Global Endodontics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

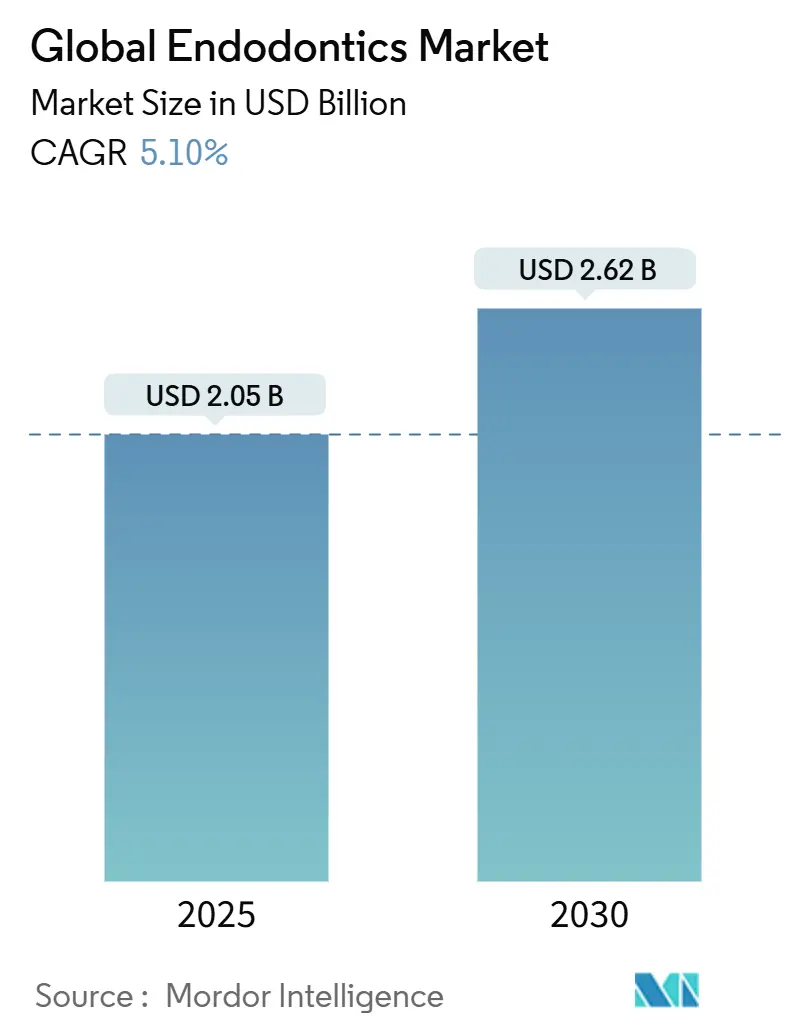

| Market Size (2025) | USD 2.05 Billion |

| Market Size (2030) | USD 2.62 Billion |

| Growth Rate (2025 - 2030) | 5.10% CAGR |

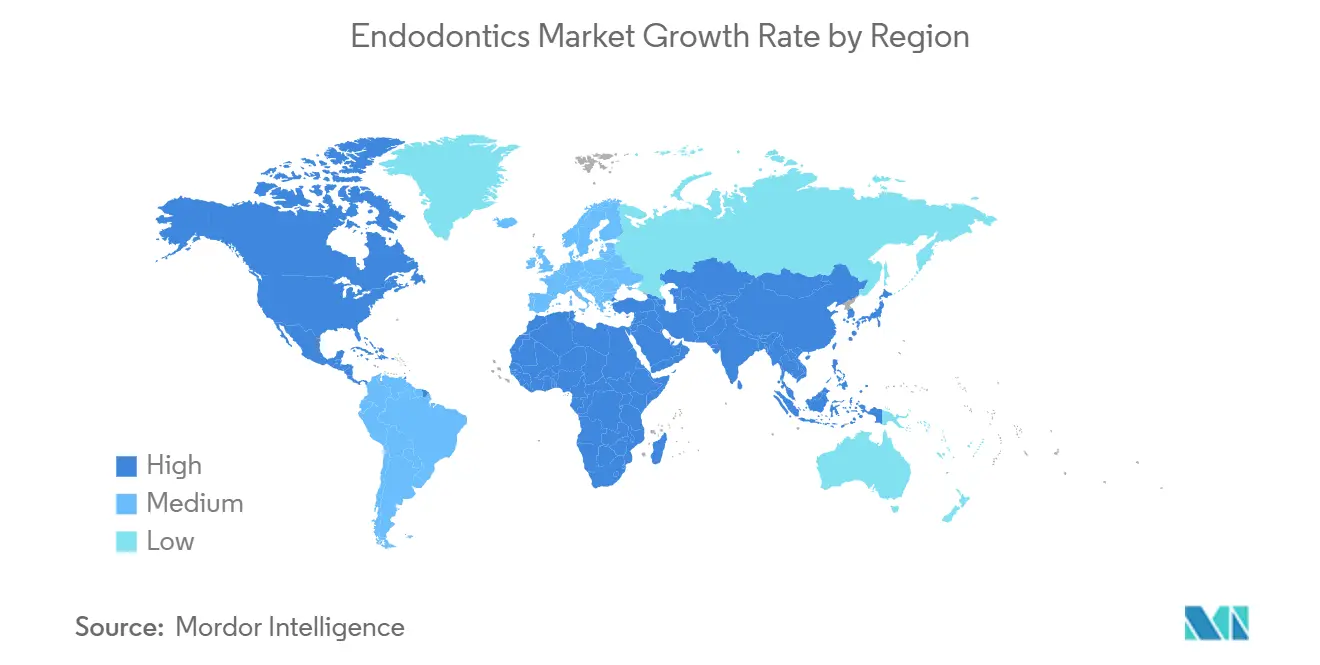

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Global Endodontics Market Analysis by Mordor Intelligence

The Global Endodontics Market size is estimated at USD 2.05 billion in 2025, and is expected to reach USD 2.62 billion by 2030, at a CAGR of 5.10% during the forecast period (2025-2030).

Growth stems from the high prevalence of periodontal disease, wider acceptance of minimally invasive techniques, and steady gains in disposable income that support elective dental care. Technological progress—especially real-time navigation and ultrasonic irrigation—raises procedural success and shortens chair time, making complex treatments more accessible. Aging populations in developed economies keep demand elevated because tooth preservation is now preferred over extraction. Meanwhile, emerging economies are investing in digital dentistry, accelerating equipment turnover and consumables usage. Competitive intensity is moderate, with established brands leaning on regulatory expertise while younger entrants differentiate through niche software-hardware bundles.

Key Report Takeaways

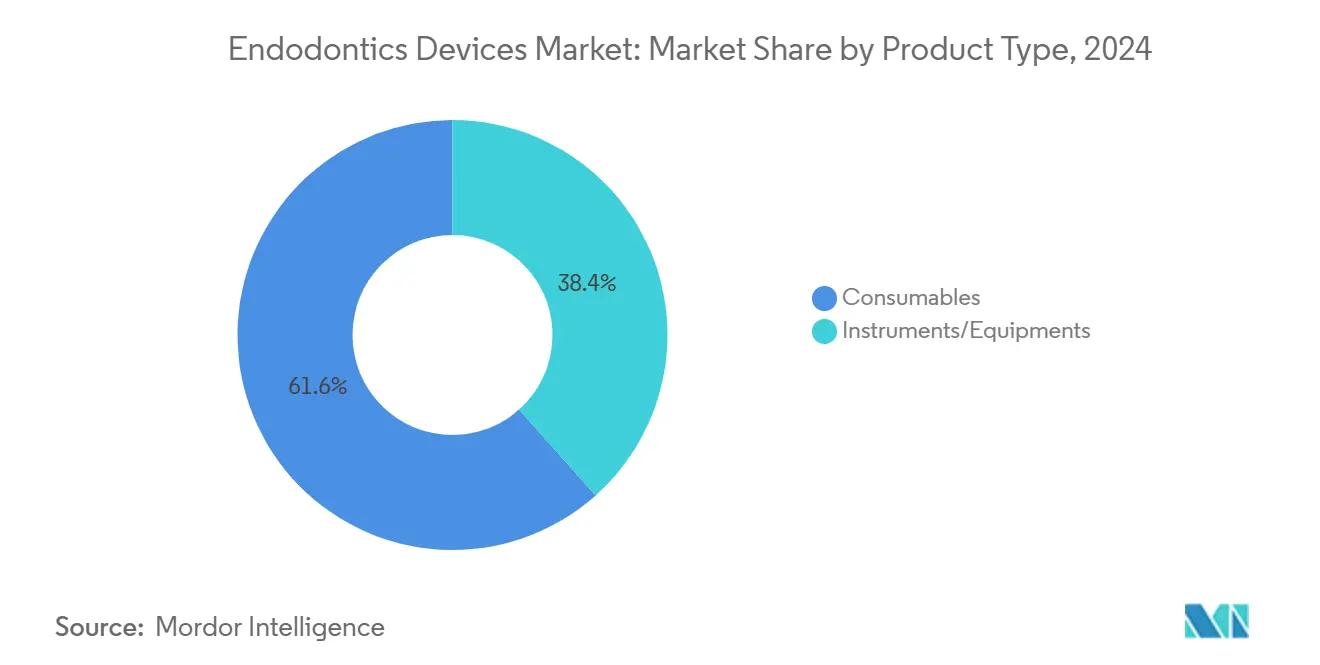

- By product type, consumables led with 61.60% revenue share in 2024, whereas instruments and equipment are projected to register a 5.90% CAGR through 2030.

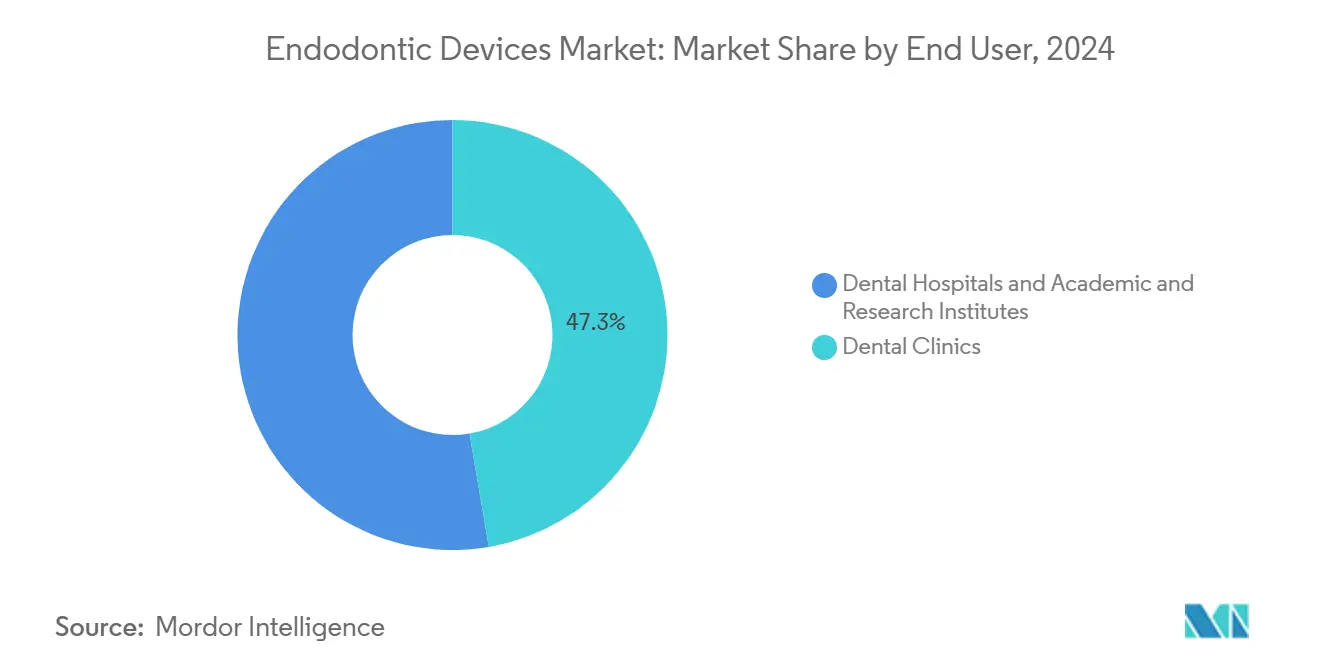

- • By end user, dental clinics commanded 47.30% of the endodontic device market share in 2024, while dental hospitals are expected to expand at 5.67% CAGR to 2030.

- • By region, North America held 41.71% of 2024 revenue; Asia-Pacific is forecast to accelerate at a 6.35% CAGR between 2025-2030.

Global Endodontics Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing incidence of periodontal diseases and rising geriatric population | 1.40% | Global | Long term (≥ 4 years) |

| Technological advancements in endodontic therapy | 1.20% | North America, Europe | Medium term (2-4 years) |

| Rise in awareness towards oral hygiene and growing dental tourism | 1.00% | Asia-Pacific, Latin America | Short term (≤ 2 years) |

| Shift toward minimally invasive endodontics | 0.80% | Global | Long term (≥ 4 years) |

| Dental tourism driving premium endodontic procedure volumes in Mexico, Turkey & Thailand | 0.70% | Mexico, Turkey, Thailand | Short term (≤ 2 years) |

| Reimbursement expansion for root canal therapy under China’s NHSA pilot | 0.60% | China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Periodontal Disease and the Aging Population

CDC surveillance shows that 42% of U.S. adults aged 30 and above present with periodontitis, and prevalence rises to 60% among those aged 65 and older [1]Source: Centers for Disease Control and Prevention, “Gum Disease Facts,” cdc.gov. Smokers and people with diabetes display even higher rates, underscoring a steady, demographically anchored patient pool. As oral-health awareness improves, clinicians emphasize tooth retention, and root-canal volume grows in tandem. The trend shapes procurement choices toward efficient obturation systems and single-use files, bolstering the endodontic device market.

Technological Advancements in Endodontic Therapy

Recent FDA clearances for navigated treatment systems exemplify the shift toward computer-assisted endodontics. Devices such as Navident EVO allow real-time tracking of file position inside canals, enhancing precision and reducing procedural missteps. Ultrasonic irrigant activation, validated by peer-reviewed evidence, improves debridement efficiency without lengthening chair time. In aggregate, these technologies expand the endodontic device market by attracting general practitioners who previously referred complex cases.

Rise in Awareness Toward Oral Hygiene and Dental Tourism

Cross-border care is drawing patients to Thailand, Mexico, and Turkey for cost-effective endodontic work. Competitive pricing pushes local clinics to adopt standardized protocols and portable motor-file systems that function reliably in diverse settings. Although complications occasionally surface, heightened scrutiny encourages suppliers to invest in devices with traceable sterilization and global service footprints, reinforcing confidence among traveling patients and practitioners.

Shift Toward Minimally Invasive Endodontics

Minimally invasive endodontics preserves peri-cervical dentin, boosting long-term tooth strength. Cone-beam CT imaging coupled with slender nickel-titanium instrumentation allows access cavities that conserve up to 40% more tooth structure than legacy approaches. Studies demonstrate improved fracture resistance, prompting educational bodies to revise curricula and accelerating demand for flexible, torque-controlled motors. The cumulative effect widens the endodontic device market size for advanced instrumentation and single-patient obturation kits.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Side effects and risks associated with endodontic treatment | -0.80% | Global | Short term (≤ 2 years) |

| Stringent regulatory policies for the approval of products | -1.10% | North America, Europe | Medium term (2-4 years) |

| Limited insurance coverage for retreatment and 3-D imaging reducing patient uptake | -0.70% | Global | Medium term (2-4 years) |

| High capital cost of CBCT & laser-assisted systems for small clinics | -0.60% | Emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Policies for the Approval of Products

The FDA’s current guidance stipulates that 510(k) submissions for endodontic devices demonstrate substantial equivalence through granular mechanical-property datasets and, increasingly, human-factors validations. Sponsors introducing novel features—such as dynamic navigation or adaptive reciprocation—often confront additional clinical-evidence requirements that elongate timelines and inflate development budgets.

A latent effect of this expanded evidentiary bar is the emergence of strategic partnerships between device manufacturers and university hospitals. By embedding trial protocols into residency programs, companies can generate regulatory-grade data while seeding product familiarity among tomorrow’s key opinion leaders. Industry observers note that these alliances also serve as de-risking tools for venture investors, who view early FDA feedback as a predictor of international market clearances.

Side Effects and Risks Associated with Endodontic Treatment

The FDA’s release of 5.8 million historical device reports revealed 2.1 million dental-implant complaints dominated by osseointegration failures. Although root-canal tools represent a fraction of these events, heightened vigilance influences purchasing habits. Clinicians increasingly favor biocompatible obturation materials and single-patient files to mitigate infection risk, slightly tempering short-term purchase cycles as they vet suppliers.

Segment Analysis

The consumables segment captured 61.60% of 2024 revenue, underlining the repetitive nature of files, sealers, and irrigation solutions. Each root-canal visit consumes a full set of single-use items, ensuring a dependable reorder rhythm that anchors the endodontic device market size for disposable products. Digital obturation guns and thermoplastic carriers further boost unit volumes as practitioners migrate from traditional hand-pluggers. Instruments and equipment, although representing a smaller revenue base, are projected to post the fastest 5.90% CAGR because cone-beam guidance, torque-controlled motors, and apex locators shorten chair time, thereby improving practice throughput. Integration with chair-side imaging enables real-time length verification, lowering retreatment rates and generating return on investment within two years. The emphasis on ergonomic handpieces and low-vibration ultrasonic units supports premium pricing while maintaining upgrade cycles.

The mid-term outlook indicates that improved nickel-titanium metallurgy will sustain demand for heat-treated file systems capable of navigating calcified canals. Simultaneously, open-platform obturation machines that sync with practice-management software are emerging as a differentiator. Suppliers that bundle software licenses with hardware upgrades gain recurring revenue while simplifying calibration compliance. Price sensitivity may rise in developing economies, but tiered portfolios offer entry-level options that lock in brand loyalty for amortized replacements. Collectively, these trends reinforce the ascendancy of both disposable and capital-equipment segments within the endodontic device market.

Note: Segment shares of all individual segments available upon report purchase

By End User: Clinics Lead, Hospitals Accelerate

Dental clinics accounted for 47.30% of 2024 demand, underscoring their role as primary sites for routine root-canal therapy. The setting benefits from high patient throughput, flexible scheduling, and owner-operator decision-making, which accelerates equipment turnover and consumables usage. Chair-side ultrasonic devices that hook directly into existing delivery systems have found rapid uptake among private practitioners. Nevertheless, dental hospitals are projected to grow at a 5.67% CAGR as they manage complex retreatment cases, medically compromised patients, and trauma-related injuries. Hospital procurement departments increasingly negotiate multi-year supply contracts, driving volume discounts that favor integrated device ecosystems.

Academic centers, although a smaller slice of the endodontic device market share, play a catalytic role in evidence generation. Trials on new thermal obturation techniques and bioceramic sealers originate in teaching hospitals, influencing guidelines that later ripple into private practice. As universities upgrade simulation labs, advanced rotaries and virtual reality training units enter the purchasing mix, reinforcing early-career brand exposure. This multichannel demand matrix keeps the endodontic device industry nimble, with marketing strategies tailored to each venue’s unique workflow.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America retained 41.71% of 2024 revenue, strengthened by robust dental insurance coverage and early adoption of digital solutions. CDC data confirm that 46% of U.S. adults aged 30 and older experience periodontitis. Productivity losses equate to USD 46 billion annually through school and work interruptions, incentivizing insurers to reimburse efficient treatments. The United States accounts for most regional sales of cone-beam navigation units, and Canada follows closely in adopting bioceramic sealers. Market leaders invest in clinical-education hubs to showcase new file geometries, reinforcing premium-brand segmentation within the endodontic device market.

Asia-Pacific is projected to climb at a 6.35% CAGR to 2030, benefiting from rising middle-class income and expanding urban clinics. Government-backed oral-health campaigns in China elevate public awareness, while India’s private dental colleges graduate nearly 30,000 dentists yearly, increasing equipment penetration. Thailand and Vietnam leverage competitive pricing to attract foreign patients, and that tourism network fuels standardized device demand across multiple currencies. Supply chains are localizing nickel-titanium file production to shorten lead times, enabling price-point flexibility that broadens access to the endodontic device market size.

Europe represents a mature yet innovative environment, combining high reimbursement with stringent material safety regulations. Germany leads sales of obturation systems, supported by a dense network of insurance-affiliated practices. The UK’s outbound tourism pressure has prompted domestic clinics to advertise same-day root-canal packages featuring guided access systems and single-visit crowns, mitigating leakage of high-value procedures. Eastern European nations, including Poland and Romania, invest in digital imaging to attract medical tourists, carving niches within the broader endodontic device market. EU-wide software standards foster interoperability, easing cross-border device servicing and widening the sales footprint of multinationals.

Competitive Landscape

The endodontic device market is moderately concentrated. Dentsply Sirona leads with a diverse catalog ranging from nickel-titanium files to apex locators and reported USD 3.79 billion in trailing twelve-month revenue for 2024. Kerr Dental strengthens its positioning with ZenFlex One reciprocating files launched in April 2025. ClaroNav differentiates through real-time surgical navigation and obtained FDA clearance for guided endodontics in March 2025 [2]Source: Becker’s Dental, “15 Dental Tech Innovations from 2024,” beckersdental.com. Competitive tactics include portfolio bundling, software-as-a-service platforms, and multi-year service contracts that anchor customer loyalty.

Acquisitions remain common; larger players absorb niche innovators specializing in bioceramic chemistry or AI-driven case planning. Intellectual-property portfolios increasingly integrate firmware to secure aftermarket revenue via file recognition chips that trigger automatic settings on torque-controlled motors. In parallel, cloud analytics partnerships—illustrated by Dentsply Sirona’s collaboration with Google Cloud—leverage anonymized treatment data to refine file design without extending R&D timelines. Regulatory know-how serves as a barrier; firms with seasoned compliance teams accelerate 510(k) submissions, outpacing smaller challengers. Yet, white-space opportunities persist in hypoallergenic obturation carriers and open-architecture imaging APIs. Overall, the competition spectrum balances scale advantages with agile innovation, sustaining a dynamic endodontic device market.

Global Endodontics Industry Leaders

-

Dentsply Sirona

-

Envista (Kerr/SybronEndo)

-

Septodont Holding

-

Coltene Group

-

Brasseler USA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Kerr Dental launched ZenFlex One reciprocating files, positioning the line as a time-saving solution for complex anatomy—a move likely to challenge incumbent heat-treated file systems.

- March 2025: ClaroNav secured FDA clearance to extend Navident EVO’s indication to guided endodontics, reinforcing the march toward navigation-assisted care.

- February 2025: Odne obtained FDA clearance for its Clean debridement device, signaling heightened regulatory openness to novel irrigant-activation technologies.

- October 2024: Kerr Dental introduced OptiBond Universal 360, a bonding agent calibrated for post-endodontic restorations.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the endodontics market as all value generated worldwide from instruments, apex locators, endodontic motors, lasers, handpieces, machine-assisted obturation units, and consumables such as NiTi rotary files, irrigants, gutta-percha, and bioceramic sealers that are deployed solely for primary root-canal therapy, retreatment, or surgical endodontic procedures across clinics, hospitals, and teaching institutes.

Scope exclusion: general dental imaging systems, implants, and orthodontic devices are not counted.

Segmentation Overview

- By Product Type

- Consumables

- Endodontic Burs

- Obturation Materials

- Endodontic Files and Shaper

- Irrigation Solutions & Lubricants

- Instruments / Equipment

- Apex Locator

- Lasers

- Machine Assisted Obturation Systems

- Scalers

- Others

- Consumables

- By End-User

- Dental Clinics

- Dental Hospitals

- Academic & Research Institutes

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle-East and Africa

- GCC

- South Africa

- Rest of Middle-East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We then interviewed practicing endodontists, procurement heads at multi-site dental service organizations, and regional distributors across North America, Europe, Asia-Pacific, and the Gulf to validate unit volumes, average selling prices, NiTi adoption rates, and consumable re-use practices that do not surface in secondary sources.

Desk Research

Mordor analysts first compiled trade and patient-care statistics from sources such as the World Health Organization's oral-health data sets, the American Association of Endodontists, Eurostat treatment discharge files, and national customs records tracking HS codes for dental consumables. Regulatory filings from the FDA and CE mark databases helped us map product clearances by type, while company 10-K statements, investor decks, and clinical-trial registries illustrated revenue splits and pipeline traction. Subscription databases, Dow Jones Factiva for deal news, D&B Hoovers for manufacturer financials, and Questel for patent counts, added competitive and innovation signals. Other publicly available academic journals supplied prevalence ratios and success-rate benchmarks. This list is illustrative; numerous additional publications were reviewed to corroborate figures and fill data gaps.

Market-Sizing & Forecasting

A top-down build used procedure volumes and average material spend per root-canal case, which are reconstructed from public treatment statistics and import values, then cross-checked through sampled ASP × volume roll-ups from key suppliers. Variables such as untreated caries prevalence, dentist-to-population ratios, disposable income growth, and NiTi file penetration inform our model. A multivariate regression projects these drivers to 2030, and selective bottom-up channel checks fine-tune regional totals where public data are thin.

Data Validation & Update Cycle

Outputs pass a two-step analyst review against independent signals, quarterly manufacturer sales, shipment anomalies, and currency swings. Reports refresh every twelve months, with interim updates triggered by major product launches or regulatory shifts; a final pre-publication audit ensures clients receive the latest view.

Why Mordor's Endodontics Baseline Commands Reliability

Published estimates often diverge because firms choose different product baskets, base years, and refresh cadences. Our disciplined scope selection, annual updating, and dual-track validation keep Mordor's numbers steady yet responsive.

Key gap drivers include whether consumables are bundled with broader dental equipment, the use of list instead of blended ASPs, and limited primary interviews that miss real-world re-use or price erosion. We also convert all revenues to USD at the average annual rate, reducing currency noise.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.05 B (2025) | Mordor Intelligence | - |

| USD 2.41 B (2024) | Global Consultancy A | Wider basket includes general dental burs and imaging disposables |

| USD 1.86 B (2024) | Research Publisher B | Excludes lasers; relies on list prices without regional discounts |

| USD 1.76 B (2024) | Industry Journal C | Devices only, no consumables; forecast based on historical CAGR extension |

Taken together, the comparison shows that once differing scopes and price assumptions are stripped away, Mordor's baseline offers a balanced midpoint grounded in clear variables, refreshed data, and transparent steps that decision-makers can replicate.

Key Questions Answered in the Report

What is driving the current growth of the endodontic device market?

Chronic periodontal disease, an aging population keen on tooth preservation, and rapid adoption of precision-guided technologies are expanding procedure volumes and device demand.

Which product category generates the highest revenue?

Consumables such as files, sealers, and irrigation solutions account for 61.60% of annual turnover because each root-canal treatment consumes multiple single-use items.

Why are dental hospitals projected to grow faster than clinics?

Hospitals increasingly manage complex retreatment and medically compromised cases, prompting investment in specialized endodontic departments that elevate their 5.67% forecast CAGR.

How do regulatory requirements affect device innovation?

Stringent FDA and EU mandates lengthen development cycles and favor companies with robust compliance teams, which can navigate 510(k) pathways and clinical-evidence demands more efficiently.

What role does dental tourism play in endodontic device adoption?

Cross-border treatment boosts demand for portable, standardized devices in emerging hubs such as Thailand and Mexico, pushing manufacturers to design equipment that performs reliably across diverse clinical settings.

Which regions offer the fastest market expansion opportunities?

Asia-Pacific leads with a projected 6.35% CAGR through 2030, supported by rising income levels, expanding urban dental infrastructure, and growing awareness of oral health.

Page last updated on: