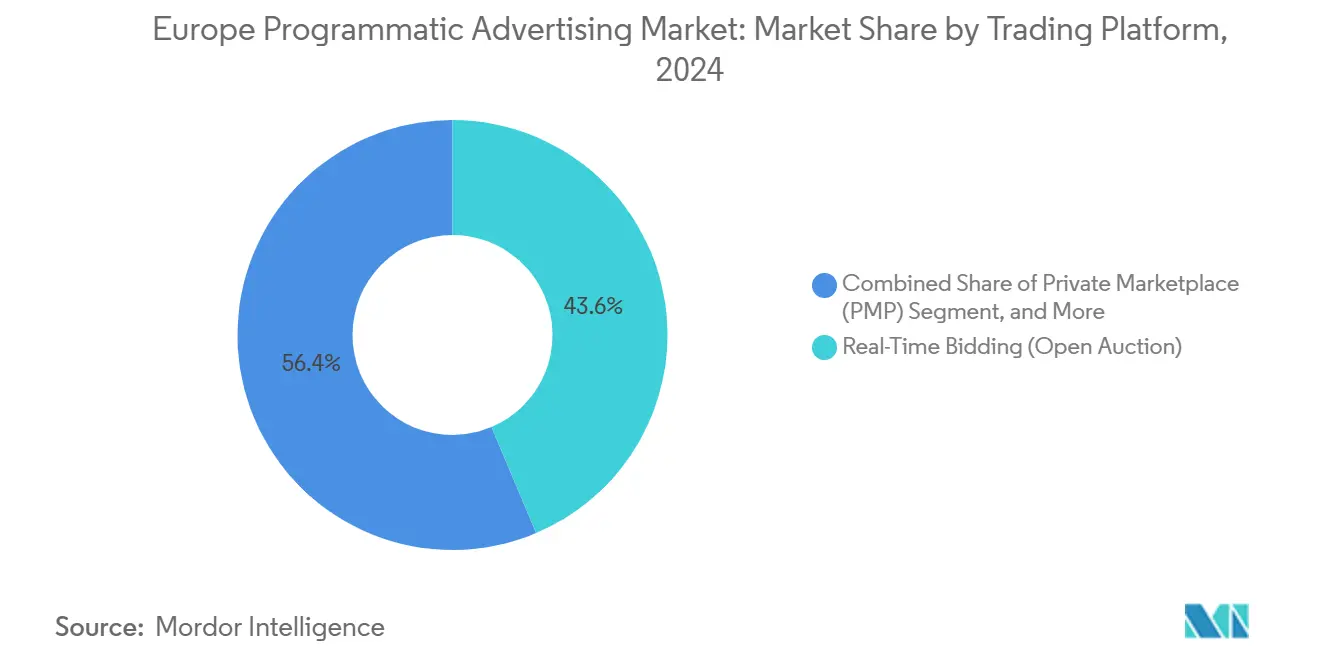

- By trading platform, RTB held 43.63% of Europe Programmatic Advertising market share in 2024, while programmatic guaranteed is forecast to grow at 8.45% CAGR to 2030.

- By advertising media, CTV and online video commanded 37.63% of Europe Programmatic Advertising market size in 2024, and digital out-of-home is advancing at an 8.33% CAGR through 2030.

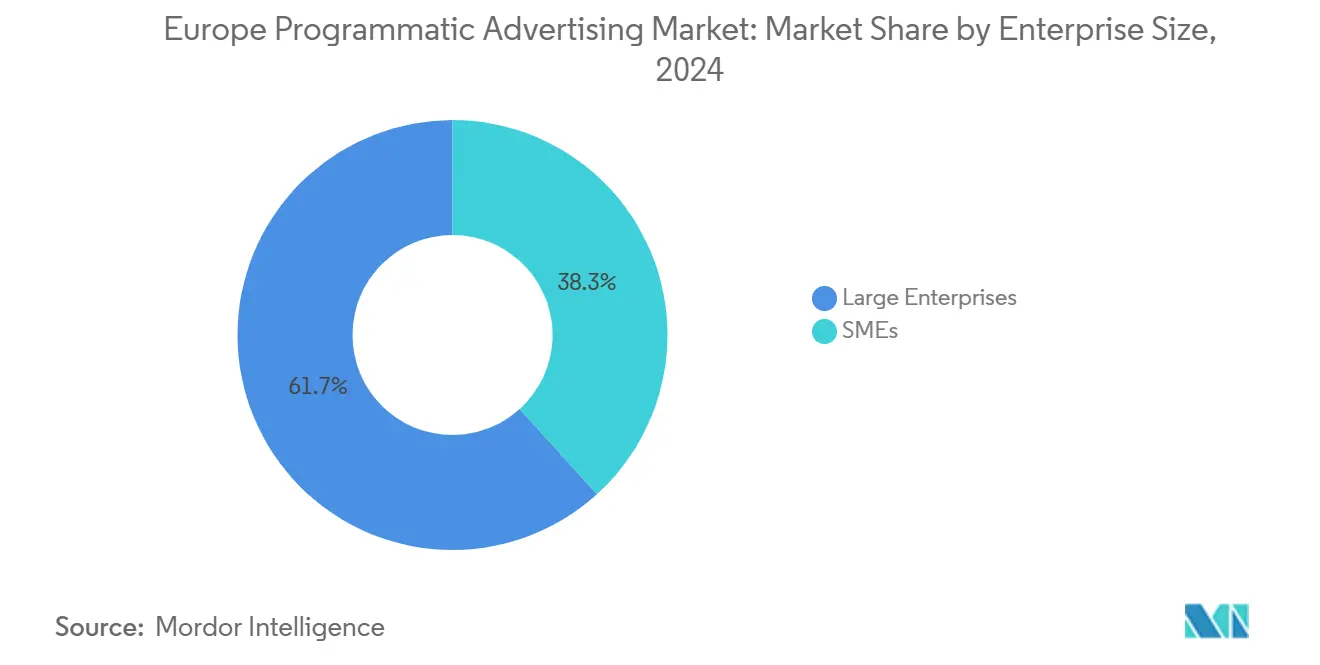

- By enterprise size, large enterprises accounted for 61.73% of Europe Programmatic Advertising market size in 2024, whereas the SME segment is progressing at an 8.76% CAGR between 2025-2030.

- By industry vertical, retail and e-commerce led with 29.84% revenue share in 2024 in Europe Programmatic Advertising market ; healthcare and pharmaceuticals is projected to register the fastest 7.99% CAGR to 2030.

- By country, the United Kingdom retained 29.83% share of Europe Programmatic Advertising market size in 2024, while Poland is expected to record the highest 8.12% CAGR through 2030

Europe Programmatic Advertising Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in digital media consumption and online video | +2.1% | Global, with DACH and Nordics leading | Medium term (2-4 years) |

| Proliferation of GDPR-compliant data for audience targeting | +1.8% | EU-wide, strongest in Germany and France | Long term (≥ 4 years) |

| Growth of Connected TV (CTV) programmatic inventory | +2.3% | UK, Germany, Netherlands core markets | Short term (≤ 2 years) |

| Accelerating adoption of mobile in-app advertising | +1.6% | Pan-European, mobile-first markets like Spain, Italy | Medium term (2-4 years) |

| Expansion of retail-media networks' programmatic offerings | +1.9% | Western Europe, retail-dense markets | Medium term (2-4 years) |

| EU Digital Markets Act spurring open-web alternatives | +1.4% | EU-27, gatekeeper-dependent markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Digital Media Consumption and Online Video

European viewers allocated more than half of their digital attention to video formats in 2024, and the imbalance between time spent and ad spend in audio and short-form video signals incremental inventory growth potential. CTV spend climbed to EUR 3.6 billion, a 23.5% year-over-year jump as broadcasters unlocked premium streams through supply-side platforms. Advanced measurement frameworks now link CTV impressions to verified outcomes, encouraging brand and performance advertisers alike to shift budgets toward Europe Programmatic Advertising market campaigns that blend reach with precision. Cross-screen sequencing tools further amplify video’s effectiveness, increasing message recall and reducing frequency waste. With near-ubiquitous fiber and 5G rollouts across the continent, bandwidth no longer limits high-definition ad delivery, enabling richer creative and seamless user experiences.[2]IAB Europe, “Vendor List TCF,” iabeurope.eu

Proliferation of GDPR-Compliant Data for Audience Targeting

Publishers and retailers invested heavily in first-party data infrastructure after the GDPR milestone year of 2018. Email, loyalty, and transaction datasets are now complemented by consented address, IP, and SDK signals, giving rise to robust audience graphs that operate without third-party cookies. IAB Europe’s Transparency and Consent Framework (TCF) lists more than 1,000 certified vendors, and 73% of major publishers have implemented ads.txt and sellers.json to ensure authorized selling paths. These measures elevate trust, cut invalid supply, and allow Europe Programmatic Advertising market participants to deploy real-time creative optimization based on lawful data triggers. The net result is a deeper, privacy-safe seed pool for look-alike modeling and contextual overlays, which expands monetization possibilities across web, app, and emerging metaverse surfaces.

Growth of Connected TV Programmatic Inventory

Broadcasters, smart-TV OEMs, and streaming platforms opened more than 200 new private marketplace lanes in 2024, bringing scalable, brand-safe inventory to demand-side platforms. Automated auction mechanisms reduce manual insertion-order friction, while multi-currency frequency management now caps ad repetition across linear and streaming feeds. Coupled with outcome-based guarantees, these advances draw incremental budget from traditional television to the Europe Programmatic Advertising market ecosystem. Marketers also benefit from household graph integrations that tie CTV exposures to e-commerce conversions, narrowing attribution loops. As national regulators phase in cross-media measurement standards, CTV’s share of video outlays is set to rise steadily throughout the forecast period.

Expansion of Retail-Media Networks’ Programmatic Offerings

European retailers monetized EUR 14.3 billion of onsite and offsite inventory in 2024, guided by commerce data that maps SKU-level intent to ad placements. Programmatic pipes now facilitate second-price auctions inside retailer ad servers, giving brands real-time visibility into bid landscapes and allowing dynamic budget shifts. Third-party marketplaces such as Mirakl bolster this capability by embedding AI-driven bid optimization modules that operate across Amazon and eBay channels. The result is a self-reinforcing flywheel: granular shopper insights fuel better targeting, leading to higher return on ad spend and yet more investment in the Europe Programmatic Advertising market retail segment. This closed-loop paradigm attracts SME advertisers who previously lacked scaled first-party insights.[3]Mirakl, “Mirakl Acquiert Adspert,” mirakl.com

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent privacy laws (GDPR, ePrivacy) limiting third-party cookies | -1.7% | EU-wide, strictest enforcement in Germany, France | Long term (≥ 4 years) |

| Persistent ad-fraud and brand-safety concerns | -1.2% | Global, heightened scrutiny in premium markets | Medium term (2-4 years) |

| Supply-path complexity and transparency issues | -0.9% | Complex programmatic markets like UK, Germany | Short term (≤ 2 years) |

| Emerging carbon-footprint scrutiny of ad-tech supply chains | -0.6% | Northern Europe sustainability leaders | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Privacy Laws Limiting Third-Party Cookies

The GDPR, ePrivacy Directive, and a patchwork of national rules restrict identifiers and mandate explicit consent, elevating compliance costs for ad-tech vendors. French watchdog CNIL catalogued more than 620 discrete systems in a typical programmatic transaction chain, each of which must now substantiate purpose limitation and data minimization claims. Large publishers deploy consent-management platforms, but smaller sites struggle with legal overhead, tempering inventory growth in the Europe Programmatic Advertising market. Parallelly, browser-level interventions curtail cookie lifespans, pushing advertisers toward contextual, cohort-based, and clean-room solutions that often carry higher implementation expenses.

Persistent Ad-Fraud and Brand-Safety Concerns

Invalid traffic siphons an estimated 5%-8% of programmatic budgets, according to registry data compiled by the Trustworthy Accountability Group. While 73% of authorized-seller files are correctly formatted, sellers.json mismatches expose lingering vulnerabilities. BidSwitch’s ads.txt targeting function mitigates some risk by filtering unauthorized domains before bid execution, yet brand-safety lapses still surface in user-generated content environments. Advertisers respond by reallocating spend to curated marketplaces and instituting impression-level log audits, raising transaction costs across the Europe Programmatic Advertising market.

Segment Analysis

By Trading Platform: RTB Anchors While Guaranteed Deals Accelerate

RTB contributed 43.63% of Europe Programmatic Advertising market share in 2024. Advertisers favor its auction efficiency, broad reach, and budget pacing flexibility. However, heightened emphasis on media quality drives publishers to augment RTB with private marketplaces that bundle audience segments and contextual signals at negotiated floors. Programmatic guaranteed, growing at an 8.45% CAGR, enables direct, IO-like commitments within automated pipes, giving both parties predictable delivery and performance. The Europe Programmatic Advertising market size for guaranteed deals is projected to climb steadily as broadcast and retail networks codify inventory packages around tent-pole events and seasonal peaks.

Private marketplaces serve as a strategic bridge, offering “first-look” access without volume guarantees. This format appeals to verticals with strict brand-safety requirements, finance, health, and government, where context and creative adjacency matter more than scale. DSP and SSP compliance with TCF v2.2 reduces legal friction, streamlines deal activation, and widens advertiser participation. Over the forecast horizon, hybrid buying frameworks that combine RTB’s reach with guaranteed deals’ certainty will become commonplace across the Europe Programmatic Advertising market, balancing cost efficiency with inventory quality.

Note: Segment shares of all individual segments available upon report purchase

By Advertising Media: CTV and Video Dominate as DOOH Surges

Online video and CTV accounted for 37.63% of Europe Programmatic Advertising market size in 2024. Household addressability, advanced audience segments, and high-impact creative drive premium pricing, and publishers leverage dynamic ad-insertion to maximize yield. Display banners remain an essential performance channel, particularly for retargeting and full-funnel sequencing. Yet the fastest-growing slice is digital out-of-home, expanding at an 8.33% CAGR as DOOH networks integrate real-time data triggers such as weather and transit flows to personalize screens.

Mobile in-app inventory is buoyed by contextual data layers that offset signal loss from cookie depreciation. App-SDK telemetry maps intent, enabling conversion-oriented formats such as playable ads and rewarded video. Audio, despite representing only 4.5% of ad spend relative to 21% of media time, offers incremental reach and low-clutter environments. As measurement unifies across screens, cross-format allocations will tighten, but video’s share should remain resilient given its superior engagement metrics within the Europe Programmatic Advertising market.

By Enterprise Size: Automation Levels the Playing Field

Large enterprises captured 61.73% of Europe Programmatic Advertising market share in 2024, leveraging in-house trade desks and proprietary data lakes. These players orchestrate omnichannel activations that blend upper-funnel branding with lower-funnel conversion tactics. Yet SMEs, advancing at an 8.76% CAGR, benefit from turnkey DSP interfaces and AI-driven optimization engines that trim campaign setup time from days to minutes. Minimum-spend thresholds have fallen sharply, and templated creative assets further lower barriers.

E-commerce integrations give SMEs visibility into SKU-level performance, enabling incremental budget shifts toward high-margin products within the Europe Programmatic Advertising market. Payment-on-results pricing models also appeal to resource-constrained advertisers, assuring spend efficacy. Over the forecast period, expect collaborative alliances between regional publishers and local business associations to offer curated packages designed specifically for SME objectives, amplifying grassroots adoption.

By Industry Vertical: Retail Leads, Healthcare Scales Fast

Retail and e-commerce held 29.84% of Europe Programmatic Advertising market size in 2024. First-party transaction data and closed-loop attribution underpin this dominance, and retailers monetize digital shelves through on-site sponsored listings and off-site audience extension. Consumer packaged goods brands tap these networks to influence purchase decisions closer to the point of sale. Healthcare and pharmaceuticals, forecast to rise at 7.99% CAGR, capitalize on telehealth adoption and clarified marketing guidelines across major EU markets. Contextual targeting combined with verified publisher lists ensures compliance and mitigates patient-data risks.

Financial services emphasize fraud-mitigation overlays, while automotive manufacturers employ sequential storytelling, from awareness to dealer footfall, across CTV and DOOH canvases. Media and entertainment firms funnel promotional spend into dynamic trailers aligned with release dates, and technology-telecom operators advertise device launches via high-impact video roadblocks. Government entities increasingly use programmatic channels for public-service communications, reflecting digital-first citizen engagement mandates. These diverse use cases reinforce the multi-vertical breadth of the Europe Programmatic Advertising market.

Geography Analysis

The United Kingdom commanded 29.83% of Europe Programmatic Advertising market share in 2024, buoyed by deep advertiser sophistication and a robust publisher ecosystem. London-based agencies pioneered programmatic innovation, and although post-Brexit regulatory nuances are complex, they have not curtailed spend growth. Germany ranks second, propelled by high GDP per capita and strong sectoral advertisers such as automotive and engineering. Its stringent privacy culture encourages early adoption of consent-first frameworks, reinforcing quality perceptions for Germany-origin inventory.

France’s luxury and retail media momentum elevates its market influence, while Italy and Spain showcase rapid mobile-first expansion, fueled by high smartphone penetration and social video consumption. The Netherlands and Belgium serve as cross-border testing grounds due to bilingual populations and strong logistics hubs that facilitate pan-EU campaigns. Poland leads Eastern Europe in vibrant DOOH and CTV deployments, illustrating how emerging-market agility can outpace the incremental growth of mature markets. Nordic countries are setting benchmarks for carbon-aware ad-tech, incorporating lifecycle emissions metrics into their buying algorithms. Collectively, these dynamics underscore the geographically heterogeneous yet interconnected landscape of the Europe Programmatic Advertising market.

Competitive Landscape

Market power is concentrated among a handful of global platforms, yet regional specialists introduce competitive tension through privacy-centric and omnichannel innovations. Google’s and Meta’s extensive logged-in user graphs deliver scale, but their walled-garden stance motivates advertisers to diversify spend into the open web. Amazon’s retail data advantages spur both collaboration and competition with European grocers developing their own retail media plays.

Independent supply-path partners target transparency-seeking buyers. Verve Group’s acquisitions of Jun Group and Captify added search-intelligence and demand-side heft, lifting its net revenues to EUR 447 million and sharpening cross-device identity resolution. Mirakl’s purchase of Adspert embeds predictive bidding across more than 400 marketplace brands, establishing a commerce-oriented differentiation. SSPs embed carbon calculators to attract sustainability-minded clients, while clean-room providers forge alliances with broadcasters to activate first-party data without raw-data transfers. This mosaic fosters healthy rivalry within the Europe Programmatic Advertising market, preserving choice while raising benchmarks for accountability and innovation.

Europe Programmatic Advertising Industry Leaders

-

Yieldbird Sp. z o.o.

-

Amobee, Inc.

-

MediaMath, Inc.

-

Adform A/S

-

The ADEX GmbH

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- September 2025: Verve Group SE purchased Captify for EUR 25.6 million, securing one of the world’s largest onsite search datasets and strengthening its demand-side footprint.

- February 2025: Outbrain closed its USD 900 million acquisition of Teads, creating a combined open-internet platform expected to manage USD 1.7 billion in annual ad spend and unlock USD 65-75 million in cost synergies by 2026.

- December 2024: Mirakl acquired German Ad-Tech startup Adspert to embed AI-driven bid optimization across its retail-media suite.

- June 2024: Verve Group acquired Jun Group for EUR 170 million, adding 230+ Fortune 500 advertisers and boosting pro-forma revenue to EUR 447 million.

Europe Programmatic Advertising Market Report Scope

Programmatic Advertising is the utilization of software to buy digital advertising. This automation makes transactions efficient and more effective, streamlining the process and consolidating your digital advertising efforts in one technology platform.

Europe Programmatic Advertisement Market is segmented By Trading Platform (Real Time Bidding, Private Marketplace Guaranteed, Automated Guaranteed and Unreserved Fixed-rate), By Advertising Media (Digital Display and Mobile Display) and By Enterprise size (SMB's and Large Enterprises). The scope of the study tracks the imact of covid-19 on the studied market.

By Trading Platform

| Real-Time Bidding (Open Auction) |

| Private Marketplace (PMP) |

| Programmatic Guaranteed |

| Preferred Deal (Unreserved Fixed-Rate) |

By Advertising Media

| Display Banner |

| Online Video and CTV |

| Mobile In-App |

| Audio |

| Digital Out-of-Home (DOOH) |

By Enterprise Size

| Small and Medium-Sized Enterprises (SMEs) |

| Large Enterprises |

By Industry Vertical

| Retail and E-Commerce |

| Consumer Packaged Goods (CPG) |

| Automotive |

| Financial Services |

| Media and Entertainment |

| Travel and Hospitality |

| Healthcare and Pharmaceuticals |

| Technology and Telecommunications |

| Government and Public Sector |

By Geography

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Poland |

| Rest of Europe |

| By Trading Platform | Real-Time Bidding (Open Auction) |

| Private Marketplace (PMP) | |

| Programmatic Guaranteed | |

| Preferred Deal (Unreserved Fixed-Rate) | |

| By Advertising Media | Display Banner |

| Online Video and CTV | |

| Mobile In-App | |

| Audio | |

| Digital Out-of-Home (DOOH) | |

| By Enterprise Size | Small and Medium-Sized Enterprises (SMEs) |

| Large Enterprises | |

| By Industry Vertical | Retail and E-Commerce |

| Consumer Packaged Goods (CPG) | |

| Automotive | |

| Financial Services | |

| Media and Entertainment | |

| Travel and Hospitality | |

| Healthcare and Pharmaceuticals | |

| Technology and Telecommunications | |

| Government and Public Sector | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is Europe’s programmatic ad spend today?

Europe Programmatic Advertising market size reached USD 108.23 billion in 2025 and is projected to hit USD 153.36 billion by 2030.

Which media channel leads automated buying?

CTV and online video jointly captured 37.63% of spend in 2024, the largest share among trading media.

What is driving the fastest growth in the next five years?

Programmatic guaranteed deals and digital out-of-home are forecast to post CAGRs of 8.45% and 8.33%, respectively, through 2030.

How do privacy regulations affect strategy?

GDPR and ePrivacy limit third-party cookies, prompting publishers and advertisers to rely on first-party and contextual data assets within consent frameworks.

Are SMEs adopting programmatic at scale?

Yes, automated self-serve platforms and AI optimization tools support an 8.76% CAGR for SME spending between 2025-2030.

Page last updated on: