Automotive Start-Stop System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

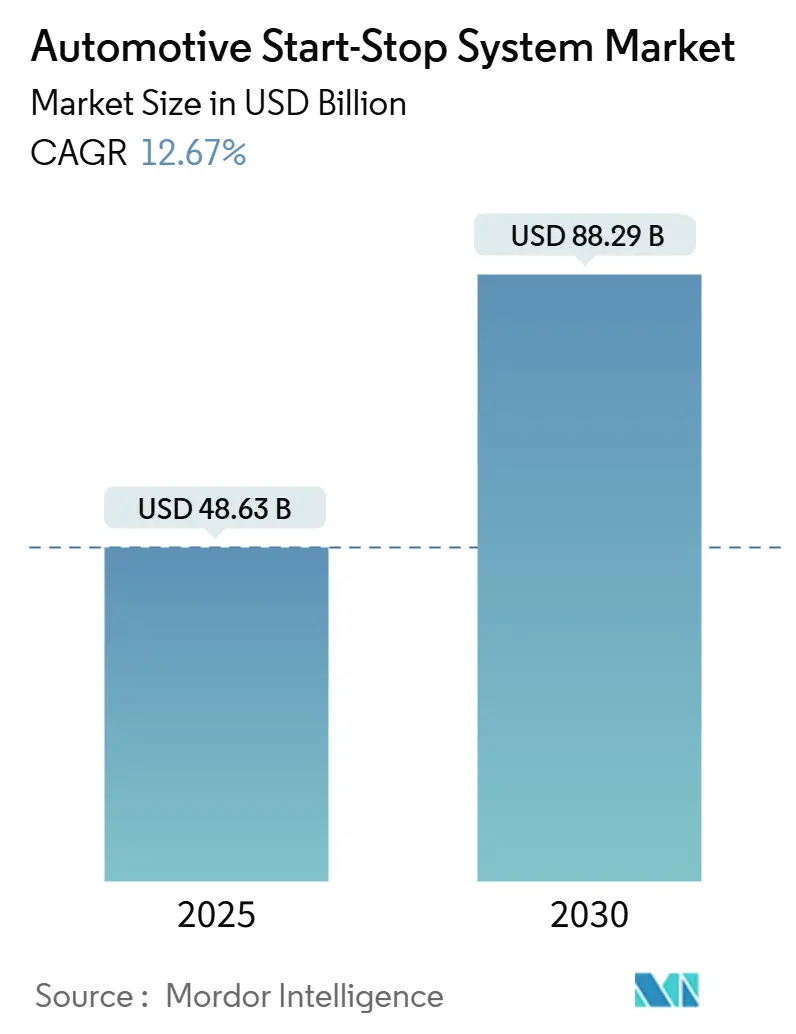

| Market Size (2025) | USD 48.63 Billion |

| Market Size (2030) | USD 88.29 Billion |

| Growth Rate (2025 - 2030) | 12.67% CAGR |

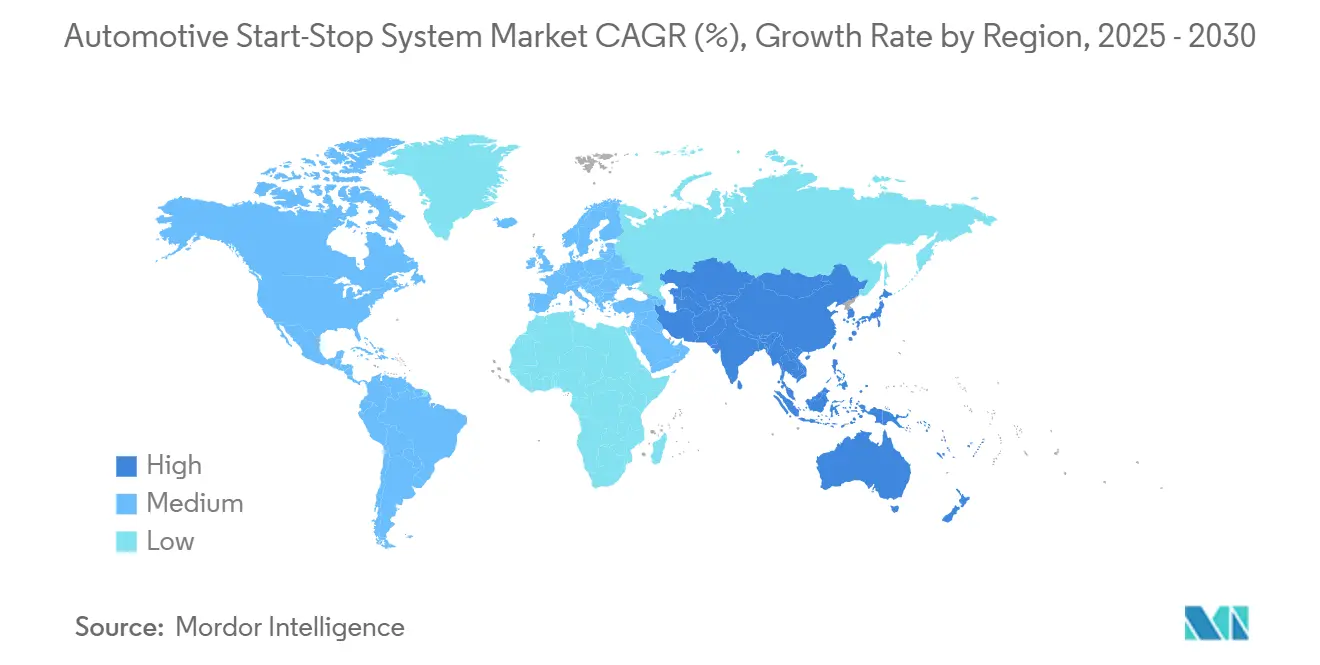

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Start-Stop System Market Analysis by Mordor Intelligence

The automotive start-stop system market size is USD 48.63 billion in 2025 and is set to reach USD 88.29 billion by 2030, advancing at a 12.67% CAGR. Several forces propel this expansion: converging Corporate Average Fuel Economy (CAFE) and CO₂ regulations in the United States, Europe, China, and India; accelerating OEM roll-outs of 48 V mild-hybrid architectures; falling lithium-ion battery costs that lengthen battery life; and fleet operators’ search for idle-reduction technologies that cut fuel spend in last-mile operations. Competitive intensity is rising as legacy Tier-1 suppliers acquire electrified-powertrain specialists, semiconductor vendors bundle power devices with software, and battery firms pursue deeper vertical integration. Opportunities emerge in Asia-Pacific manufacturing hubs, light commercial vehicle fleets, and service-market parts as the installed base ages.

Key Report Takeaways

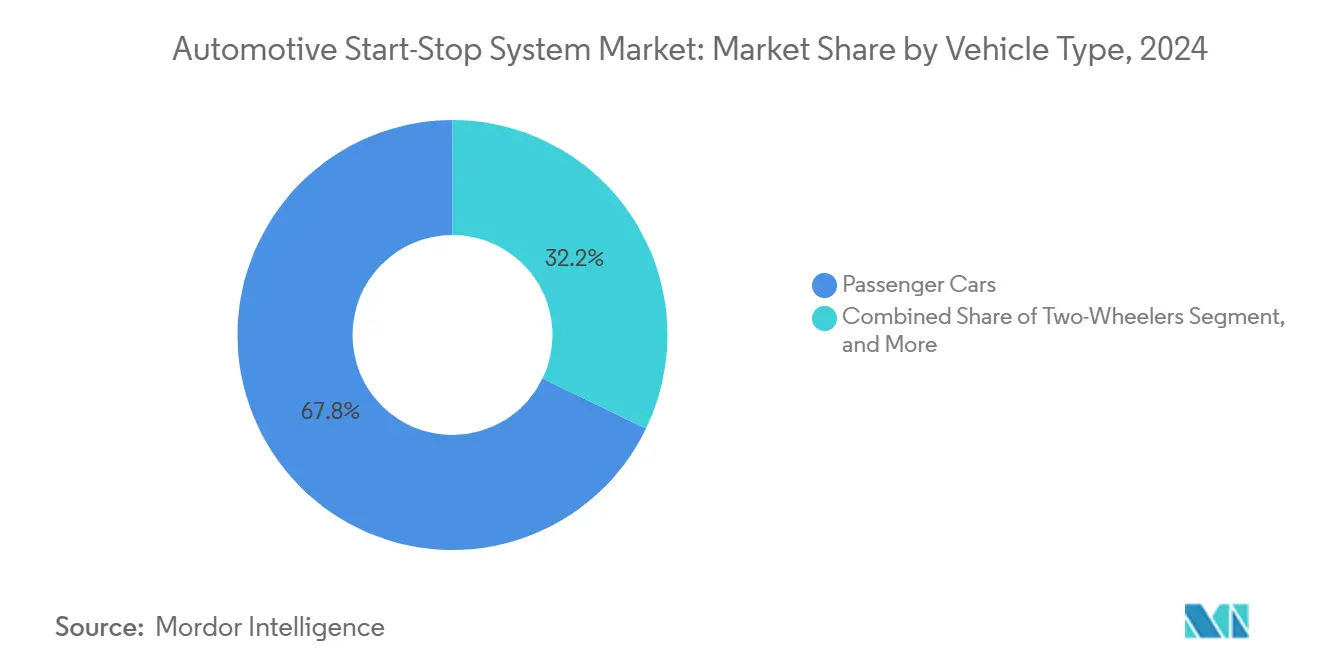

- By vehicle type, passenger cars led with 67.84% revenue share in 2024, while light commercial vehicles are forecast to expand at a 13.57% CAGR to 2030.

- By technology, belt-driven alternator starter units commanded 46.52% of revenue in 2024, whereas integrated starter generator systems are projected to grow at a 13.89% CAGR through 2030.

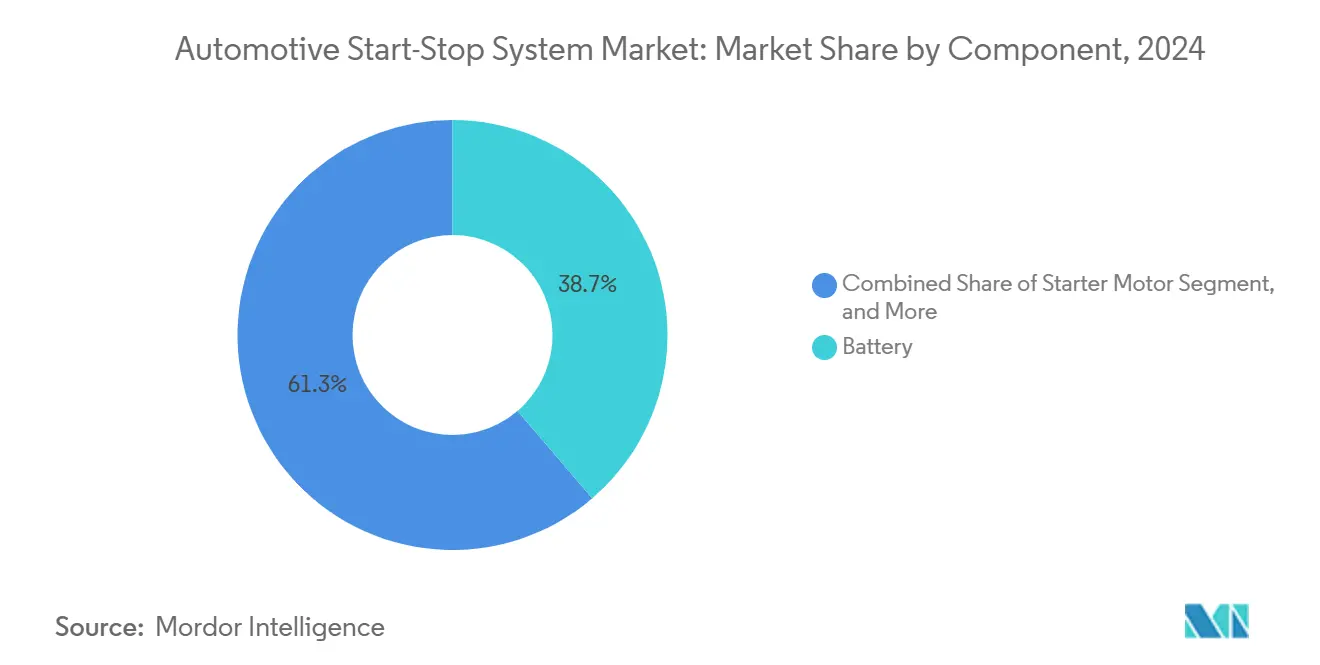

- By component, batteries accounted for a 38.73% share in 2024, while control units and sensors registered the fastest 12.94% CAGR over the forecast period.

- By fuel type, gasoline applications captured a 53.87% share in 2024, while hybrid configurations, including 48 V systems, advance at a 13.43% CAGR to 2030.

- By geography, Asia-Pacific dominated with a 42.94% share in 2024 and is expected to post the highest 12.89% CAGR through 2030.

Global Automotive Start-Stop System Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened CAFE and CO₂ regulations | +2.1% | North America, EU | Medium term (2-4 years) |

| Rising demand for micro-hybrid passenger cars | +1.8% | Asia-Pacific, Latin America | Long term (≥ 4 years) |

| OEM integration of 48 V mild-hybrid architectures | +1.5% | Global premium segments | Medium term (2-4 years) |

| Decreasing lithium-ion battery costs | +1.2% | Global manufacturing centers | Short term (≤ 2 years) |

| Fleet electrification mandates for commercial vans | +0.9% | North America, EU | Medium term (2-4 years) |

| Insurance-telematics incentives for idle reduction | +0.6% | Developed telematics markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heightened CAFE and CO₂ Regulations

Converging fuel-economy and carbon-emission rules in the United States, the European Union, China, and India make start-stop systems a default fitment on new internal combustion platforms. [1]U.S. Environmental Protection Agency, “Final Rule – Greenhouse Gas Emissions Standards for Model Years 2027-2032,” epa.gov Automakers risk steep fines for non-compliance, so start-stop integration occurs even where consumer demand is weak. The policy momentum also shortens product-planning cycles, pushing OEMs to adopt modular 12 V and 48 V systems that scale across global vehicle platforms. Suppliers with multi-region homologation capabilities, therefore, position themselves as compliance partners rather than component vendors.

Rising Demand for Micro-Hybrid Passenger Cars

Household budgets in emerging economies remain fuel-price sensitive, turning micro-hybrid passenger cars into a cost-effective step toward electrification. [2]Ministry of Road Transport and Highways, “End-of-Life Vehicle Rules, 2025,” morth.nic.in Localized production in India, China, and Southeast Asia trims logistics costs and import duties, keeping system prices within reach of mass-market segments. Urban stop-and-go traffic patterns amplify the fuel-saving value proposition, encouraging OEMs to market start-stop technology as a convenience feature alongside efficiency gains.

OEM Integration of 48 V Mild-Hybrid Architectures

Premium brands now standardize 48 V electrical systems that pair seamlessly with integrated starter generator hardware. [3]BMW Group, “48 V Mild-Hybrid Integration,” bmwgroup.com The higher voltage enables faster, quieter restarts and unlocks ancillary functions such as electric boost and coasting. Semiconductor makers package power MOSFETs, gate drivers, and microcontrollers into single modules, lowering bill-of-materials costs and simplifying vehicle-level integration. As 48 V architectures cascade from luxury to volume segments, suppliers able to deliver both 12 V and 48 V solutions gain share.

Decreasing Lithium-Ion Battery Costs

Automotive-grade lithium-ion pack prices continued to decline through 2024, allowing OEMs to specify higher-cycle-life batteries for start-stop duty without a cost penalty. Extended flooded lead-acid (EFB) and absorbent glass-mat (AGM) chemistries also absorb cost pressures, generally improving warranty confidence among fleet operators. Coupled with smarter battery-management software, lower cell prices directly tackle historic consumer skepticism around replacement costs.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Battery-electric vehicle cannibalization | –1.4% | Developed EV markets | Long term (≥ 4 years) |

| Semiconductor supply-chain fragility | –0.8% | Global | Short term (≤ 2 years) |

| Consumer durability concerns | –0.7% | Emerging markets | Medium term (2-4 years) |

| Regulatory uncertainty in developing regions | –0.5% | Africa, parts of South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Adoption of Battery-Electric Vehicles Cannibalizing Fitment

In markets where full EV penetration exceeds 15%-notably Norway, the Netherlands, and California-start-stop fitment faces a structural ceiling because pure battery vehicles remove the internal combustion engine altogether. Luxury OEMs allocate R&D toward dedicated EV platforms, further shrinking the premium ICE addressable base. Suppliers buffer the risk by diversifying into DC-DC converters, onboard chargers, and thermal-management modules that serve both EV and hybrid architectures.

Supply-Chain Fragility for Power Semiconductors

Tight wafer capacity and geopolitical concentration of fabrication in East Asia expose the automotive start-stop system market to component shortages, especially for 40-60 V MOSFETs and high-current relays. Lead times lengthened to more than 40 weeks during the 2021-2022 shortage, prompting OEMs to dual-source or redesign around alternative packages. Tier-1 suppliers respond by locking multi-year capacity reservations and investing in failure-in-time (FIT)-rate analytics to reassure automakers on supply security.

Segment Analysis

By Vehicle Type: Commercial Fleets Accelerate Adoption

Passenger cars delivered 67.84% of the automotive start-stop system market in 2024, while light commercial vehicles are projected to expand at a 13.57% CAGR through 2030. Fleet owners calculate payback periods of fewer than 24 months when vehicles run dense urban routes with high idle times. Telematics platforms quantify fuel savings, reinforcing procurement decisions.

As regulatory bodies in Europe and North America tighten tailpipe CO₂ caps for vans, OEMs embed start-stop systems as standard equipment on new models. Emerging last-mile logistics networks in India and Southeast Asia compound unit demand. In heavy commercial vehicles, adoption remains selective because auxiliary loads such as refrigeration complicate restart cycles, yet pilot programs in refuse-collection fleets indicate growing feasibility.

Note: Segment shares of all individual segments available upon report purchase

By Technology: ISG Systems Gather Momentum

Belt-driven alternator starter solutions accounted for 46.52% of the automotive start-stop system market share in 2024, but integrated starter generator units will record a 13.89% CAGR up to 2030. BDAS retains traction in cost-sensitive A- and B-segment cars due to proven reliability.

ISG platforms, though costlier, deliver near-imperceptible restarts and regenerative braking energy up to 15 kW, aligning with premium brand expectations. As 48 V wiring looms become commonplace, the cost delta narrows, promoting ISG penetration into high-volume C-segment crossovers. Direct-starter architectures shrink in share but persist in niche retrofit programs and emerging-market two-wheelers.

By Component: Intelligence Outpaces Electro-Mechanical Content

Batteries represented 38.73% of the automotive start-stop system market size in 2024; control units and sensors rose fastest at a 12.94% CAGR. Growing software content captures more value as OEMs demand diagnostic data, state-of-charge algorithms, and cybersecurity compliance.

Starter motors and alternators see incremental design innovations centered on friction reduction and thermal optimization, but face pricing pressure as production scale rises. Wiring harnesses, mounts, and auxiliary hardware stay largely commoditized, though lightweight aluminum cabling becomes more common to meet vehicle-level mass targets.

Note: Segment shares of all individual segments available upon report purchase

By Fuel Type: Hybrid Bridges the Transition

Gasoline powertrains held 53.87% share of the automotive start-stop system market in 2024, yet hybrid variants will post the swiftest 13.43% CAGR to 2030. Diesel adoption contracts in European passenger cars but stabilizes in commercial fleets, where torque requirements dominate.

Hybrid growth stems from OEM roadmaps that stretch internal-combustion asset life while achieving interim emission reductions. In price-sensitive markets, bi-fuel compressed natural gas vans increasingly specify start-stop systems to maximize range. Alternative fuels, including ethanol blends and liquefied petroleum gas, remain niche but garner regulatory attention in Brazil and India, suggesting localized upside.

Geography Analysis

Asia-Pacific contributed 42.94% of the automotive start-stop system market revenue in 2024 and is projected to grow at a 12.89% CAGR through 2030. China mandates fleet-wide corporate average fuel-consumption targets that tighten annually, while India enforces End-of-Life Vehicle recycling rules from April 2025 that spur component design upgrades. Japanese and South Korean OEMs export high-value 48 V systems worldwide, leveraging domestic expertise in power electronics.

Europe remains a technology trendsetter as the 2025-2030 CO₂ roadmap calls for 15% fleet emission cuts; start-stop adoption in A- and B-segment cars is saturated, but replacement demand and mild-hybrid premium segments sustain volumes. North America’s new EPA greenhouse-gas framework for model years 2027-2032 amplifies demand, particularly in pickup trucks and vans, where idle times are lengthy.

The Middle East and Africa record modest uptake, yet Saudi Arabia’s fuel subsidy reforms and South Africa’s urban-air-quality policies lay the groundwork for future growth. South America exhibits uneven momentum; Brazil’s flex-fuel fleet offers a testing ground for dual-fuel combustion strategies, though macroeconomic volatility tempers procurement cycles.

Competitive Landscape

The automotive start-stop system market features moderate consolidation. Schaeffler closed its USD 21 billion acquisition of Vitesco Technologies in October 2024, integrating starter-generator, power-electronics, and drivetrain software portfolios. Continental added 700 new aftermarket SKUs for 2025 service channels, defending lifetime-revenue streams on its installed base. Robert Bosch advances the Powernet Guardian platform, embedding cybersecurity and energy-optimization functions across both 12 V and 48 V architectures.

Semiconductor vendors such as STMicroelectronics and ROHM deepen partnerships with Tier-1s to lock design wins for power devices, while battery specialists Johnson Controls and Hitachi Astemo invest in manufacturing upgrades that deliver higher cycle life and thermal robustness. Market entrants focus on software layers-predictive idle-stop algorithms, over-the-air calibration, and telematics analytics-challenging hardware-centric incumbents.

Competitive intensity grows fastest in Asia-Pacific, where local suppliers bundle start-stop hardware with region-specific after-sales networks. In Europe and North America, regulatory compliance expertise and established OEM relationships remain decisive differentiators. Overall, the top five suppliers control roughly 55% of global revenue, signaling a moderately concentrated structure.

Automotive Start-Stop System Industry Leaders

-

Aisin Corporation

-

BorgWarner Inc.

-

DENSO Corporation

-

Valeo SA

-

Robert Bosch GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: India implemented End-of-Life Vehicle Rules mandating certified recycling and setting material traceability requirements that influence start-stop component design

- October 2024: Schaeffler completed acquisition of Vitesco Technologies to create an integrated powertrain powerhouse

- September 2024: Continental announced 700+ new aftermarket part numbers, including start-stop batteries, alternators, and control units for 2025 release

- August 2024: Robert Bosch reported USD 99.3 billion revenue for 2024 and highlighted Powernet Guardian for 48 V architectures

Global Automotive Start-Stop System Market Report Scope

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Two-Wheelers |

| Belt-Driven Alternator Starter (BDAS) |

| Integrated Starter Generator (ISG) |

| Direct Starter |

| Battery |

| Starter Motor |

| Alternator |

| Control Unit and Sensors |

| Other Component |

| Gasoline |

| Diesel |

| Hybrid (Incl. 48-V) |

| Alternative Fuels (CNG, LPG, Flex-Fuel) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Vehicle Type | Passenger Cars | ||

| Light Commercial Vehicles | |||

| Heavy Commercial Vehicles | |||

| Two-Wheelers | |||

| By Technology | Belt-Driven Alternator Starter (BDAS) | ||

| Integrated Starter Generator (ISG) | |||

| Direct Starter | |||

| By Component | Battery | ||

| Starter Motor | |||

| Alternator | |||

| Control Unit and Sensors | |||

| Other Component | |||

| By Fuel Type | Gasoline | ||

| Diesel | |||

| Hybrid (Incl. 48-V) | |||

| Alternative Fuels (CNG, LPG, Flex-Fuel) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the 2025 value of the automotive start-stop system market?

It stands at USD 48.63 billion.

How fast will the market grow through 2030?

Revenue is projected to rise at a 12.67% CAGR, reaching USD 88.29 billion.

Which vehicle category shows the quickest growth?

Light commercial vehicles expand at 13.57% CAGR through 2030.

Why are 48 V systems important for start-stop technology?

They enable integrated starter generator units that deliver smoother restarts and additional energy-recapture functions.

Which region generates the largest revenue?

Asia-Pacific contributes 42.94% of global revenue and grows at 12.89% CAGR.

How will BEV adoption affect demand?

Rising BEV penetration in developed markets limits future addressable volumes for start-stop systems, trimming the long-term growth rate.

Page last updated on: