Let (X, Y), (X 1 , Y 1), (X 2 , Y 2),. .. denote independent positive random vectors with common distribution function F (x, y) = P (X x, Y y) with F (x, y) < 1 for all x, y. Based on the X i and the Y j we construct the sum sequences S 1...

moreLet (X, Y), (X 1 , Y 1), (X 2 , Y 2),. .. denote independent positive random vectors with common distribution function F (x, y) = P (X x, Y y) with F (x, y) < 1 for all x, y. Based on the X i and the Y j we construct the sum sequences S 1 n and S 2 m respectively. For a double sequence of weighting constants {b(n, m)} we associate a weighted renewal function G(x, y) defined as G(x, y) = ∞ n=0 ∞ m=0 b(n, m)P (S 1 n x, S 2 m y). The function G(x, y) can be expressed in terms of wellknown renewal quantities. The main goal of this paper is to study asymptotic properties of G(x, y). In the one-dimensional case such results have been obtained among others by Omey and Teugels [Weighted renewal functions: a hierarchical approach, Adv. in Appl. Probab. 34 (2002) 394-415.] and Alsmeyer [Some relations between harmonic renewal measures and certain first passage times, Statist. Probab. Letters 12 (1991) 19-27; On generalized renewal measures and certain first passage times, Ann. Probab. 20 (1992) 1229-1247]. Here we prove a multivariate version of the elementary renewal theorem and moreover we obtain a rate of convergence result in this elementary renewal theorem. We close the paper with an application and some concluding remarks. For convenience we prove and formulate the results in the two-dimensional case only.

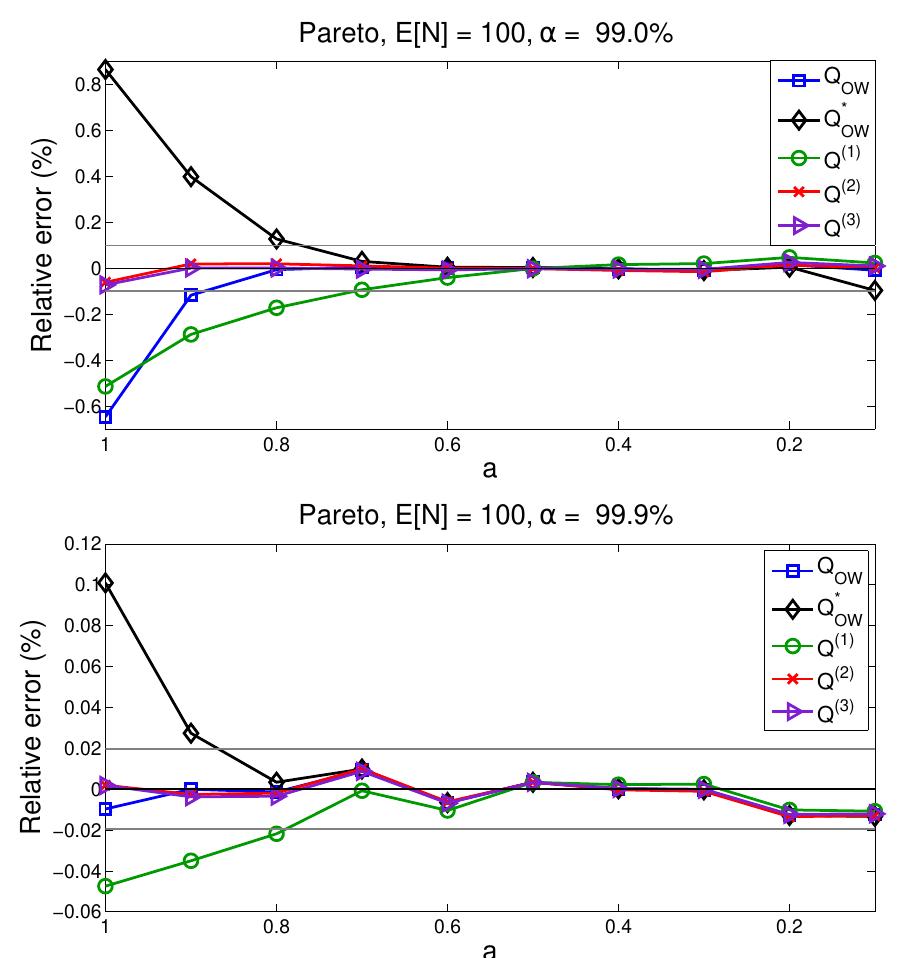

![Fig. 8 Relative error for Pareto/Poisson as a function of E[N] for a = 99.9% and different values of a: a = 2.00 (upper plot) and a = 1.20 (lower plot).](https://figures.academia-assets.com/105789926/figure_015.jpg)

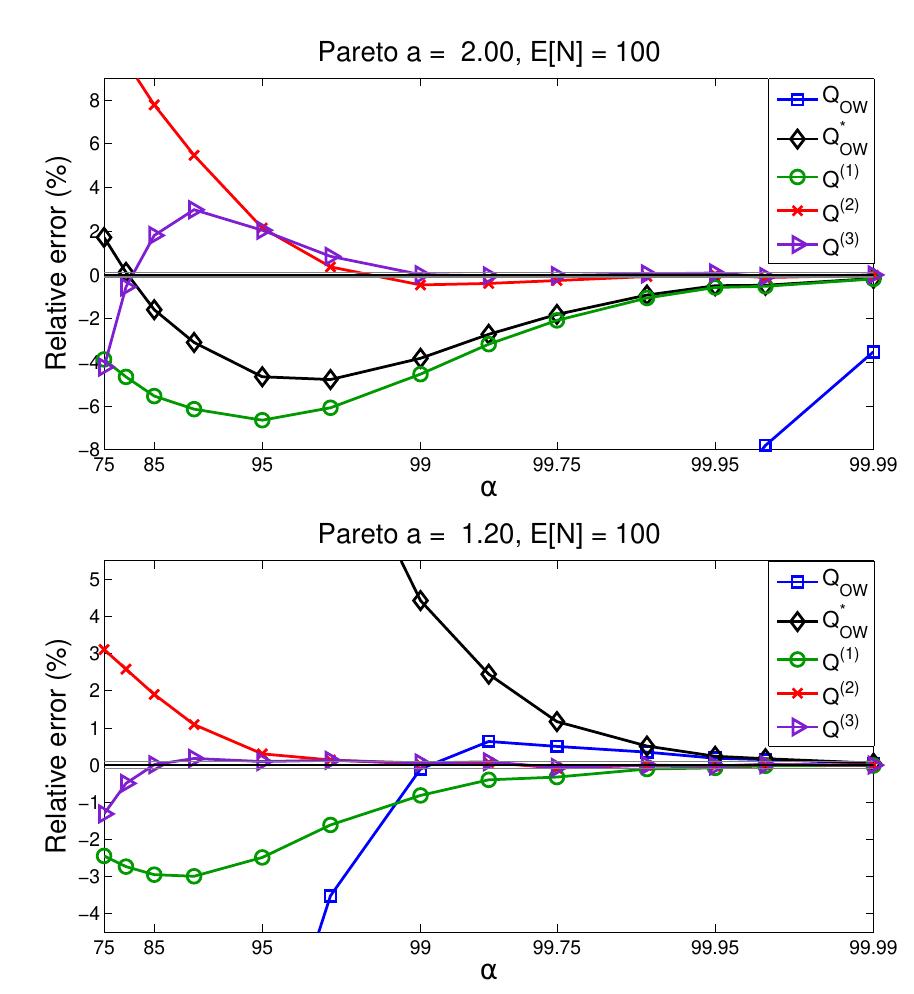

![Fig. 11 Relative error for Poisson/Pareto as a function of E[N] for a = 99.9% and different values of a. Fig. 10 Relative error for Poisson/Pareto as a function of a for X = 100 and different values of a.](https://figures.academia-assets.com/105789926/figure_017.jpg)

![Fig. 5 Relative error for Lognormal(o = 2)/Poisson as a function of a for E[N] = 100 (upper plot) and as a function of E[N] for a = 99.9% (lower plot) Fig. 4 Relative error for Lognormal /Poisson (A = 100) as a function of o for a = 99% (upper plot) and a = 99.9% (lower plot). 5.3 Pareto distribution](https://figures.academia-assets.com/105789926/figure_011.jpg)

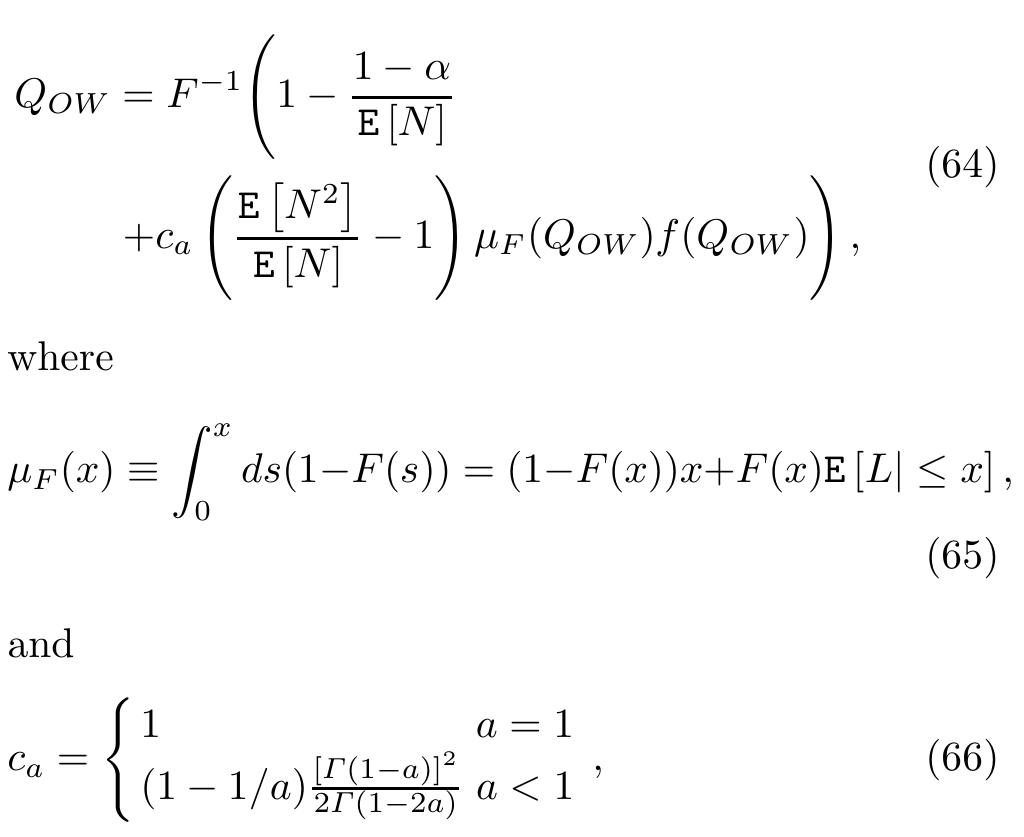

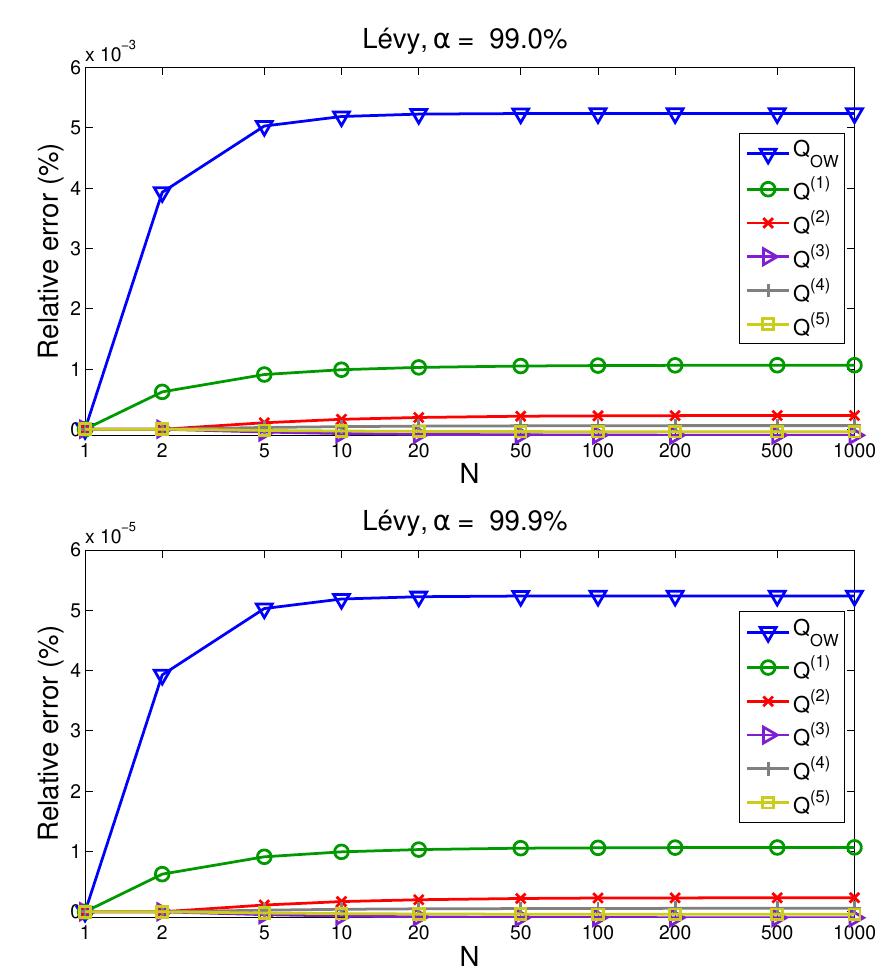

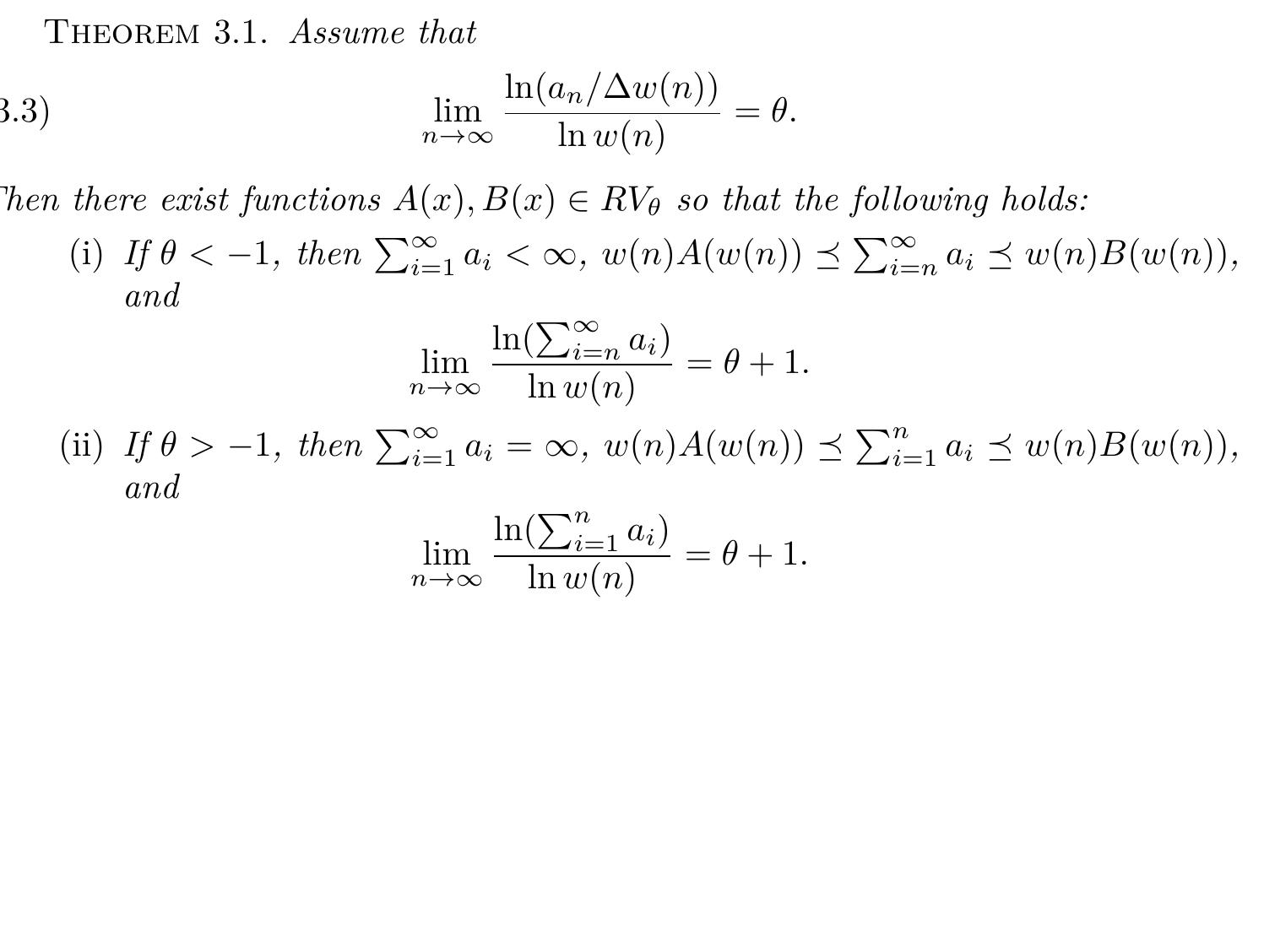

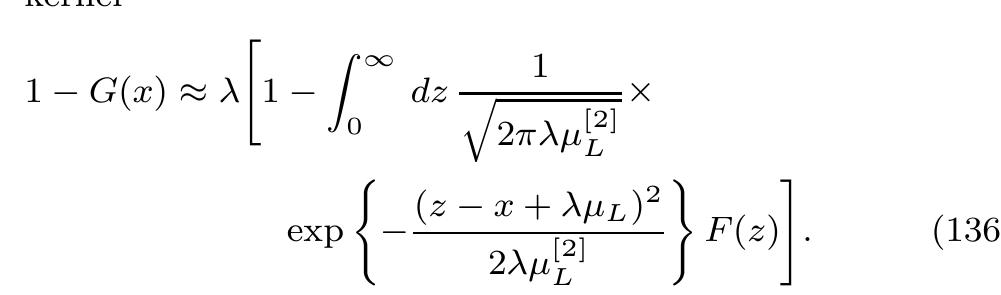

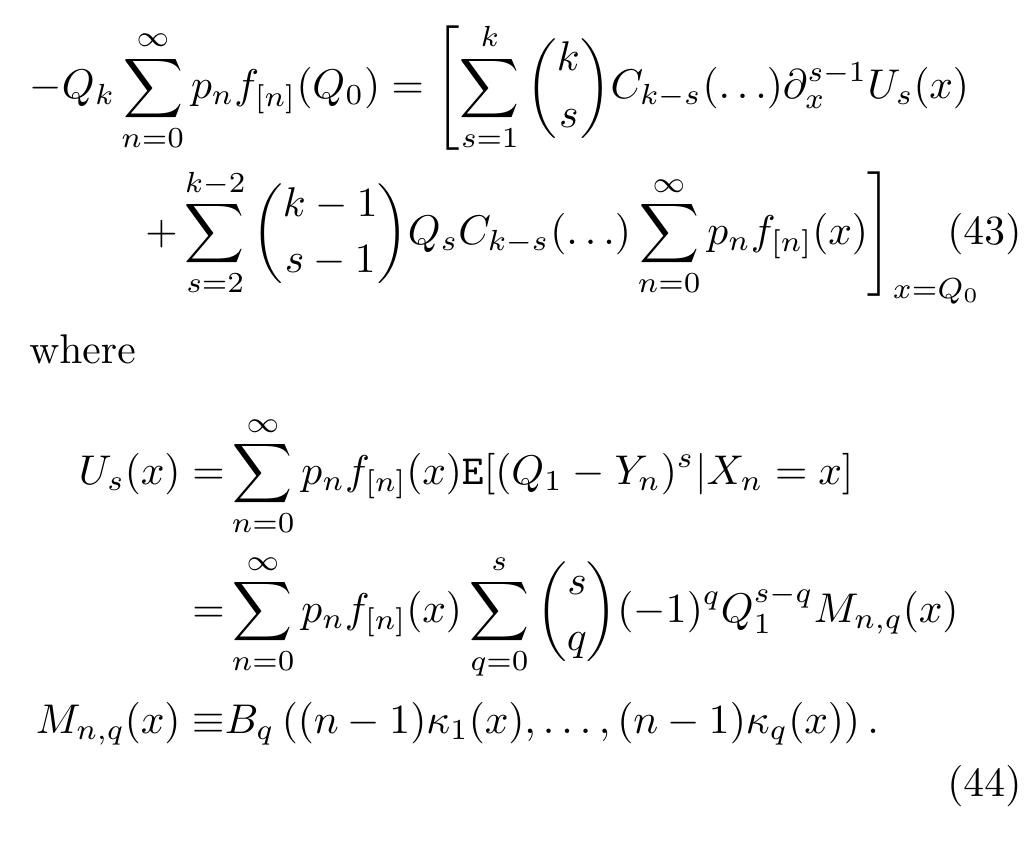

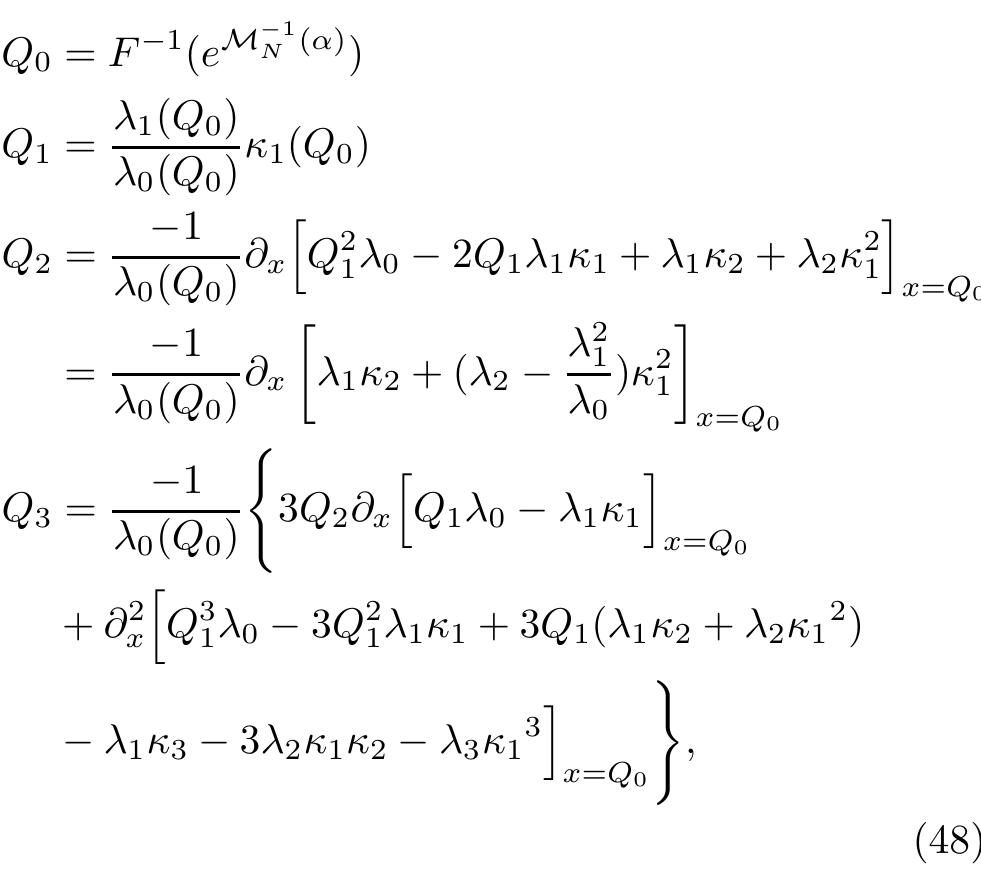

![where v, = E[N*] are the moments of the frequency dis- tribution. Using these approximations, the high-percentile corrections to the single-loss formula can be expressed directly in terms of the moments of the frequency dis- tribution The approximation to Q, is similar to the corrections to the single loss formula proposed in the literature (Bocker and Sprittulla, 2006; Sahay et al, 2007; Degen, 2010; Albrecher et al, 2010). In section 4, we provide a review of these corrections. Their accuracy will be compared to the perturbative expansion in section 5. To make the numerical computation of the perturba- tive approximation up to high orders feasible it is use- ful to express the terms of the series recursively. These recursive expressions are presented in Appendix C.](https://figures.academia-assets.com/105789926/figure_006.jpg)