Chickpea Market Size and Share

Chickpea Market Analysis by Mordor Intelligence

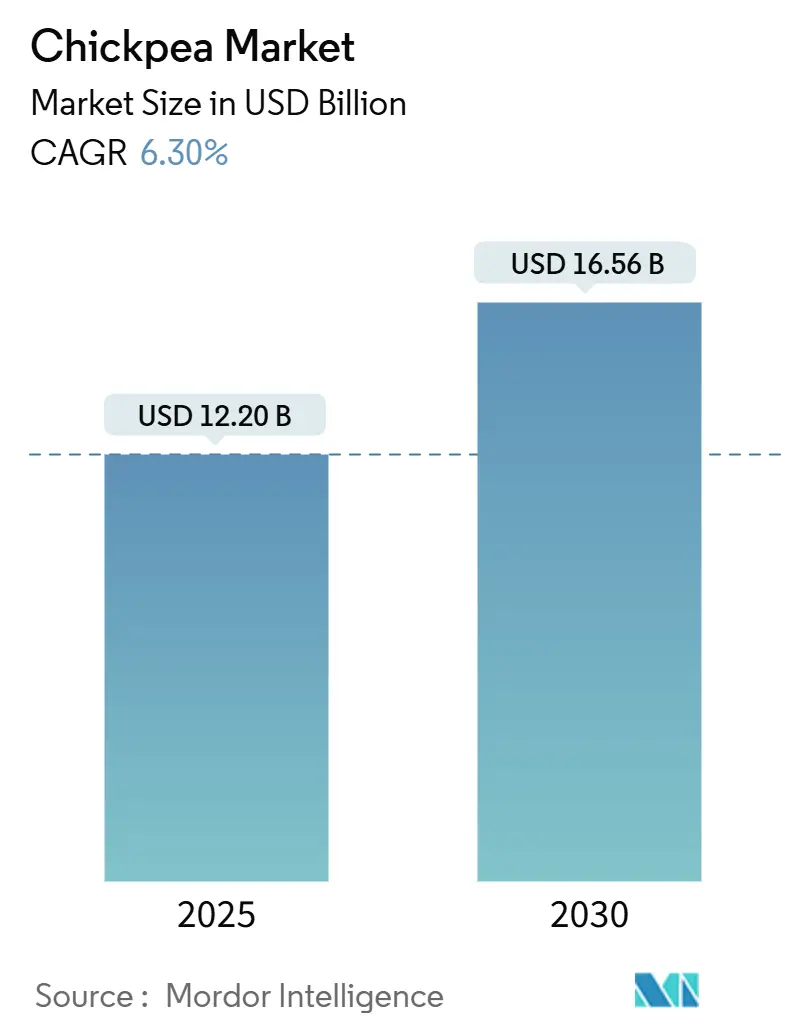

The chickpea market reached a market size of USD 12.2 billion in 2025 and is forecast to climb to USD 16.56 billion by 2030, reflecting a 6.3% CAGR over the period. Robust demand from plant-based eating trends, rapid uptake of pulse proteins in functional foods, and government-backed nutrition programs are the pivotal growth drivers. Companies are scaling processing capacity for high-purity isolates while simultaneously valorizing by-products such as aquafaba for clean-label emulsifiers. Digital agriculture tools are beginning to narrow historic yield gaps in smallholder systems, supporting a more reliable supply. On the demand side, gluten-free bakery innovation and mainstream adoption of meat alternatives are broadening chickpea applications, encouraging ingredient manufacturers to lock in longer contracts and invest in upstream traceability platforms. The market also reflects growing price premiums for high-protein and organic variants, signaling an enduring shift toward value-added positioning.

Key Report Takeaways

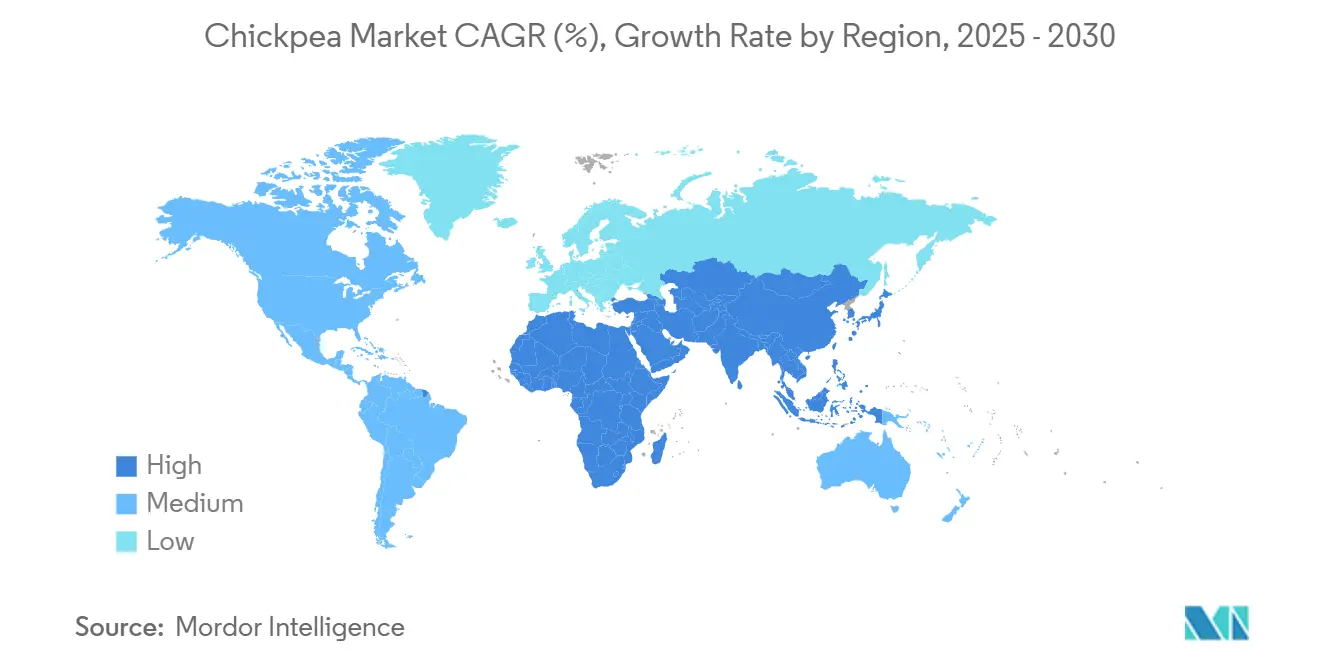

- By geography, Asia-Pacific held 36% of the chickpea market share in 2024, confirming its position as the largest regional contributor. Africa is projected to grow at a 7.20% CAGR through 2030, making it the fastest-expanding regional segment.

Global Chickpea Market Trends and Insights

Drivers Impact Analysis

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding vegan and flexitarian populations | +1.8% | Global, with a concentration in North America and Europe | Medium term (2-4 years) |

| Surge in pulse-based protein isolates for functional foods | +1.5% | North America, Europe, and the Asia-Pacific | Medium term (2-4 years) |

| Growth of gluten-free bakery and snack categories | +1.2% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Government biofortification programs for climate-smart legumes | +0.9% | Africa, South Asia, with expansion to South America | Long term (≥ 4 years) |

| Circular-economy valorization of chickpea by-products | +0.6% | Europe, North America, with emerging adoption in Asia | Long term (≥ 4 years) |

| Digital agriculture boosting smallholder chickpea yields | +0.7% | Africa, South Asia, with spillover to the Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Vegan and Flexitarian Populations

Plant-based dietary adoption is outpacing animal protein growth as consumers pursue ethical, health, and environmental goals. Similar shifts are observed in the United States, where omnivores account for over half of all plant-based product purchases, confirming that pulses have penetrated mainstream grocery baskets. Brands are leveraging the halo effect of “clean protein” to launch chickpea-based ready meals, nutrition bars, and milk alternatives that target flexitarian shoppers. The demographic sweet spot overlaps with younger, urban consumers whose purchasing power is set to expand through 2030. This shift fuels demand for reliable ingredient quality, prompting processors to formalize long-term contracts with growers.

Surge in Pulse-Based Protein Isolates for Functional Foods

Technological advances in membrane filtration and salt-based extraction have delivered chickpea protein isolates exceeding 90% purity while retaining solubility and gel strength vital for meat analogs[1]Source: Baraem Ismail, “Salt Solubilization Coupled with Membrane Filtration,” Foods, foodsmdpi.com. Strategic partnerships, such as Ingredion teaming with InnovoPro, accelerate commercialization by pairing global distribution with proprietary extraction know-how. The result is a virtuous cycle: reliable isolate quality encourages food formulators to trial chickpea proteins, which in turn secures off-take agreements that justify further capacity expansion. End uses now include sports-nutrition powders, spoonable yogurts, and frozen desserts, pushing demand beyond historical hummus and flour applications.

Growth of Gluten-Free Bakery and Snack Categories

Chickpea flour’s 12-14% protein content and neutral flavor make it a preferred gluten-free base. Tortilla formulations with 30% chickpea flour deliver higher iron and potassium without sacrificing flexibility, expanding options for better-for-you snack wraps[2]Source: Asmaa Benayad et al., “Addition of Chickpea Flour in Durum Wheat Flour,” Foods, mdpi.com. Artisan bakeries have adopted steamed chickpea flour, which achieves 18-month shelf stability and eliminates bitter notes common in raw pulse flours. Mainstream brands have responded; global product launches that feature chickpea as a primary ingredient rose nearly 20% between 2021 and 2022, tightening ingredient supply and prompting growers in Australia and Canada to allocate larger acreage.

Government Biofortification Programs for Climate-Smart Legumes

Public-sector initiatives are upgrading chickpea micronutrient profiles while also boosting yields. Canada’s “Expanding Nutrients in Food Systems” project targets more than 11 million beneficiaries across five countries by 2027. Field trials demonstrate that foliar applications of zinc and iron nanoparticles lift yields to 14.10 quintals per hectare and fortify grain iron levels by more than 30%. In parallel, the USDA Agricultural Research Service is screening 300 chickpea accessions to identify genetic markers for protein, fiber, and fatty acid concentrations, accelerating cultivar development pipelines. These programs enhance both nutritional value and climate resilience, strengthening long-term demand.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Yield volatility from El Niño-linked drought cycles | -1.4% | Global, with a severe impact in Africa and South Asia | Short term (≤ 2 years) |

| Post-harvest mycotoxin contamination risks | -0.8% | Developing countries, particularly South Asia and Africa | Medium term (2-4 years) |

| Price under-cutting from synthetic pea-protein concentrates | -0.7% | North America and Europe | Medium term (2-4 years) |

| Logistics bottlenecks at key export ports | -0.5% | Australia, India, and emerging African exporters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Yield Volatility from El Niño-Linked Drought Cycles

Historical El Niño events have slashed chickpea output by up to 65% in Ethiopia and 25-30% in India, triggering price spikes and import surges. Drought stress not only limits yield but also amplifies root pathogens, with dry root rot incidence expanding 14-fold under severe moisture deficits. Growers in semi-arid belts increasingly shift acreage to more drought-tolerant pulses or cereals during forecasted El Niño years, compounding supply tightness. Breeding programs are accelerating drought-escape varieties, but widespread adoption remains several seasons away. Adaptation strategies include developing drought-tolerant varieties and implementing supplemental irrigation systems, with research indicating that early sowing and short-duration cultivars can mitigate some yield losses.

Post-Harvest Mycotoxin Contamination Risks

Aflatoxin B1 exceeded regulatory thresholds in 62% of Pakistani chickpea lots sampled in 2023. Contamination triggers costly rejections in European ports where limits are set at 2 parts per billion, undermining exporter margins. Climate change lengthens warm, humid storage windows that favor Aspergillus growth. Technologies such as plasma treatment and controlled-atmosphere storage show promise, yet demand capital outlays are seldom feasible for small-volume traders. The economic impact extends beyond direct losses, with contamination risks increasing insurance costs and requiring investment in detection and management systems throughout the supply chain.

Geography Analysis

Asia-Pacific captured 36% of the chickpea market share in 2024, reflecting entrenched culinary traditions and expanding packaged food use. The chickpea market size attached to regional processing clusters is anticipated to widen as multinational snack brands procure from dedicated sourcing hubs. The regional dynamics reflect divergent consumption patterns and production capabilities that are reshaping global trade flows.

Africa’s contribution remains smaller in absolute terms, yet the region posts the fastest CAGR at 7.20% through 2030. Ethiopia leveraged digital extension platforms to lift yields and unlock export quality standards, aligning with EU import protocols. Donor-funded biofortification projects introduce high-iron varieties, enhancing both domestic nutrition and premium export positioning. The chickpea market size for African origin shipments is projected to surpass USD 430 million by 2030, buoyed by trade diversification into Middle Eastern and Southeast Asian destinations.

North America and Europe command premium niches focused on high-protein flours and isolates destined for flexitarian product lines. Recent consolidation, exemplified by Above Food’s takeover of The Redwood Group’s specialty crop division, signals an emerging scale play to secure contiguous supply in these mature but innovation-oriented markets. Australia’s record 2 million metric tons harvest showcases the potential for counter-seasonal supply to smooth global availability, though logistics constraints remain a limiting factor. South America contributes modestly through Argentine and Brazilian acreage expansions focused on counter-seasonal supply windows. Meanwhile, Turkey’s target of USD 1 billion in food exports to China over five years underscores the Middle East’s ambitions to leverage geographic proximity as a trading bridge[3]Source: Ege İhracatçı Birlikleri, “Turkish food exporters set USD 1 billion target for China,” eib.org.tr.

Recent Industry Developments

- August 2024: Above Food secured its position among North America’s largest suppliers through the purchase of The Redwood Group’s specialty crop ingredient division.

- February 2024: InnovoPro launched barista-grade chickpea protein to expand its plant-based protein ingredient segment, which is anticipated to boost the food and beverage industry.

Global Chickpea Market Report Scope

A chickpea is a hard, pale brown, round seed that can be cooked and eaten. They are very versatile, healthy, and easy to cook. The Chickpea market is segmented by Geography into North America, Europe, Asia-Pacific, South America, and Africa. The report includes production (volume), consumption (volume and value), import (volume and value), export (volume and value), and price trend analysis. The report offers market size and forecasts in terms of value (USD) and volume (metric tons) for all the above segments.

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Asia-Pacific | India |

| China | |

| Australia | |

| Japan | |

| Middle East | Turkey |

| Saudi Arabia | |

| United Arab Emirates | |

| Africa | South Africa |

| Egypt | |

| Ethiopia |

| By Geography (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis) | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Asia-Pacific | India | |

| China | ||

| Australia | ||

| Japan | ||

| Middle East | Turkey | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Africa | South Africa | |

| Egypt | ||

| Ethiopia | ||

Key Questions Answered in the Report

How big is the chickpea market size in 2025?

The chickpea market size reached USD 12.2 billion in 2025.

What is the forecast growth rate through 2030?

The market is projected to expand at a 6.3% CAGR between 2025 and 2030.

Which region leads global consumption?

Asia-Pacific accounts for 36% of global consumption, driven by India and China.

Which region will grow the fastest?

Africa is forecast to post a 7.20% CAGR through 2030.

What are the main restraints to growth?

Drought-linked yield volatility, mycotoxin contamination, synthetic protein price competition, and port logistics bottlenecks pose the key challenges.

Page last updated on: