The Federal Reserve announced at its October 28-29 policy meeting it was cutting rates for the second time this year, lowering the target range by a quarter percentage to 3.75%-4.00%.

After the recent cut in September, the move shows central bankers are more worried about a softening labor market than about elevated levels of inflation.

Jerome Powell, chair of the Federal Reserve, put it this way: “In the near term, risks to inflation are tilted to the upside and risks to employment to the downside—a challenging situation. There is no risk-free path for policy as we navigate this tension between our employment and inflation goals. Our framework calls for us to take a balanced approach in promoting both sides of our dual mandate.”

In its statement, the Fed also signaled another rate cut in December “is not a forgone conclusion.” This means the central bank is planning to make borrowing cheaper, but maybe not before the year ends.

For savers, the implications are immediate. Top certificate of deposit (CD) yields are brushing up against 4.10% annual percentage yield (APY), while the national average savings rate languishes at just 0.40%, according to the FDIC. That spread won’t hold for long. As the Fed moves down, banks follow, often quickly.

Consumers face a shrinking window. Locking in a rate today could pay off when deposit yields inevitably start sliding in the months ahead. Fixed-term CDs are the surest way to capture today’s high rates, but flexibility matters too. A ladder of six- to 24-month terms, paired with a no-penalty or bump-up CD, can help balance security with liquidity.

The bigger risk is inertia. Once cuts accelerate, banks will waste no time shaving yields. Waiting too long could mean watching top-tier returns vanish while inflation keeps chewing away at cash.

Not sure whether to lock in or stay liquid? We’ll break down the numbers and the smartest moves to protect your savings while the Fed’s new path takes shape.

Discover® 12-Month Certificate of Deposit term

Annual Percentage Yield

4.05%

Minimum Deposit Requirement

$0

Member FDIC

4.05%

$0

Are CD Rates Rising, Falling or Staying the Same?

The national average for a 12-month CD has already slipped, down to 1.68% in October 2025 from 1.81% a year earlier, according to the Federal Reserve Bank of St. Louis. That decline may seem small, but it’s a sign of where things are headed now that the Fed has begun cutting rates.

By comparison, Sallie Mae is still offering far higher yields. Its 12-month CD pays 4.00% APY, while the 15-month CD goes up to 4.10% APY. Even shorter terms like six and nine months are at 3.90% APY, which is more than double the national average. The spread shows why shopping around matters. Sticking with a big bank could mean earning under 2.00%, while moving to a competitive online bank could quadruple your return.

And more rate cuts are on the table.

That means CD yields are likely to drift lower over the next six to 12 months. Banks that were once competing aggressively for deposits may start to pull back, especially if borrowing costs continue to fall.

For consumers, this is a narrowing window. Locking in a CD with a competitive online bank can help preserve higher yields before the market resets.

A CD ladder of six- to 24-month terms offers balance, keeping part of your savings liquid while protecting the best available rates. Adding a no-penalty or bump-up CD can provide extra flexibility if banks shift strategy faster than expected.

The bottom line: Fed policy is moving in a direction that will put pressure on deposit rates. Savers who wait could end up stuck near the national average, while those who shop around now can still lock in 4.00% or better.

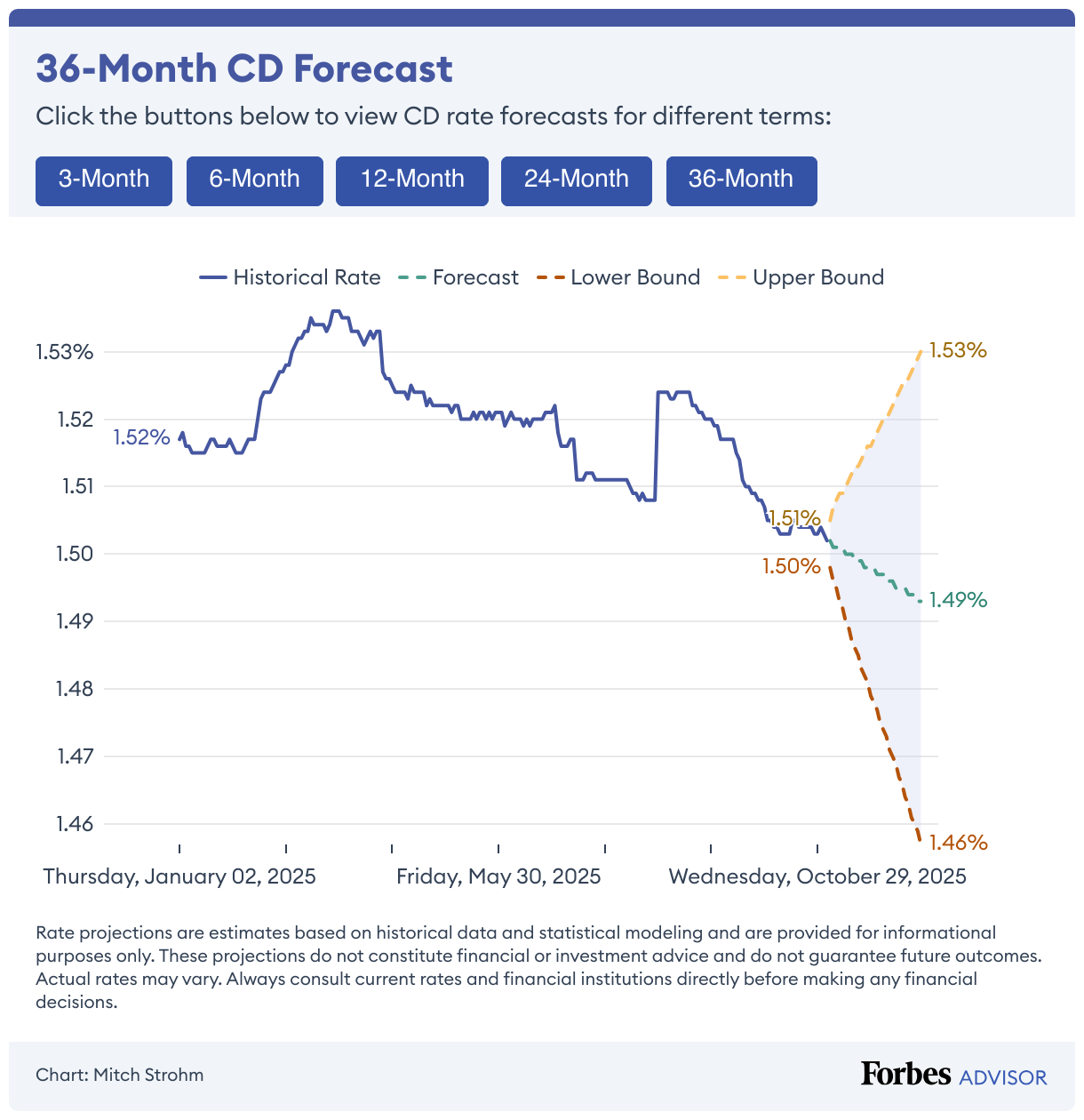

Wondering where CD rates might be heading in the short term? The forecast below provides our best estimate based on current data.

Historical CD Rates: 1980 – 2025

Here’s a look at how CD rates have performed over the past few decades.

CD Rates From 1980 to 1989

The 1980s began with the highest CD interest rates in 60 years. In March 1980, six-month CD rates averaged 17.74% APY, and the rate rose to 17.98% in August 1981. At the same time, the average 3-month CD rate hit 18.65%. But these historically high interest rates were tempered by high inflation rates—13.30% in 1979 and 12.40% in 1980.

Editor’s note: The specific rates mentioned in this section might not be represented in the graph above because average annual rates were used as data points rather than monthly rates.

The 1980s also began with the worst recession in the United States since the Great Depression. In late 1982, the unemployment rate reached 11%. And with lower employment rates comes reduced deposits. Average six-month CD rates remained high, at 12.57% in 1982, but dropped to 9.28% in 1983 as inflation remained low and recovery began.

Interest rates hit 12.08% in June 1984, but the remainder of the ’80s saw interest rates averaging between 6.5% and 10.8%.

CD Rates From 1990 to 1999

At the beginning of 1990, CD interest rates were still above 8%. But that year later saw a recession, which cooled inflation and contributed to declining CD rates. The average interest rate for six-month CDs dropped to 3.76% in 1992 and 3.28% in 1993.

Editor’s note: The specific rates mentioned in this section might not be represented in the graph above because average annual rates were used as data points rather than monthly rates.

By 1994, rates rose and hovered between 5% and 5.7% and stayed there through the end of 1999.

CD Rates From 2000 to 2009

With two recessions bookending the decade, 2000 to 2009 saw large fluctuations in CD rates. The rates in 2000 averaged 6.59%, but when the dot-com bubble burst that year, causing a stock market crash, the Fed lowered interest rates below 2.00% to counter the resulting recession of 2001. Rates on six-month CDs fell to 3.66% in 2001 and 1.81% in 2002 before bottoming out at 1.17% in 2003.

Editor’s note: The specific rates mentioned in this section might not be represented in the graph above because average annual rates were used as data points rather than monthly rates.

Rates rebounded in 2005, and from 2006 through 2007 consumers enjoyed rates around 5.20% on six-month CDs. But when the Great Recession began in 2008, rates fell to 3.14%. And in 2009, as foreclosure rates rose again, six-month CD rates fell to 0.87%—the lowest rate seen in over five decades.

CD Rates From 2010 to 2019

In the wake of the housing market crash and record-high foreclosures that occurred during the Great Recession, the government helped stabilize banks by giving them large cash bailouts. These cash infusions made banks less dependent on competitive interest rates to bring in deposits.

Throughout the 2010s, interest rates on six-month CDs remained low. Between 2010 and 2012, rates averaged 0.42% to 0.44%. In 2013, rates dropped below 0.15% for six-month CDs, while 12-month CDs remained under 1.00%.

Editor’s note: The specific rates mentioned in this section might not be represented in the graph above because average annual rates were used as data points rather than monthly rates.

Unlike previous decades when short-term CDs offered competitive rates and long-term CDs paid a lower rate of return, the 2010s saw the APY on CDs flatten across all terms.

While six-month CD rates remained the same throughout 2017, 12-month CD rates continued to fall and fluctuated between 0.20% and 0.30%. The years 2018 and 2019 saw a small uptick in rates as APYs on six-month and 12-month CDs rose to 0.40% and 0.60%, respectively. At the same time, 60-month CDs rose above 1.10% and paid up to 1.22% by the end of 2018. Overall, the decade saw historical lows in CD rates.

CD Rates Since 2020

In 2020, rates remained low. As recently as 2021, large national banks were still paying rates below 0.30% on CDs, while many online banks were offering competitive CD rates close to the national rate cap.

Beginning in April 2022, the effective federal funds rate rose dramatically, from 0.33% in April to 3.08% in October. As lending rates increased in 2022, CD rates also rose through the entire year. Banks were willing to incentivize savings to capitalize on the higher loan APRs. Paired with the conclusion of the Restoration Plan for reserve requirements, banks continued to encourage savings deposits as they were required to maintain a 2% cash reserve. By December 2022, the effective federal funds rate reached 4.10%.

CD rates continued to climb throughout 2023, with the effective federal funds rate reaching 5.33% in August 2023. For the remainder of 2023, the FOMC decided to maintain the current federal funds range, ending a long string of rate hikes dating back to March 2022.

CD rates remained high through 2024, with the best CD rates topping 5.00%. Even some large national banks were paying 5.00% on short-term CDs. The best online banks were paying upward of 5.30% on 12-month CDs.

The Federal Reserve announced the first rate cut in September 2024 in response to a softening job market, which triggered a downward trend in savings rates. The best CD rates now range from 3.80% to 4.10% APY. In the October 28-29 meeting, the Fed also indicated another rate cut could occur in December, so it's possible CD rates will continue to decrease in 2025.

Why Your CD Rate Lags the Fed—and How to Make It Work for You

You’ve probably heard that when the Federal Reserve raises interest rates, banks tend to boost what they pay on savings accounts and CDs. But here’s the reality: rate cuts may show up more immediately, while increases don’t always show up right away, or match the Fed’s moves dollar for dollar.

According to data from the Federal Reserve Bank of St. Louis, the average federal funds rate over the past five years was 2.83%.

During that same period, the average yield on a 12-month CD was just 1.16%, while six-month CDs averaged 0.96%. That’s a spread of nearly two percentage points.

Even during the Fed’s aggressive rate hikes between 2022 and 2024, when policymakers raised rates by over five percentage points to fight inflation, CD yields lagged. Many banks used the higher-rate environment to widen profit margins, offering modest increases in CD returns without fully passing on the benefit to savers.

On the flip side, when the Fed starts cutting rates—as it did in late 2024—CD yields tend to drop quickly. In fact, they often fall faster than they rise. For example, Sallie Mae’s 12-month CD dropped from 5.15% in June 2024 to 4.20% by June 2025—a sharp decline in just one year.

This uneven movement means timing matters. When the Fed is raising rates, banks may delay increasing CD yields. But when cuts are expected, rates can fall fast. If you're hoping to lock in a competitive return, waiting too long can cost you.

That’s why it pays to shop around and act strategically. While national averages can lag behind the Fed, some banks offer top-tier rates that respond more quickly to policy shifts.

Where To Find the Best CD Rates

Rates aren’t what they were at the end of 2023, but the top CD offerings are still strong, especially if you know where to look.

- Online banks tend to lead the pack. They offer higher yields and lower fees thanks to lower operating costs. Plus, they’re more aggressive about attracting new customers.

- Credit unions are another great option. These nonprofit institutions often return value to members in the form of better savings products.

- Promotional CDs can deliver standout yields, but they may come with unconventional terms like 11 or 19 months. If you're flexible, you can cash in on those short-lived offers.

The best CD rate for you depends on your savings goals, timeline, and how much flexibility you need. But one thing is clear: A little research now can go a long way in boosting your returns.

Best CD Rates

Make Your Savings Count

Don’t just park your money and hope for the best. CD rates may rise, fall or flatline, but savers who stay sharp and strategic are the ones who come out ahead.

Here’s how to make your money work harder:

- Compare CD rates like you compare flight prices. Online banks often offer the highest yields because they don’t have the overhead of traditional institutions, and they’re hungry for your business.

- Lock in now if you think cuts are coming. When the Fed drops rates, banks follow fast. The best CD deals tend to vanish overnight.

- Use short-term CDs if you want options. They give you flexibility while still delivering solid returns, especially in a shifting rate environment.

- Save more, earn more. It’s basic math. A $10,000 deposit at 4.5% earns $450 in a year. Double it and you earn $900.

Frequently Asked Questions (FAQs)

Will CD rates go up in 2025?

Not likely. CD yields topped out around the end of 2023 and fell throughout 2024 as the market expected the Fed to cut rates.

When will CD rates go up?

Unless inflation reemerges, causing the Fed to hike the federal funds rate, don’t expect CD rates to increase.

Should I invest in a CD?

CDs offer guaranteed returns and are federally insured. If you have funds that you won’t need right away, CDs are an excellent way to build up your savings. It’s a good idea to have a fully funded emergency fund so you don’t have to withdraw money from a CD before it reaches maturity.

If you’re not sure that you can part ways with your cash long-term, you might be better off looking for the best high-yield savings accounts, which may offer rates comparable to CD rates.