Europe English Language Teaching Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

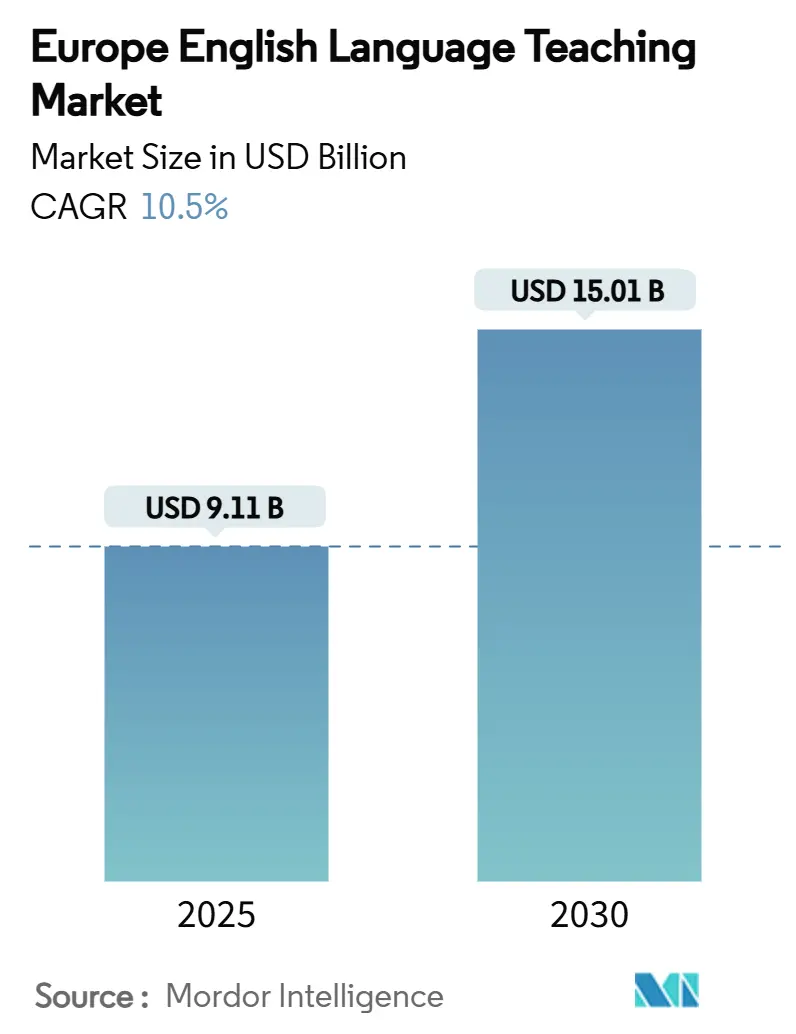

| Market Size (2025) | USD 9.11 Billion |

| Market Size (2030) | USD 15.01 Billion |

| Growth Rate (2025 - 2030) | 10.50% CAGR |

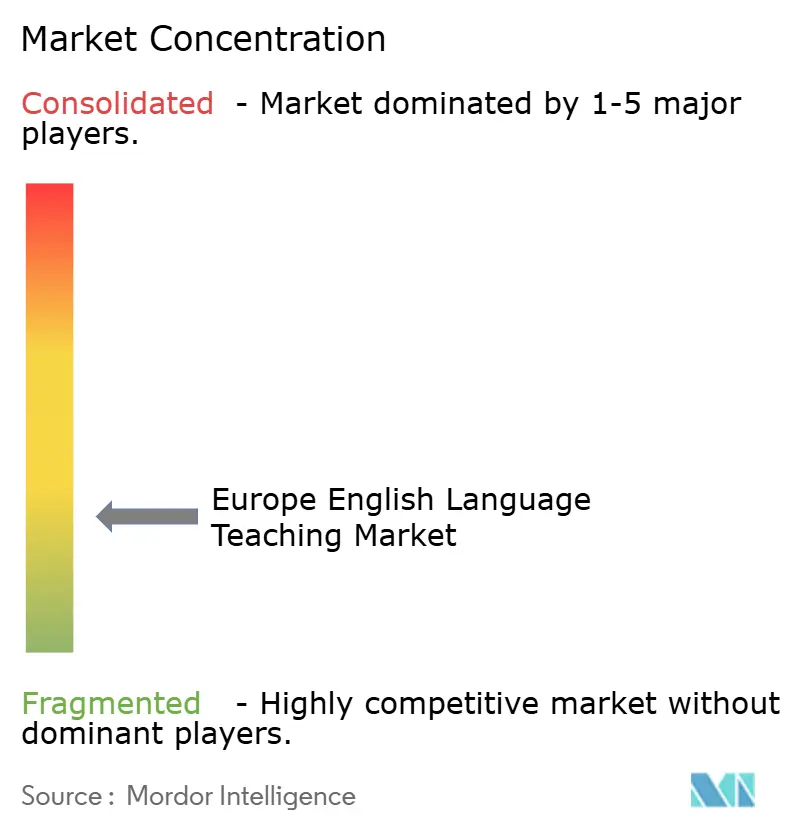

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe English Language Teaching Market Analysis by Mordor Intelligence

The European english language teaching market size stands at USD 9.11 billion in 2025 and is forecast to expand to USD 15.01 billion by 2030 on a steady 10.5% CAGR. The upside stems from EU-level funding that embeds English in every digital-education initiative, corporate upskilling tied to labor-mobility rules, and the rapid diffusion of artificial-intelligence courseware.[1]European Commission, “Digital Education Action Plan 2021-2027,” europa.eu EdTech partnerships with schools are shortening content-refresh cycles and compressing delivery costs, while inbound student flows keep institutional demand elevated despite Brexit-related visa frictions. Providers that combine curriculum alignment with CEFR and data-driven personalization are moving fastest to secure public procurement contracts.

Key Report Takeaways

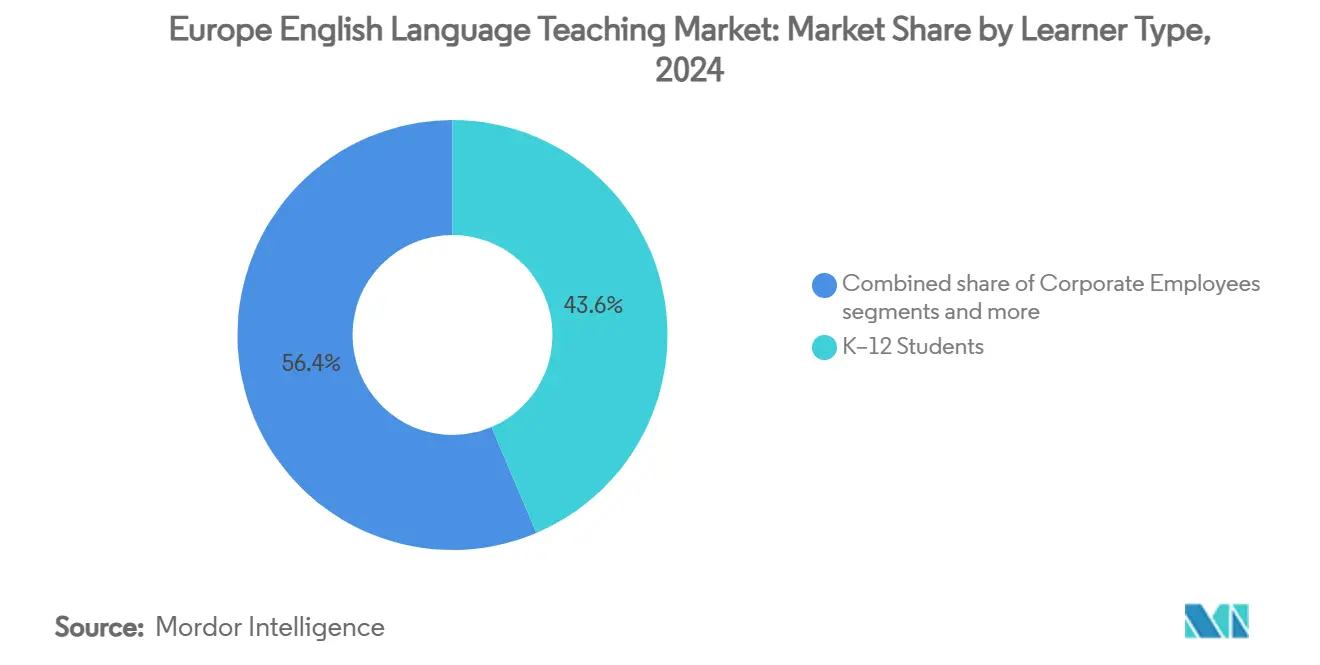

- By learner type, K-12 students held 43.61% of the Europe english language teaching market share in 2024, whereas corporate employees are on track for the highest 11.32% CAGR through 2030.

- By product type, coursebooks and print materials commanded 49.12% of the Europe english language teaching market size in 2024; digital courseware and apps are projected to rise at a 12.41% CAGR between 2025-2030.

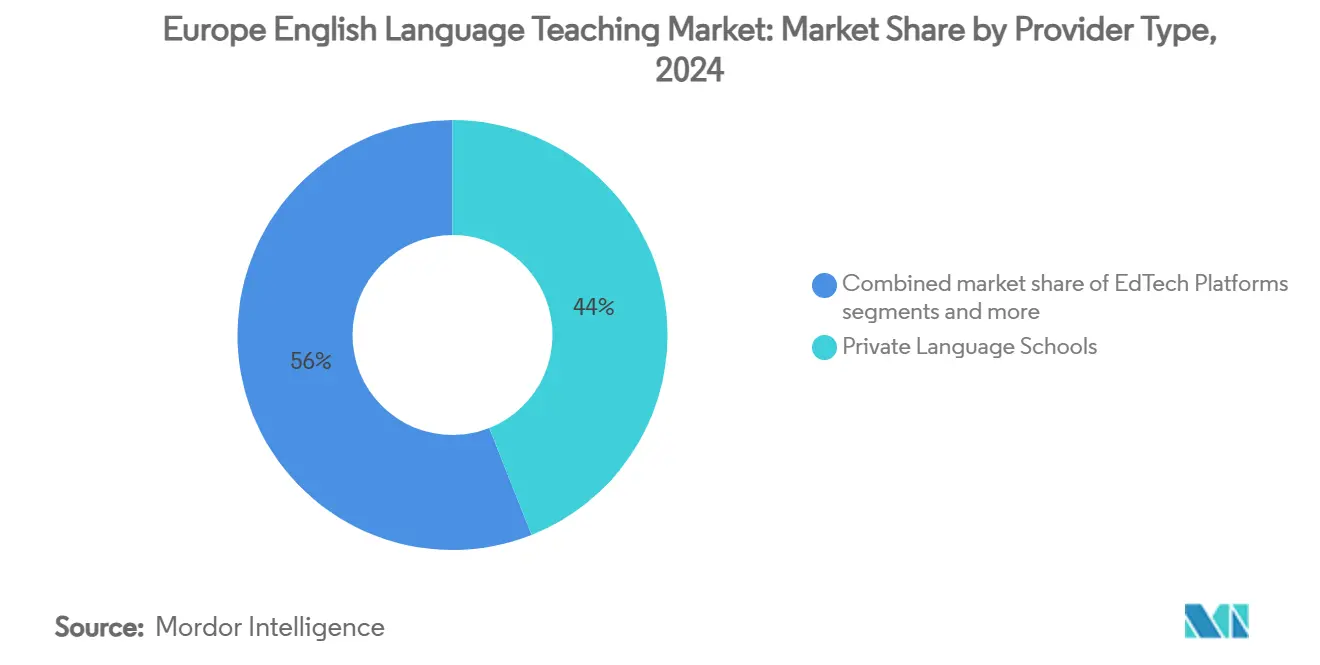

- By provider type, private language schools represented 44% revenue share in 2024, while EdTech platforms are advancing at a 13.10% CAGR to 2030.

- By geography, the United Kingdom led with a 26% revenue share in 2024, whereas Poland is forecast to grow the fastest at 12.56% CAGR to 2030.

Europe English Language Teaching Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising inbound student mobility to Europe | +2.1% | UK, Germany, France, Netherlands | Medium term (2–4 years) |

| Mandatory English curricula in K–12 across the EU | +1.8% | EU-wide (strongest in Eastern Europe) | Long term (≥ 4 years) |

| Corporate upskilling for intra-EU labor mobility | +2.3% | Germany, Netherlands, France, Nordics | Short term (≤ 2 years) |

| EUR 28.4 billion Erasmus+ budget | +1.4% | EU-wide (major university hubs) | Medium term (2–4 years) |

| AI voice-tutoring lowering micro-school costs | +1.7% | UK, Germany, Nordics | Short term (≤ 2 years) |

| EU Digital Education Action Plan procurement incentives | +1.2% | Digitally advanced EU regions | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Inbound Student Mobility to Europe

European universities pitch themselves as cost-effective alternatives to traditional Anglophone destinations, and liberal youth-mobility schemes restore exchange channels curtailed after Brexit. Germany’s relaxed work-study rules let international students log 140 full workdays annually, enlarging the pipeline for pre-arrival English instruction. The United Kingdom’s proposed UK-EU Youth Mobility Scheme extends two-year residency rights to participants aged 18-30, rekindling bilateral flows. Poland’s universities, buoyed by Ukrainian refugee enrollment, roll out English-medium programs that extend beyond Warsaw to Kraków and Wrocław. Demand is shifting from retail consumers toward university-brokered contracts that bundle pre-departure courses and on-campus academic-English support services, solidifying multi-year revenue visibility for aligned providers.

Mandatory English Curricula in K-12 Across the EU

All 27 EU members require English as the first foreign language, and many eastern states start formal instruction in grade 1. Ministries procure turnkey courseware that maps directly to CEFR levels, giving established publishers predictable volume commitments. The curriculum mandate smooths demand across economic cycles, yet demographic decline prompts consolidation of smaller schools, favoring suppliers with nationwide reach. Governments also bake digital-competence modules into language instruction, expanding addressable spend for EdTech vendors that can offer integrated analytics dashboards.

Corporate Upskilling for Intra-EU Labor Mobility

Remote work has normalised cross-border hiring, leaving English as the default operating language inside multinational teams. German automakers, Dutch fintech firms, and French pharma groups now pre-fund business-English boot camps as part of onboarding. Return-on-investment metrics such as project-cycle velocity and error-reduction rates underpin renewed training budgets, shielding the segment from household spending volatility. Customised sector vocabulary and industry-specific simulations help premium providers defend pricing at a time when consumer-facing courses are commoditising.

AI Voice-Tutoring Lowering Operating Costs of Micro-Schools

Voice-first tutoring engines automate pronunciation feedback and enable always-on conversational practice, slicing instructor labour down to periodic coaching. Micro-schools combine rented co-working rooms with AI tutors to undercut legacy language centres by 25% on tuition, expanding access for lower-income adults in Southern Europe. Providers emphasise hybrid models that keep human mentors for cultural nuance and soft-skill development, thereby maintaining perceived instructional quality while achieving cost savings.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining birth rate shrinking K–12 cohort | -1.9% | EU-wide (acute in Southern & Eastern Europe) | Long term (≥ 4 years) |

| Visa tightening for non-EU fee-paying learners | -1.4% | UK, with spillover across the Schengen Zone | Short term (≤ 2 years) |

| AI-generated bilingual content reduces formal ELT need | -1.1% | Tech-advanced regions | Medium term (2–4 years) |

| Private ELT prices are rising above wage growth | -0.8% | Southern Europe, UK | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Declining Birth-Rate Shrinking K-12 Cohort

EU births fell to 3.88 million in 2022 from 6.4 million in 1964, translating to smaller class sizes and under-utilised school infrastructure in Spain, Italy, and parts of Eastern Europe[2]Bruegel, “Europe’s Demographic Challenge,” bruegel.org. Providers dependent on textbook volume face revenue compression, and teacher redeployment toward adult-education programmes accelerates. Policymakers promote lifelong-learning vouchers to offset classroom closures, but market momentum shifts to corporate and senior-citizen segments.

Visa Tightening for Non-EU Fee-Paying Learners

The United Kingdom’s January 2024 rule barring most dependents of international students is forecast to curtail enrolment by 140,000 heads[3]GOV.UK, “New Rules on International Student Dependants,” gov.uk. Fee-paying English-preparation courses once clustered around London and Oxford face enrolment dips and are racing to build online campuses that serve students still offshore. Competing destinations such as Germany and the Netherlands loosen work-hour caps, recapturing part of the displaced demand but leaving total regional volumes subdued in the short run.

Segment Analysis

By Learner Type: Corporate Demand Outpaces K-12 Stability

Europe English Language Teaching market size for K-12 learners held USD 3.97 billion in 2024, equal to 43.61% of overall revenue, yet its expansion slows as EU demographics contract. Corporates generated USD 1.98 billion and are growing the Europe English Language Teaching market by an 11.32% CAGR, fueled by cross-border projects and M&A integration timelines.

Corporate budgets remain resilient because language proficiency is tied to risk-mitigation metrics such as regulatory misfilings and customer-service errors. Vendor invoices are usually absorbed within broader talent-development lines, shielding them from household spending cycles that weigh on evening courses for teenagers. With hybrid work becoming permanent, corporate HR departments demand dashboards that quantify speaking-fluency gains against project KPIs, giving data-ready EdTech firms a procurement edge.

Note: Segment shares of all individual segments available upon report purchase

By Product Type: Digital Courseware Captures Growth Premium

Coursebooks retained 49.12% of 2024 revenue, but their share of the European English Language Teaching market is projected to decline 7 percentage points by 2030 as schools migrate to subscription models. Digital courseware already contributes USD 1.14 billion and is on track for a 12.41% CAGR, reflecting procurement preferences in EU Digital-Education tenders.

AI-driven authoring tools cut lesson-development cycles from six months to six weeks, letting publishers refresh idiom sections and current-events case studies in real time. Licensing frameworks with annual per-student fees replace one-off textbook sales, smoothing revenue trajectories and opening analytics-upsell paths. Assessment plug-ins inside the same ecosystem auto-generate CEFR-aligned progress reports, reducing test-administration workloads for over-stretched teachers.

By Provider Type: Platforms Erode Brick-and-Mortar Advantage

Private language schools owned 44% of Europe english language teaching market share in 2024, due to legacy networks concentrated in the UK, Spain, and Italy. Their margin, however, compresses as EdTech platforms scale at a 13.10% CAGR, offering freemium entry points that convert to paid tiers through AI-driven personalization.

Brick-and-mortar chains counter with blended models that pair weekend workshops with platform homework, yet rising rents and compliance costs narrow their maneuvering room. Platforms, conversely, acquire cohorts at marginal costs near zero, then upsell certificates accepted by multinational employers, thereby absorbing premium positioning once dominated by universities.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

The United Kingdom delivered USD 2.37 billion of revenue in 2024, equal to 26% of the Europe English Language Teaching market. Domestic enrolments remain steady while overseas inflows wobble under visa constraints, prompting schools to roll out virtual reality classrooms funded by regional levelling-up grants. Germany ranks second by spend, propelled by bundled English-plus-coding boot camps that satisfy Mittelstand export ambitions and open residency routes for high-skill migrants.

Poland’s Europe English Language Teaching market size is smaller at present, but it accelerates at a 12.56% CAGR, attracting Ukrainians seeking EU-recognized English credentials and EU students priced out of Western capitals. France leverages its Erasmus+ intake to maintain scale in academic-English segments and experiments with bilingual degree tracks to further lift demand.

Nordic markets, though numerically modest, achieve some of the highest per-capita spends as corporates require near-native fluency for customer-support outsourcing. Southern Europe fights price sensitivity; providers there pivot to micro-credential bundles affordable via monthly instalments, sustaining participation despite wage stagnation.

Competitive Landscape

The European English Language Teaching market remains fragmented, leaving ample headroom for M&A. Large publishers such as Pearson and Oxford University Press accelerate software-as-a-service pivots by embedding adaptive-learning engines inside flagship series. The British Council continues to influence standards, yet budget pressures have it outsourcing ancillary services and renegotiating teacher contracts.

Technology-native entrants scale through viral marketing: freemium apps employ machine-learning to recommend daily micro-lessons, feeding premium tiers that offer proctored assessments recognised by corporate HR. Private-equity interest rises—Veritas Capital’s plan to merge Cambium with Houghton Mifflin Harcourt would create a K-12 content powerhouse with AI-enabled analytics. Larger corporates partner with niche AI-speech specialists to integrate real-time accent feedback into team-collaboration suites.

Labour unions watch the automation trend warily; however, the consensus among educators is that AI will augment rather than eliminate teaching roles. Classroom instructors increasingly become learning-experience designers curating multimedia content flows instead of delivering grammar lectures. The new competitive frontier thus rests on orchestrating human expertise and algorithmic scale rather than choosing between them.

Europe English Language Teaching Industry Leaders

-

British Council

-

Pearson plc

-

EF Education First

-

Cambridge University Press & Assessment

-

Berlitz Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The UK-EU Youth Mobility Scheme gained preliminary approval, granting 18-30-year-olds two-year work-and-study permits across borders, boosting exchange-linked ELT demand.

- April 2025: Duolingo rolled out 148 new AI-generated language courses, doubling its portfolio while reporting a 10% contractor redeployment to machine-authoring oversight roles.

- March 2025: Veritas Capital unveiled plans to merge Cambium Learning with Houghton Mifflin Harcourt, signaling large-scale content-tech consolidation.

- February 2025: EF Education First partnered with Tour de France and Tour de France Femmes avec Zwift for 2025-2026, embedding language-immersion programs into sports-event hospitality packages.

Europe English Language Teaching Market Report Scope

| K-12 Students |

| Higher-Education Students |

| Corporate Employees |

| Coursebooks & Print Materials |

| Digital Courseware & Apps |

| Tutoring & Test-Prep Services |

| Assessment & Certification Services |

| Private Language Schools |

| EdTech Platforms |

| Higher-Education Institutions |

| Corporate Training Providers |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Sweden |

| Poland |

| Russia |

| Rest of Europe |

| By Learner Type | K-12 Students |

| Higher-Education Students | |

| Corporate Employees | |

| By Product Type | Coursebooks & Print Materials |

| Digital Courseware & Apps | |

| Tutoring & Test-Prep Services | |

| Assessment & Certification Services | |

| By Provider Type | Private Language Schools |

| EdTech Platforms | |

| Higher-Education Institutions | |

| Corporate Training Providers | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe English Language Teaching market in 2025?

The Europe English Language Teaching market size is USD 9.11 billion in 2025 and is forecast to reach USD 15.01 billion by 2030.

Which learner segment is expanding the fastest?

Corporate employees lead growth with an 11.32% CAGR through 2030, driven by cross-border work requirements.

Why is Poland considered a high-growth market?

Poland combines favourable visa policies with rising refugee and student inflows, giving it a 12.56% CAGR outlook through 2030.

What product category is gaining share most rapidly?

Digital courseware and mobile apps are growing at a 12.41% CAGR as EU funding preferences tilt toward online solutions.

How are AI tools affecting provider strategies?

AI voice-tutoring and automated content authoring lower delivery costs, enabling EdTech platforms to scale faster than traditional schools.

What risk does demographic decline pose?

Falling birth rates shrink the K-12 cohort, cutting textbook volumes and forcing providers to pivot toward adult and corporate segments.

Page last updated on: