Digital English Language Learning Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

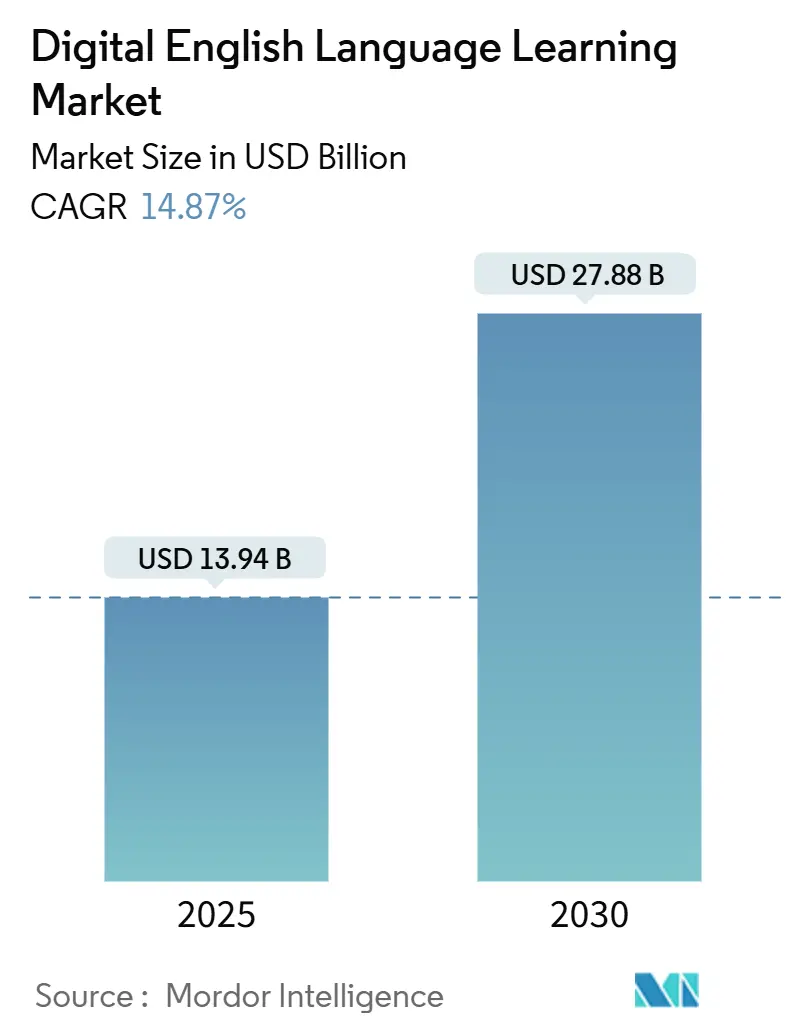

| Market Size (2025) | USD 13.94 Billion |

| Market Size (2030) | USD 27.88 Billion |

| Growth Rate (2025 - 2030) | 14.87% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Digital English Language Learning Market Analysis by Mordor Intelligence

The digital English language learning market size is valued at USD 13.94 billion in 2025 and is forecast to reach USD 27.88 billion by 2030, expanding at a 14.87% CAGR. Behind this growth stands a confluence of smartphone ubiquity, AI-powered personalization, and corporate upskilling programs that elevate English proficiency to a core workplace skill. Government digitalization initiatives in K-12 systems, notably across Asia-Pacific, are institutionalizing online language study, while immersive VR and 5G networks are re-shaping how pronunciation and fluency tools deliver real-time feedback. Cloud infrastructure adoption is unlocking scalable adaptive learning, and freemium business models are widening access in price-sensitive segments, signaling a shift toward accessibility-driven monetization. Competitive momentum remains brisk as incumbents and AI startups contend for share by embedding analytics, speech recognition, and certification utilities into cohesive learning ecosystems.

Key Report Takeaways

- By end user, individual learners accounted for 36.47% share of the digital English language learning market size in 2024 and are advancing at a 16.79% CAGR to 2030.

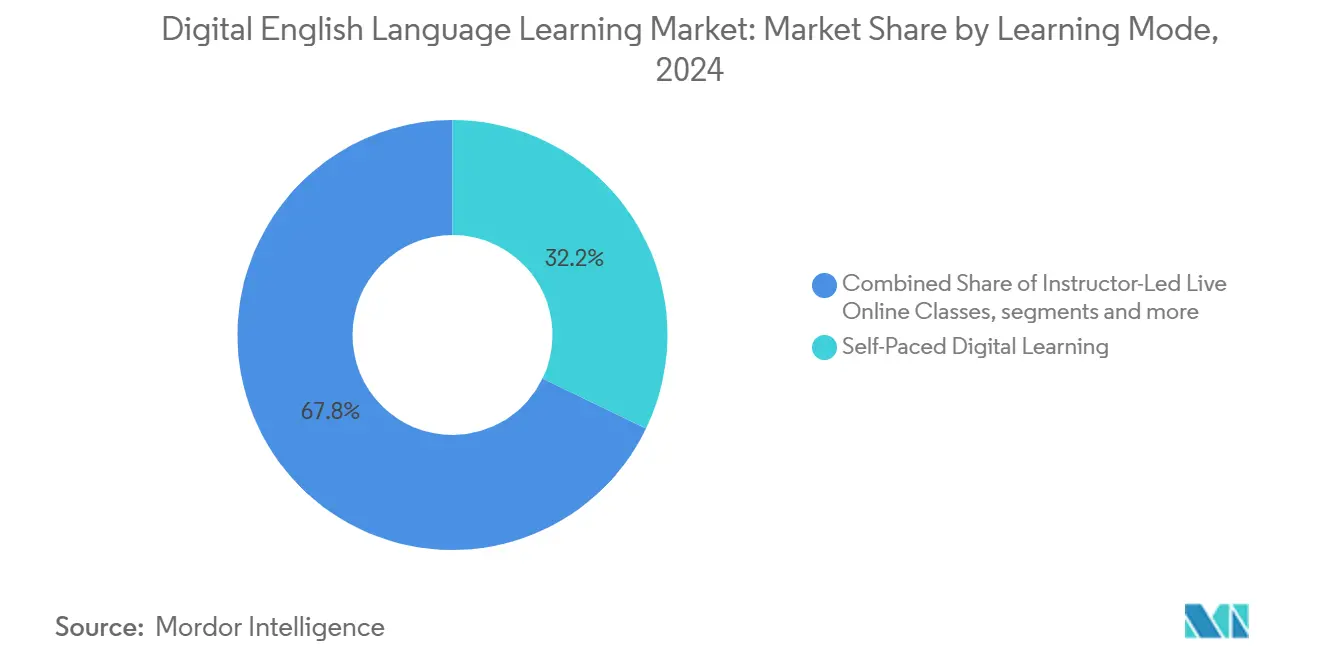

- By learning mode, self-paced formats led with 32.16% revenue share in 2024, while immersive/VR experiences are projected to expand at a 19.58% CAGR through 2030.

- By product type, digital courseware accounted for 27.92% revenue share in 2024, while pronunciation and fluency tools are progressing at a 17.35% CAGR, outpacing other categories.

- By business model, subscription-based accounted for 47.22% share of the market in 2024, while freemium and ad-supported formats are registering the fastest 18.17% CAGR to 2030.

- By geography, Asia-Pacific held 39.45% of the digital english language learning market share in 2024.

Global Digital English Language Learning Market Trends and Insights

Drivers Impact Analysis

| Driver | ( ~ ) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid smartphone & affordable mobile-internet penetration | +2.5% | Global with strongest impact in APAC and MEA | Medium term (2–4 years) |

| Corporate upskilling demand for global business English | +1.8% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Government-led K-12 digitalization initiatives | +1.2% | APAC core, spill-over to MEA and South America | Long term (≥ 4 years) |

| AI-powered personalization improves learner outcomes | +0.9% | Global with early adoption in developed markets | Medium term (2–4 years) |

| Post-pandemic talent-mobility driving certification uptake | +0.7% | Global, concentrated in urban centers | Short term (≤ 2 years) |

| Telco-edtech zero-rated data bundles expand reach | +0.6% | APAC, MEA, and South America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rapid Smartphone & Affordable Mobile-Internet Penetration

Mobile learning has scaled rapidly, with 94% of Generation Z using phones for study and the broader mobile learning segment on track for USD 77.4 billion by 2025 [1]HolonIQ, “AI English Courses Up 2.5×,” holoniq.com. Five-minute micro-lessons consumed during commute windows are replacing classroom constraints, and 5G rollouts are enhancing speech-recognition latency, essential for pronunciation coaching. Enterprises mirror this shift as 67% of US firms deploy mobile learning for staff, embedding English modules in flow-of-work scenarios that demand minimal scheduling friction. The widespread use of smartphones and cheap mobile internet has reduced access barriers, particularly in emerging markets like Southeast Asia, Sub-Saharan Africa, and MENA. This infrastructure boost is enabling asynchronous learning and real-time practice for language acquisition, expanding edtech’s reach beyond traditional classroom contexts.

Corporate Upskilling Demand for Global Business English

Amazon’s pledge to reskill 700,000 employees showcases how large multinationals institutionalize English programs. Earnings studies reveal proficiency can lift wages by up to 80%, a statistic reinforcing ROI-centric investment in specialized business English curricula [2]Pearson Languages, “The Impact of English,” pearson.com. AI conversation coaches now tailor sector vocabulary, and integrations with productivity suites allow seamless launch of lessons directly within workplace platforms, trimming context-switch penalties. As cross-border operations and global remote teams become standard, English fluency is increasingly viewed as a baseline employability skill rather than a competitive edge. This shift is driving enterprises to embed continuous language learning into professional development frameworks, especially in finance, tech, and customer service sectors.

Government-Led K-12 Digitalization Initiatives

South Korea budgeted USD 70 million for AI textbooks in 2025, signaling policy-level support for digital materials across core subjects. Indonesia’s Emancipated Curriculum mandates English from grade 1 by 2027/28, greatly enlarging the public-sector addressable base. Similar initiatives under Estonia’s AI Leap 2025 show how nations position language mastery as a lever for future competitiveness, standardizing demand for cloud-delivered content. These programs are accelerating demand for interactive and adaptive digital tools that support personalized learning at scale, especially in under-resourced rural schools. EdTech firms aligning content to national curricula and local languages are gaining strategic footholds through public-private partnerships and procurement frameworks.

AI-Powered Personalization Improves Learner Outcomes

AI English courses have grown 2.5 times year-on-year, led by Duolingo’s roll-out of video-call drills and auto-generated content. Microsoft’s Speech Pronunciation Assessment and ELSA Speak’s feedback loops personalize pacing, raising test scores by 6% in controlled studies. These systems adapt micro-tasks around user proficiency, shortening time-to-fluency and reducing dropout rates. Adaptive algorithms also identify recurring grammar or pronunciation errors, offering targeted revision modules in real time. AI tutors are increasingly integrated into LMS platforms, enabling school systems and corporations to deploy scalable, data-driven support without expanding teaching staff.

Restraints Impact Analysis

| Restraint | ( ~ ) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent digital divide in low-income cohorts | –1.1% | Rural APAC, MEA, and South America | Long term (≥ 4 years) |

| Free content cannibalization & low willingness to pay | –0.8% | Global, particularly emerging markets | Medium term (2–4 years) |

| Data-privacy regulations raising compliance costs | –0.6% | EU, North America, expanding globally | Short term (≤ 2 years) |

| Algorithmic bias concerns in AI language assessment | –0.4% | Developed markets with strict oversight | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Persistent Digital Divide in Low-Income Cohorts

Connectivity gaps still hinder adoption as rural regions wrestle with device affordability and patchy broadband. The paradox is acute: communities that stand to benefit most from English skills face the steepest access barriers [3]Suzanne Romaine, “Language Equality & Schooling: Global Challenges & Unmet Promises,” amacad.org. Remedies require telcos, NGOs, and edtech firms to co-invest in infrastructure and subsidized devices. Edtech platforms are increasingly experimenting with offline-first models, allowing lesson downloads during brief connectivity windows. In many cases, local educators double as digital access intermediaries, helping students navigate platforms on shared community devices. However, without national policies that prioritize rural digital inclusion, such efforts risk remaining fragmented and unsustainable.

Free Content Cannibalization & Low Willingness to Pay

YouTube tutorials and open resources dilute the perceived value of paid platforms, particularly in markets where disposable income is tight. Providers counteract by bundling certifications, ad-free experiences, and advanced analytics that free options lack. Success hinges on converting free users to premium tiers through clear skill pathways and outcome proof-points. In many emerging markets, cultural norms also influence spending behavior, with free resources often preferred due to skepticism about digital payments. To overcome this, platforms invest in localized marketing and flexible payment models such as micro-subscriptions and pay-as-you-go plans. Educational providers are increasingly collaborating with employers and governments to subsidize costs and demonstrate tangible returns on investment.

Segment Analysis

By Learning Mode: Flexible Self-Paced Formats Anchor Demand

Self-paced digital courses captured 32.16% of the digital English language learning market share in 2024. Their asynchronous design lets adults weave study into fragmented schedules, sustaining dominance. VR-based approaches, though nascent, are scaling at 19.58% CAGR as Meta Quest-enabled classrooms reproduce social immersion. Gamified microlearning fuses bite-sized lessons with leaderboards, elevating completion metrics and supplying steady daily-active-user pipelines. Learners increasingly favor formats that blend entertainment with education, boosting engagement and retention. This shift pushes providers to innovate continuously, integrating social features and adaptive challenges to maintain interest over time.

Immersive modes blur with self-paced models as AI chatbots provide synchronous speaking drills on demand. This convergence signals a future where learning-mode boundaries fade: one application can morph from solo flashcard review to live VR dialogue, retaining users across proficiency milestones. The seamless transition between modes also enhances personalized learning journeys, allowing users to practice in varied contexts without switching platforms. Such fluidity is expected to raise lifetime user value and deepen skill mastery through diversified input.

By End User: Individuals Propel the Upswing

Individuals claimed 36.47% of 2024 revenue and propel the fastest 16.79% CAGR through 2030, underscoring how career mobility incentives move learning budgets from institutions to consumers. Mobile apps with localized payment solutions cater to first-job seekers in India and Brazil, where English unlocks upticks in earnings trajectories. This democratization of language learning empowers underserved populations to access global opportunities with minimal upfront costs. The rise of gig economy jobs further drives demand for flexible, on-the-go language skill acquisition among individuals.

K-12 learners represent a policy-driven cohort as ministries digitize curricula, yet growth rates lag individuals because baseline enrollment is already high in developed economies. Corporate demand remains sturdy as remote work drives need for common lingua franca; vendors bundle reporting dashboards for HR teams to quantify ROI. Education ministries are increasingly investing in blended learning solutions that combine digital and in-person instruction, optimizing classroom outcomes. Meanwhile, corporations prioritize scalable training platforms that support rapid upskilling amid evolving workplace communication demands.

By Product Type: Courseware Remains Core While Pronunciation Accelerates

Digital courseware held a 27.92% share in 2024, anchoring the digital English language learning market with structured pathways. Pronunciation and fluency tools, fueled by advances in speech analytics, scale at 17.35% CAGR to 2030. Enterprises prioritize articulate verbal communication, pushing the adoption of granular accent-reduction modules. The integration of real-time feedback and gamified speech drills makes pronunciation practice more engaging and measurable. This focus responds to employer demands for confident speakers who can navigate global business environments with clarity.

Integrated learning suites combine courseware, AI tutors, and certification trackers under one login, reinforcing user stickiness. Assessment engines adapt question difficulty in real time, a feature PTE Academic and TOEFL upgrades illustrate as they modernize to adaptive formats. Such comprehensive platforms also facilitate continuous learner assessment, enabling personalized pathways that address individual weaknesses. Providers leverage data analytics to refine content and enhance predictive success models, driving higher completion rates.

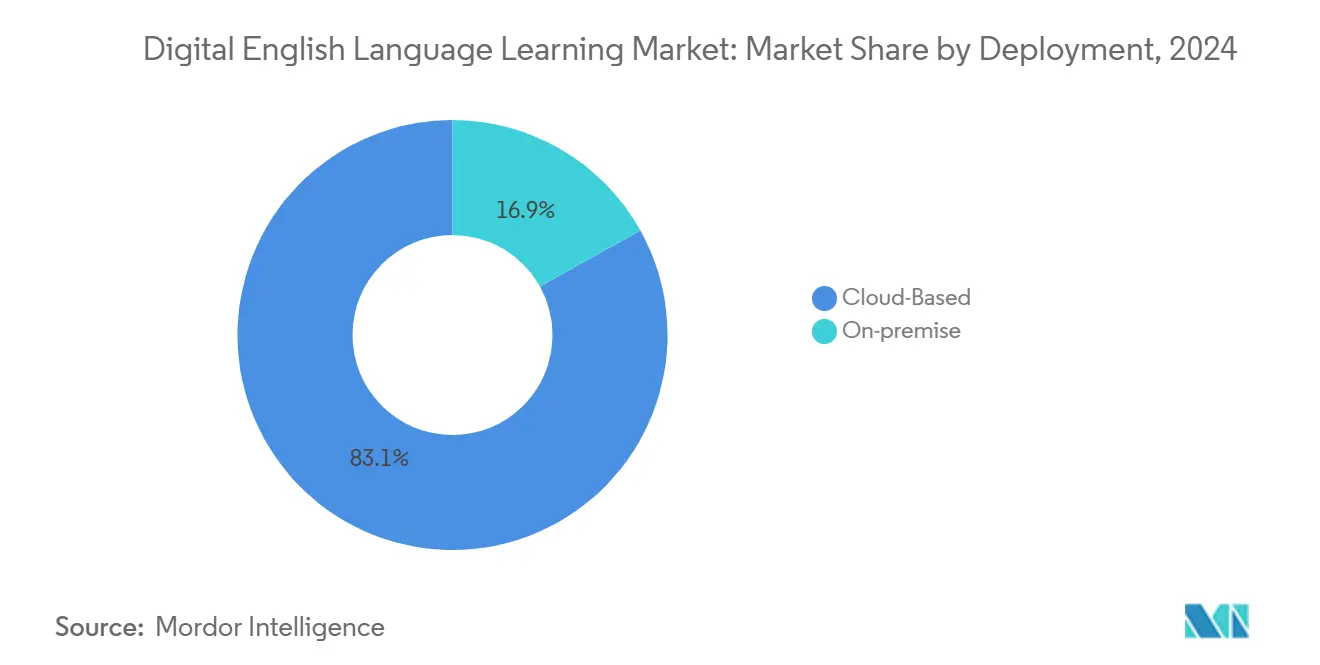

By Deployment: Cloud Architecture Underpins AI Personalization

Cloud solutions owned 83.07% of 2024 revenue and carry the highest 15.67% CAGR because AI models require elastic compute to parse speech and generate dynamic curriculum. Continuous delivery lets vendors launch weekly feature drops without user-side installs. Edge computing complements cloud by processing latency-sensitive pronunciation tasks locally, then syncing progress to central servers. This hybrid approach optimizes user experience by balancing performance and data security, particularly in bandwidth-constrained regions. It also enables rapid innovation cycles, allowing providers to quickly integrate user feedback and emerging AI capabilities.

On-premise persists in sectors with stringent data-sovereignty rules, yet hybrid architectures that encrypt and shard data across local and cloud nodes offer compliance without sacrificing feature velocity. Organizations in healthcare, government, and finance sectors especially demand such tailored deployments to meet regulatory mandates. Vendors respond by customizing solutions that blend centralized intelligence with localized control, enhancing trust and adoption.

By Business Model: Subscription Stability Meets Freemium Reach

Subscriptions commanded a 47.22% share in 2024, delivering predictable cash flows that finance perpetual content refresh. Freemium and ad-supported streams surge at 18.17% CAGR as platforms seek viral growth in lower-income regions. Conversion levers include unlimited review sessions, offline downloads, and certification vouchers. The subscription model supports ongoing learner engagement through regular content updates and community features. Meanwhile, freemium offerings lower barriers to entry, building large user bases that platforms can monetize via upsells and partnerships.

Institutions negotiate volume licensing for thousands of seats, often layering predictive analytics that map employee proficiency gaps to business KPIs. One-time purchases decline as learners favor continuous skill-stacking journeys over static course assets. Enterprise clients increasingly demand integrated reporting and ROI measurement to justify training spend. This drives vendors to develop modular solutions that adapt to changing organizational priorities and workforce skills needs.

Geography Analysis

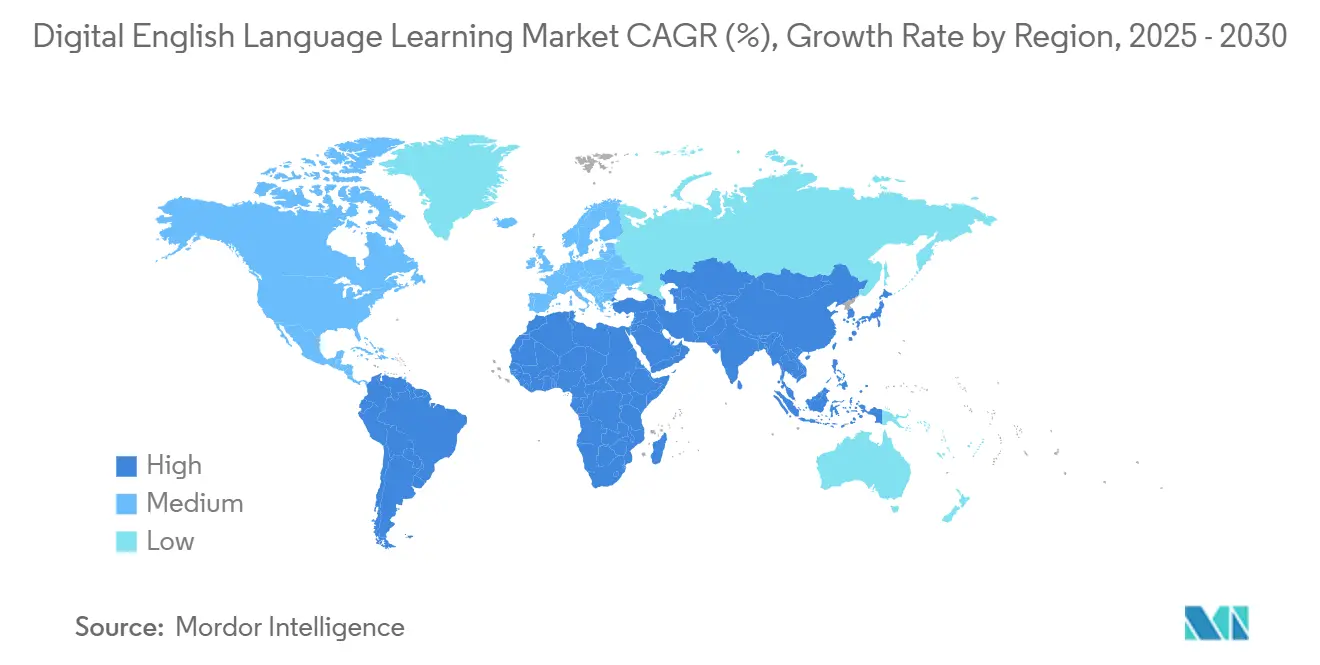

Asia-Pacific generated the largest USD value and 39.45% share of the digital English language learning market in 2024. China’s 400 million learners and India’s AI startup wave drive a 16.23% regional CAGR to 2030. Funding rounds underscore momentum: SpeakX secured USD 10 million to target Tier-2 cities where English skills open upward career mobility. South Korea’s AI textbook program and Indonesia’s primary-school mandate embed long-range demand signals.

North America’s corporate culture keeps the digital English language learning market size buoyant, as 67% of companies integrate mobile modules into upskilling suites. High smartphone penetration enables VR pilots and AI pronunciation labs at enterprise scale. Europe faces a demographic dip of 15.3 million English learners by 2025, yet business-English demand offsets declines as firms seek cross-border collaboration efficiency.

South America, the Middle East, and Africa account for smaller bases yet register double-digit growth. Zero-rated telco bundles in Nigeria and Kenya widen reach, and Brazil’s middle-class expansion nurtures a willingness to pay for certification-linked programs. Vendors must localize dialect examples and user interfaces to resonate across cultural contexts, raising product-development complexity while unlocking diversified revenue streams.

Competitive Landscape

Competitive intensity remains moderate. Duolingo’s AI-first roadmap launched 148 new courses and a Video Call feature that lifted daily active users 51% to 40 million in Q4 2024. Babbel surpassed 1 million US subscriptions after strengthening its B2B pipeline. Traditional publishers such as Pearson accelerate digital pivot through integrated learning analytics, while VR specialist Immerse partnered with Benesse and Meta to deliver headset-based role-play scenarios.

AI startups penetrate niches, pronunciation engines, industry-specific vocabulary, or localized cultural content, underscoring fragmentation. Consolidation looms as larger platforms acquire specialized algorithms to shore up differentiation. Content breadth, certification credibility, and enterprise integrations now define purchase criteria, pushing vendors toward interoperable APIs and single-sign-on functionality that lower IT overhead for buyers.

White-space opportunities persist in accent-specific fluency modules and low-bandwidth app versions for emerging markets. Market leaders refine user-lifecycle monetization: free onboarding funnels, mid-tier subscriptions, and high-margin certification bundles together maximize revenue per learner across tenure stages.

Digital English Language Learning Industry Leaders

-

Duolingo

-

Babbel

-

Pearson (English)

-

EF Education First

-

Busuu (Chegg)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: TOEFL has confirmed that adaptive design enhancements will be implemented in January 2026, allowing the Reading and Listening sections to adjust in real time based on a test taker's performance. This change aims to improve the exam's relevance, efficiency, and fairness by providing a more personalized assessment experience.

- February 2025: Sunlands Technology Group has integrated DeepSeek AI into its platform to deliver more personalized and adaptive learning experiences for adult learners in China. This strategic move positions the company to better serve the country’s rapidly growing adult-education market, which is valued at USD 788.3 billion.

- January 2025: iHuman Inc. has launched iHuman Chinese Reading, a new product aimed at enhancing early language development among children. The platform has quickly gained traction, reaching 29.12 million monthly active users (MAUs) and expanding its B2B services to nearly 10,000 kindergartens across China.

- July 2024: Indonesia has activated its Emancipated Curriculum, which notably reinstates English instruction starting from grade 1 to strengthen foundational language skills. The curriculum is set for a full nationwide rollout by the 2027/28 academic year, aiming to modernize education and enhance global competitiveness.

Global Digital English Language Learning Market Report Scope

| Self-Paced Digital Learning |

| Instructor-Led Live Online Classes |

| Immersive/VR-Based Learning |

| Blended/Hybrid Learning |

| Gamified Microlearning |

| K-12 Students |

| Higher Education Students |

| Corporate & Government Workforce |

| Individual Learners |

| Digital Courseware |

| Virtual-Classroom Platforms |

| Assessment & Certification Tools |

| Pronunciation & Fluency Tools |

| Integrated Learning Platforms |

| Cloud-based |

| On-premise |

| Subscription-based |

| Institutional Licensing |

| Pay-Per-Certification / One-Time Purchase |

| Freemium & Ad-Supported |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Benelux (Belgium, Netherlands, and Luxembourg) | |

| Nordics (Sweden, Norway, Denmark, Finland, and Iceland) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Learning Mode | Self-Paced Digital Learning | |

| Instructor-Led Live Online Classes | ||

| Immersive/VR-Based Learning | ||

| Blended/Hybrid Learning | ||

| Gamified Microlearning | ||

| By End User | K-12 Students | |

| Higher Education Students | ||

| Corporate & Government Workforce | ||

| Individual Learners | ||

| By Product Type | Digital Courseware | |

| Virtual-Classroom Platforms | ||

| Assessment & Certification Tools | ||

| Pronunciation & Fluency Tools | ||

| Integrated Learning Platforms | ||

| By Deployment | Cloud-based | |

| On-premise | ||

| By Business Model | Subscription-based | |

| Institutional Licensing | ||

| Pay-Per-Certification / One-Time Purchase | ||

| Freemium & Ad-Supported | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Benelux (Belgium, Netherlands, and Luxembourg) | ||

| Nordics (Sweden, Norway, Denmark, Finland, and Iceland) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the digital English language learning market today?

The digital English language learning market size stands at USD 13.94 billion in 2025 and is projected to double to USD 27.88 billion by 2030.

Which learning mode is growing fastest?

Immersive and VR-based learning posts the highest 19.58% CAGR as headsets simulate real-world conversational contexts, accelerating fluency.

Why does Asia-Pacific dominate adoption?

The region houses 400 million Chinese learners and a surge of Indian AI startups, coupled with government mandates that integrate digital English into school curricula.

What business models win in price-sensitive regions?

Freemium and ad-supported models grow at 18.17% CAGR because they lower entry costs while upselling premium features and certification add-ons.

How are corporations using digital English tools?

Roughly 67% of US firms embed mobile language modules into workforce programs, often pairing AI conversation coaches with performance analytics to raise global collaboration efficiency.

What key technology drives personalization?

Cloud-hosted AI engines analyze speech and engagement data in real time, tailoring lesson difficulty and timing to individual proficiency gaps.

Page last updated on: